Do you remember Allianz, the prominent German insurer, wanting to buy a 50% controlling stake in Income in July? Well, it seems that the deal is on hold (for now).

Following a thorough parliamentary review and amendments to the Insurance Act, the government has rejected Allianz's current proposal to gain a foothold within Singapore’s fastest-growing and deeply-rooted insurance institutions.

Key concerns raised by the government include unresolved complexities in the acquisition agreement terms, and ongoing public doubts about Income's commitment to its long-standing social missions in Singapore—the cornerstones of its identity for nearly six decades.

What you need to know about NTUC Income—the trusted insurer for Singaporean working class

Established in 1970 by the National Trades Union Congress (NTUC), the social enterprise was a much-needed answer to demands for affordable coverage among underserved workers and middle-to-low income families, who were once vulnerable to working hazards and accidents without proper protection.

Given Singapore's early development as a country of mostly working class, it was necessary for the Labour Movement to evolve into a social institution that prioritised the workers' needs. Hence, those earning a monthly salary of $1,101 to $1,800 could enjoy coverage for costly expenditures, including:

- In-patient medical fees

- Special needs packages (Income remains the only insurer to cover children with autism)

- Payouts to support social causes (ie. children’s life and education expenses)

Besides Income, NTUC also expanded its mission to other facets of Singaporean life, particularly consumer protection.

NTUC FairPrice, a supermarket chain founded in 1983, offers essential goods at affordable prices to tackle unscrupulous consumption by those who hoard and profit from scarce items. Its goal was (and still is) to support workers' rights and ensure they can always afford a decent meal on the table.

Others co-operatives under NTUC include:

- NTUC Club: Provides recreational activities and spaces for both the public and union members.

- NTUC First Campus: Singapore's largest Early Childhood Care and Education service providers, with more than 170 preschool centres in operation.

- NTUC Health: Enables affordable eldercare and health services, including day/senior care centres, home care services, family medicine clinics, dental clinics, pharmacy retail outlets, and senior activity centres.

- NTUC LearningHub: Leading Continuing Education and Training provider that aims to transform the lifelong employability of working people across 29,000 organisations in Singapore.

To this day, Income Insurance is still the first and only cooperative insurer in Singapore, with as many as 2 million policyholders. Many Singaporeans (including us) consider Income a national icon. Unlike other insurers that frequently increase premiums, Income maintains reasonable pricing for its insurance schemes.

