*Note that insurers may adopt the new definitions at an earlier date — before 26 August 2020.

On 29 August 2019, the Life Insurance Association (LIA) Singapore announced changes to the critical illnesses (CI) definitions and names, effective no later than 26 August 2020.

Why the review?

According to LIA Singapore, this round of review:

- Addresses ambiguities that have arisen due to medical advancements and health trends in the past 5 years

- Ensures that CI products stay relevant with the changing times, especially with Singapore’s rapidly ageing population and rising incidences of chronic illnesses

- Ensures that the intended scope of coverage is clear to consumers

LIA Singapore clarified that changes are meant to express the intent of the coverage with greater clarity, so that customers do not misunderstand what is being covered and what is not. There is no change to the intended scope of coverage, when compared against the definitions of 2014.

The last update to LIA Singapore’s CI definitions was in 2014, where some of the 37 severestage CIs definitions were revised; and the maximum limit of 30 medical conditions per CI plan was abolished to allow for more medical conditions to be covered.

All member companies of LIA Singapore and the General Insurance Association of Singapore will need to adopt the set of revised definitions no later than 26 August 2020.

However, policyholders with existing CI policies are not impacted by the new CI definitions. Here’s an overview of the upcoming changes to CI definitions, and how they compare with the existing CI definitions:

What are the changes?

Here’s a quick look at what’s been changed (we have omitted what has not been changed, but you can read the detailed list of the LIA CI Framework 2019):

Before 26 August 2020 — LIA CI Framework 2014 | From 26 August 2020 — LIA CI Framework 2019 | Change to name? | Change to definition? |

Major Cancers | Major Cancer | Yes | Yes |

Heart Attack of Specified Severity | Heart Attack of Specified Severity | No | Yes |

Stroke | Stroke with Permanent Neurological Deficit | Yes | Yes |

Aplastic Anaemia | Irreversible Aplastic Anaemia | Yes | Yes |

Deafness (Loss of Hearing) | Deafness (Irreversible Loss of Hearing) | Yes | Yes |

Loss of Speech | Irreversible Loss of Speech | Yes | Yes |

Parkinson’s Disease | Idiopathic Parkinson’s Disease | Yes | Yes |

Viral Encephalitis | Severe Encephalitis | Yes | Yes |

Blindness (Loss of Sight) | Blindness (Irreversible Loss of Sight) | Yes | Yes |

Coma | Coma | No | Yes |

Multiple Sclerosis | Multiple Sclerosis | No | Yes |

Muscular Dystrophy | Muscular Dystrophy | No | Yes |

Alzheimer’s Disease / Severe Dementia | Alzheimer’s Disease / Severe Dementia | No | Yes |

HIV Due to Blood Transfusion and Occupationally Acquired HIV | HIV Due to Blood Transfusion and Occupationally Acquired HIV | No | Yes |

Benign Brain Tumour | Benign Brain Tumour | No | Yes |

Major Head Trauma | Major Head Trauma | No | Yes |

Progressive Scleroderma | Progressive Scleroderma | No | Yes |

Systemic Lupus Erythematosus with Lupus Nephritis | Systemic Lupus Erythematosus with Lupus Nephritis | No | Yes |

Other Serious Coronary Artery Disease | Other Serious Coronary Artery Disease | No | Yes |

Poliomyelitis | Poliomyelitis | No | Yes |

Loss of Independent Existence | Loss of Independent Existence | No | Yes |

Kidney Failure | End Stage Kidney Failure | Yes | No |

Heart Valve Surgery | Open Chest Heart Valve Surgery | Yes | No |

Surgery to Aorta | Open Chest Surgery to Aorta | Yes | No |

Bacterial Meningitis | Severe Bacterial Meningitis | Yes | No |

Paralysis (Loss of Use of Limbs) | Paralysis (Irreversible Loss of Use of Limbs) | Yes | No |

Apallic Syndrome | Persistent Vegetative State (Apallic Syndrome) | Yes | No |

We want to highlight the changes to some most commonly claimed CIs (according to LIA).

Major Cancer

The name changes from “Major Cancers” to “Major Cancer”, and there have been changes to the definition as well.

Added to definition: Major Cancer diagnosed on the basis of finding tumour cells and/or tumour-associated molecules in blood, saliva, faeces, urine or any other bodily fluid in the absence of further definitive and clinically verifiable evidence does not meet the above definition.

Reason: With the development of research into liquid biopsy, it is necessary to future-proof the definition to avoid the situation of having to consider a claim based on blood or body fluid test with no identifiable tumour cells.

An exclusion has been added for bone marrow malignancies. According to LIA Singapore, there are some newer bone marrow malignancies, despite being classified as “03-malignant” by the World Health Organization (WHO), which are really minor cancers and where no high risk treatment is required, they do not fulfill the intent of severe stage coverage.

Other changes and full details can be found here.

