Unlike a rolling stone that gathers no moss, idle cash doesn’t gather any interest. So, we’ve got to keep our hard-earned money “rolling” and hustling in order to make the most out of it.

But what exactly can you do with idle cash? Most of you are financially savvy enough to know that storing it in a piggy bank or in a sock under your bed is NOT a good idea. But did you know that leaving it in a regular savings account is almost just as bad?

When it comes to what to do with our money, we hear lots of different recommendations floating around. Everyone, from your parents to your friends, has an opinion. But how can we know which approach is really right for us?

Let’s look at two basic ways to generate returns from idle cash: using a cash management tool, and the more traditional path of using a fixed deposit with a bank.

What is a cash management tool?

A cash management tool enables you to invest your spare cash, usually in a money market fund, without sacrificing liquidity. You just transfer your spare cash to a cash management account, and it is automatically invested. There is no lock-in period, so you can withdraw your money whenever you wish, just like you would from a traditional savings account, without having to pay a penalty. There may be some management fees involved.

What is a fixed deposit offering from a bank?

Fixed deposits, also known as time deposits, are a common financial product offered by banks. They enable you to earn interest on your cash, on condition that your money stays “locked up” in the fixed deposit for a predetermined amount of time.

For instance, you may opt to put your money in a 24-month fixed deposit in exchange for an interest rate of x%.

The duration of fixed deposits can range from a few days to a few years, but the most common fixed deposits in Singapore run for 3, 6, or 12, 18 or 24 months. In general, the longer the tenure of the fixed deposit, the higher the interest rate. Paying in a larger amount can also secure a higher interest rate in some cases.

What happens if you need to withdraw cash from a fixed deposit? You typically lose all the interest you were supposed to earn, and might even get slapped with a penalty.

Cash management tool vs bank’s fixed deposit

The biggest difference between a cash management tool and a fixed deposit is liquidity. Cash management tools have no lock-in period, enabling you to withdraw your money whenever you want. Conversely, when it comes to fixed deposits, you cannot touch the cash until the full duration of the fixed deposit has run its course.

Here’s a summary of the key differences between cash management tools and fixed deposits:

Cash management tool | Fixed deposit | |

Lock-in | No | Yes, for duration of fixed deposit |

Fees | Depends on provider; minimal if any. i.e. Moneybull offers $0 fees^ | Forfeit of interest and possible penalty fee for early withdrawal |

Minimum amount to start | Depends on provider, minimal if any. i.e. Get started with Moneybull with just $1 | Yes, usually at least $5,000 |

Yield | Can go over 4%* | About 3.5%* with a lock-in of 6 months |

*Based on current market situation

Is a bank’s fixed deposit for you?

Fixed deposits can be worth it if you are willing to lock in your money for long enough and/or deposit a large enough amount to secure a really attractive interest rate. Some banks offer promotional interest rates that you can secure if you satisfy the minimum deposit amount.

One advantage of banks’ fixed deposits is that they are almost risk-free. The Singapore Deposit Insurance Corporation (SDIC) insures up to $75,000 worth of deposits per partner bank (this amount includes any other cash you might have with the bank, not just your fixed deposits). So, if you’re very, very risk-averse, you might feel safer with a fixed deposit.

If you have a large lump sum of cash that you’re very sure you won’t need for the next few months or years and are able to deposit enough of it to obtain a nice promotional interest rate that exceeds what cash management tools are offering, that’s a good argument for putting the money in a fixed deposit. However, the interest rate would have to be pretty attractive, considering how competitive cash management tools’ interest rates are nowadays.

Is a cash management tool the way to go?

Cash management tools offer a way to earn good returns on your idle cash, while preserving the flexibility to withdraw the money at any time. Because there is usually no minimum deposit, that makes cash management tools ideal for any amount of cash you might have lying around that you haven’t already invested.

Although, like all investments, cash management tools aren’t 100% risk free, they’re still considered a low-risk option, which makes them a good choice for those of us who can’t afford to lose money.

Interested in cash management tools but not sure where to look? Moneybull is a wealth management tool, owned by investment broker Webull, which enables you to earn a yield on idle cash while maintaining liquidity and low risk. Do note that you will need a margin account to activate Moneybull. The yield is generated by automatically investing your idle cash in underlying cash funds.

Moneybull charges $0^ fees, and the barriers to entry are ridiculously low — you can start growing your cash for as little as US$1 or S$1!

There’s no lock-in period, so you retain ultimate flexibility, which enables you to earn a higher yield on your idle cash without having to miss out on market opportunities. This means that idle funds in your Webull account can be auto-invested using Moneybull while you can still use the auto-invested amount to trade stocks and options as usual. This is like having your cake and eating it too!