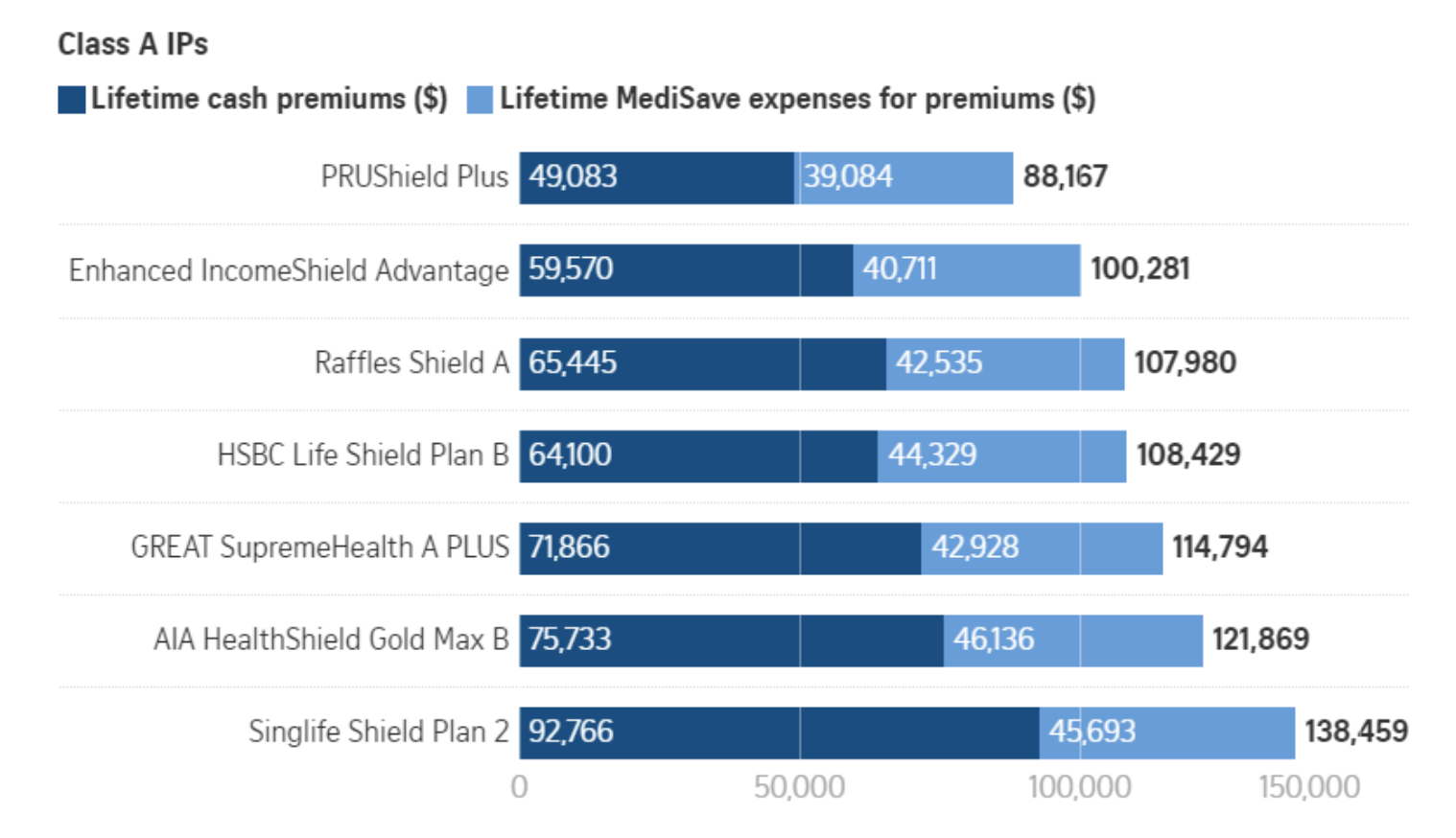

Example: Consider the lifetime pricing of Income’s Enhanced IncomeShield Advantage health insurance, as compared to other notable institutions:

Lifetime premium of Integrated Shield Plan in July 2024. Image: Strait Times

As of July, Income's lifetime premiums remain the lowest among the six insurers, and nearly half the price of Singlife Shield Plan 2, which costs you a staggering $92,766.

Why did the sale of NTUC Income happen in the first place?

In 2022, Income cited strong competition from over 40 international and domestic insurers, bancassurance (hybrid between banks and insurers) and tech players (i.e. DigiBanks). Thus, they began restructuring and transitioned towards becoming a corporate entity under Income Insurance Ltd.

As a co-operative, Income was restricted in its ability to raise capital from sources outside of other cooperatives and trade unions. This move would assist Income in accessing a wealth of funding from global investors (such as Allianz) to continue rolling out new products, while staying competitive domestically.

Just 2 years later, however, Income decided to sell more than half of Income's shares, citing ongoing operational challenges, including difficulties with scaling its business model and attracting top talent as key factors in its decision.

Why is the deal controversial and how does it affect Singaporeans?

First, it contradicts Income’s primary stakeholder promise made in 2022

The first concern most Singaporeans have is that the sale directly contradicts NTUC’s promise of remaining the majority stakeholder in the corporatisation announcement.

NTUC currently holds 72.8% of Income’s total shares, with the remaining shares owned by individual shareholders. Should Allianz acquire a 51% stake and minority shareholders are unwilling to tender their shares, NUTC’s control could go from 49% to as low as 21% following the sale.

Second, it reflects Income as prioritising profits over people

With NTUC's apparent loss of control over Income, many believed that Allianz, a profit-driven institution, could fundamentally alter Income's core mission—from providing coverage to Singapore's underserved communities to prioritising financial gains.

This has been the case for many foreign buyouts throughout Asia. Over the past 2 years, around 300 local hotels in Vietnam's major cities of Hanoi and Ho Chi Minh City have been listed on the market each month. Despite the possibility of restructuring to retain ownership, many owners opt to sell to foreign bidders as a viable exit strategy for cost write-off.

This reliance on foreign capital has accelerated international dominance in the Vietnamese hotel industry, reducing a once-strong pipeline of local enterprises to mere components of conglomerates' portfolios and undermining consumer trust in domestic products/services.

To further illustrate, Income Insurance, since its corporatisation, has also taken a more aggressive approach to divert resources for increased profitability, particularly in real estate:

- In 2022, NTUC’s Mercatus Co-operative divested Jurong Point and Swing By @ Thomson Plaza, along with a 10-year property management service agreement for AMK Hub, to Hong Kong’s Link REIT for $2.16 billion.

- In 2023, Mercatus divested another portfolio of 18 commercial properties in HDB estates for around $265 million. One year later, Income Insurance sold its 11-storey commercial building at Prinsep for $147 million.