Stroke with Permanent Neurological Deficit

The name changes from “Stroke” to “Stroke with Permanent Neurological Deficit” to reflect intent.

An exclusion is added for secondary haemorrhage within a pre-existing cerebral lesion. As explained by LIA’s statement for changes: Sometimes, after a cranial surgery, the pathological analysis of the resected tumour could show signs of “intra tumour” bleeding. Whilst there is intracranial or cerebrovascular bleeding, it is not a valid claim under the Stroke definition. The bleeding in this instance is due to the cranial surgery, and not the same underlying pathology as “Stroke” as intended to be covered here. This is to address such misunderstandings.

Other changes and full details can be found here.

Heart Attack of Specified Severity

By replacing the word “obstruction of blood flow” with “ischaemia”, this better reflects the intent to cover both Type 1 Myocardial Infarction (MI) and Type 2 MI.

If you are interested to find out more on other CI definitions changes, you can refer to the LIA CI Framework 2019 for more details.

Besides looking at definition changes above, here are some other things one can consider when thinking about CI coverage.

The importance of Early CI coverage

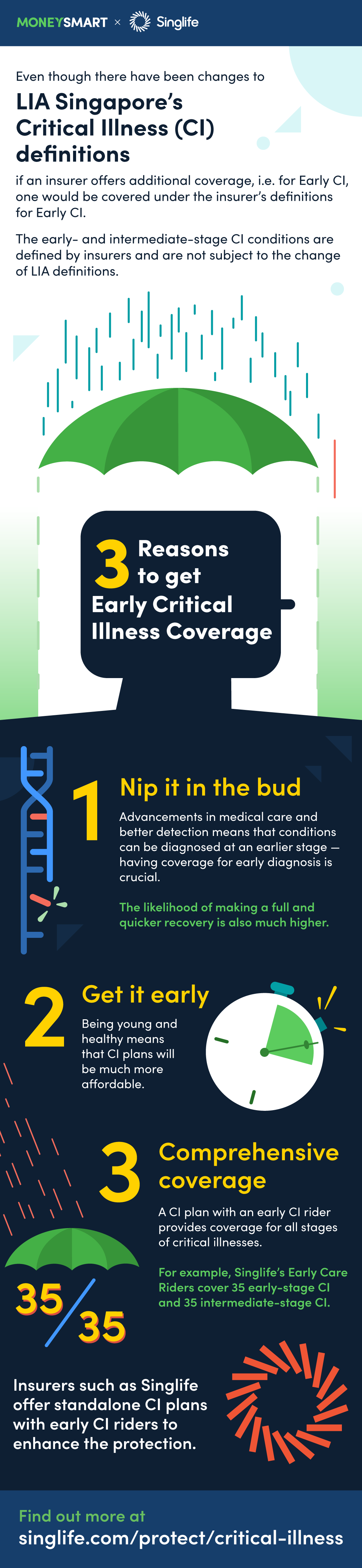

Even though there have been changes to LIA Singapore’s CI definitions, LIA’s common definitions describe the respective medical conditions at the ‘severe’ or ‘late’ stage. If an insurer offers additional coverage such as coverage for Early CI (ECI), one would be covered under the insurer’s definitions for ECI.

With today’s medical advancements, CI can be diagnosed at the earlier stages and treatment of CI at the earlier stages can improve chances of recovery — and with that, having coverage for early diagnosis is crucial. With ECI coverage, you can be sure that you will be covered for early and intermediate stages CIs.

Getting a CI plan early

Finally, with all this talk of CI, if you are indeed considering getting a CI plan, read this article for more information on the benefits of getting a CI plan early. (TLDR; being young and healthy means that CI plans will be much more affordable.)

Singlife’s CI plans offer

For those who are interested to purchase a CI plan, insurers such as Singlife offers standalone CI plans with ECI riders to enhance the protection. In addition, Singlife is currently the only insurer that allows individuals to purchase CI plans directly online.

Learn more about Singlife’s CI products and get a quote here.

Save 15% on your Critical Illness Base Plan + Rider. For a limited time only. Promo code: SAVE15

Terms apply. Head over to singlife.com/promotions for more information.

Terms & Conditions This premium discount is not applicable to any loadings imposed due to underwriting. Singlife reserves the right to amend the terms & conditions of this campaign at its sole discretion at any time without prior notice. The discounts are applicable throughout the policy term, as long as the policy remains in-force.

The information is meant for your general knowledge and does not regard any specific investment objectives, financial situations or particular needs any person might have and should not be relied upon as the provision of financial advice. Protected up to specified limits by SDIC. Singlife’s Critical Illness plan is protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact Singlife or visit the LIA or SDIC web-sites (www.lia.org.sg or www.sdic.org.sg). This advertisement has not been reviewed by the Monetary Authority of Singapore. Information is correct as of 13 July 2020.

Related Articles