The new directions led some to believe that the deal is another 'backdoor' attempt by NTUC to secure larger financial gains, while straying away from its original goal - protecting Singaporean interests.

Third, changes in prices and policies are likely to roll out for future Income customers

Since the news broke out, both NTUC and Allianz have reiterated their commitment to fulfilling several existing initiatives, such as:

- Provision of $100 million over a 10-year-period (starting from 2021) to community and sustainability causes, as well as $1 billion to combat climate change;

- Continuation of low-cost insurance schemes such as NTUC GIFT and LUV for coverages against sudden deaths/permanent disabilities among lower-income seniors.

However, the Monetary Authority of Singapore (MAS)—the regulatory body of the Income/Allianz deal—is only requiring both parties to uphold existing contracts, should the sale be approved by 2025. As a result, future policyholders may still be subject to drastic adjustments in terms and conditions, product offerings and services.

What are the outlined benefits for both Allianz & NTUC Income?

As mentioned above, Allianz intends for Income to continue partaking in national insurance programmes, as well as maintaining its commitment to initiatives that benefit workers and the environment.

The German insurer also stated that, as Income’s life insurance market share went down to less than 10% over the last decade, its majority stake will strengthen the national insurer’s relevance and resilience in Singapore, enabling it to better serve Singaporeans.

However, Income's historical performance suggested otherwise. In 2023 alone, its purchasing expectations and completions(26.5%) surpassed those of multinational companiesin Singapore, including AIA (18.2%) and Prudential (16.9%), highlighting a stronger market presence than what is indicated.

In contrast, the deal would significantly elevate Allianz's position in the P&C (Property & Casualty) and Health and Life insurance markets, propelling it from the ninth-largest insurer in Asia to the fourth, and from third to second in Singapore. From a purely business perspective, the acquisition seems to favour Allianz rather than NTUC Income.

Why was the current proposal rejected?

Transparency remains a key issue

Going back to 2022, Income, now formerly a cooperative, was required to transfer S$2 billion in surplus funds to a government account, or the Co-operative Societies Liquidation account to benefit other cooperative sectors and movements, as part of its corporatisation.

Income then successfully appealed and wasallowed to retain all of the funds. The government deemed that Income’s assurance of upholding its social missions, despite the legal changes, was credible for the insurer to utilise the surplus and strengthen its capital in a competitive market.

However, in contrast to Income's earlier pledge, Allianz is now proposing a capital reduction of around S$1.85 billionwithin the first 3 years of acquisition. This has raised additional concerns about Income's future direction under Allianz:

- Impact on Financial Stability: Reducing Income's capital could weaken Income’s financial stability and ability to meet its obligations to long-term social initiatives in Singapore.

- High Potential for Increased Premiums: To maintain adequate financial reserves, Income might increase premiums for its policyholders, or trimming down on assurance packages that specifically cater to low-income families.

- Reduced Solvency: Capital decrease could lower Income's solvency ratio, which measures an insurer's financial strength and ability to pay claims. Lower solvency ratio could raise concerns about Income's financial security.

No legal documents for the capital reduction proposal (as of October)

Furthermore, besides MAS, notable regulators such as the Ministry of Culture, Community and Youth (MCCY), who initially approved of the deal, was not informed of the latest decision.

As there has yet to be specific guidelines to guarantee Income's focus on social missions, along with long-term financial plans post-capital reduction, the government decided to include MCCY’s perspectives in the revised Insurance Act.

Future applications from co-op insurers or those linked to cooperatives will now be evaluated by both the MAS and the MCCY with a stronger emphasis on social impact to ensure the rightful benefits for workers and Singaporeans alike.

What is next for Income policyholders?

After the deal fell through, Allianz is now revising its proposal to address the government's concerns and resubmit it for review. The government remains open in considering a revised version, should it adequately address the ongoing concerns.

Meanwhile, the Monetary Authority of Singapore (MAS) has increased its oversight of Income's strategy and capital management to protect the interests of existing policyholders during this lingering period. However, it still begs the question. How will future holders be affected by the acquisition, once the deal is done?

Final thoughts

The future of Income depends on how this revised proposal finally unfolds. Singaporeans need clearer details, stronger regulations, and complete transparency. More importantly, assurances that the focus on its social missions and affordable insurances will not be compromised.

There will still be risks of higher premiums, slight shifts in Income's focus—exemplified by the ongoing plans for expansion in Asia-Pacific—or regulatory hurdles. It's crucial to stay informed of the situation, monitor progress, and actively advocate for our interests so Income continues to benefit all Singaporeans and new policyholders alike.

What are your thoughts on Allianz's Bid for NTUC Income? Share them with us on Instagram.