.png)

- True zero fees for US Stocks

- US$0*

- Min. Commission Fee for SG Stocks

- S$0*

- Platform Fee

- US$0*

Invest, trade and get REWARDED 💥

Get up to S$230 Cash via PayNow

• OR Apple Airpods 4 with ANC (worth S$249)

• OR Garmin Forerunner 165 Watch (worth S$379)

• OR TTRacing Swift X Pro Gaming Chair (worth S$429)

OR choose from many more rewards when you meet invest, trade and maintain the min. deposit.

T&Cs apply.

[Webull Welcome Promotion]

• Get up to S$1,888* in Welcome Rewards. T&Cs apply.

• Enjoy 0% Platform Fees on US stocks, US options, and HK trades.

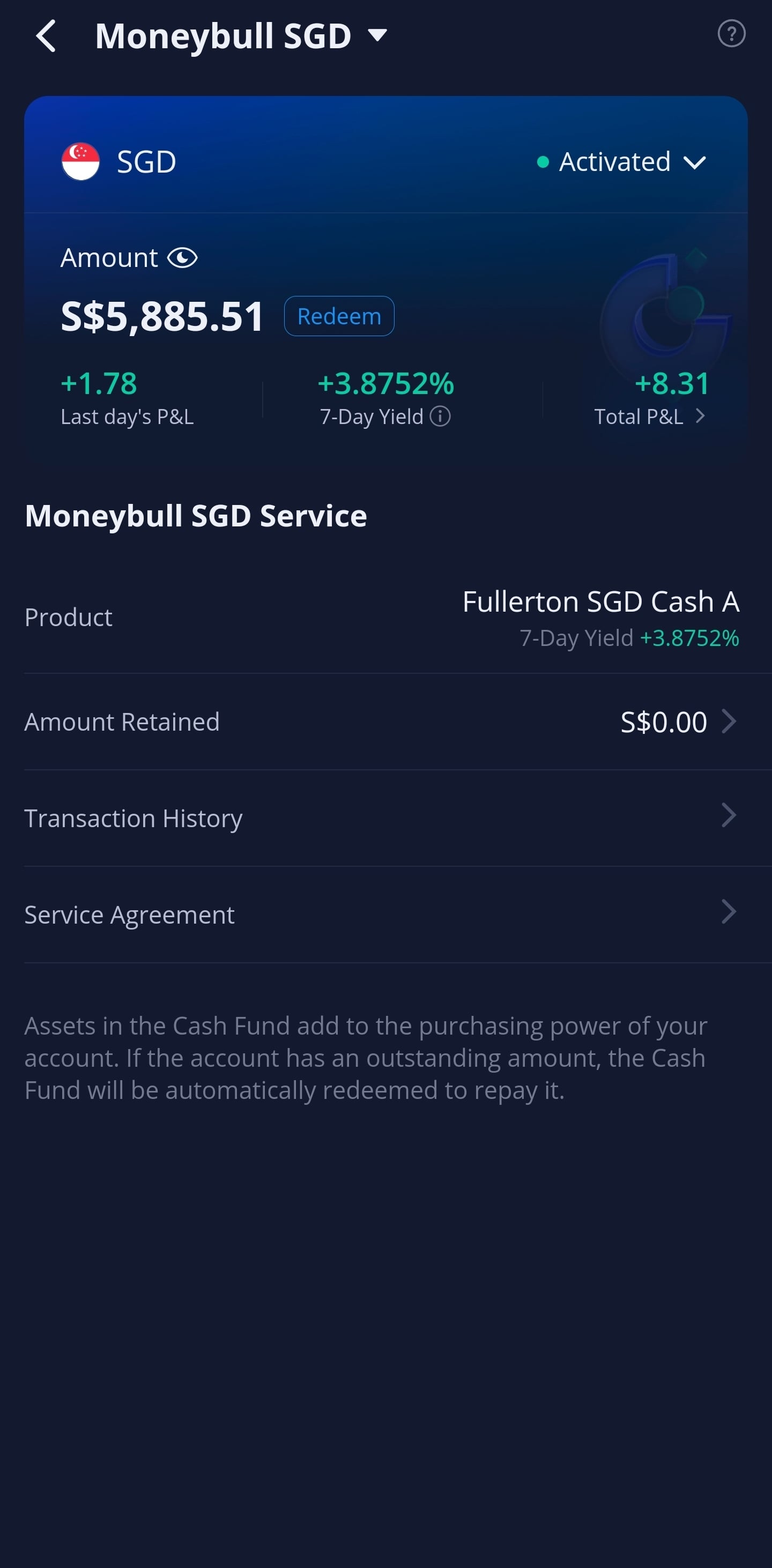

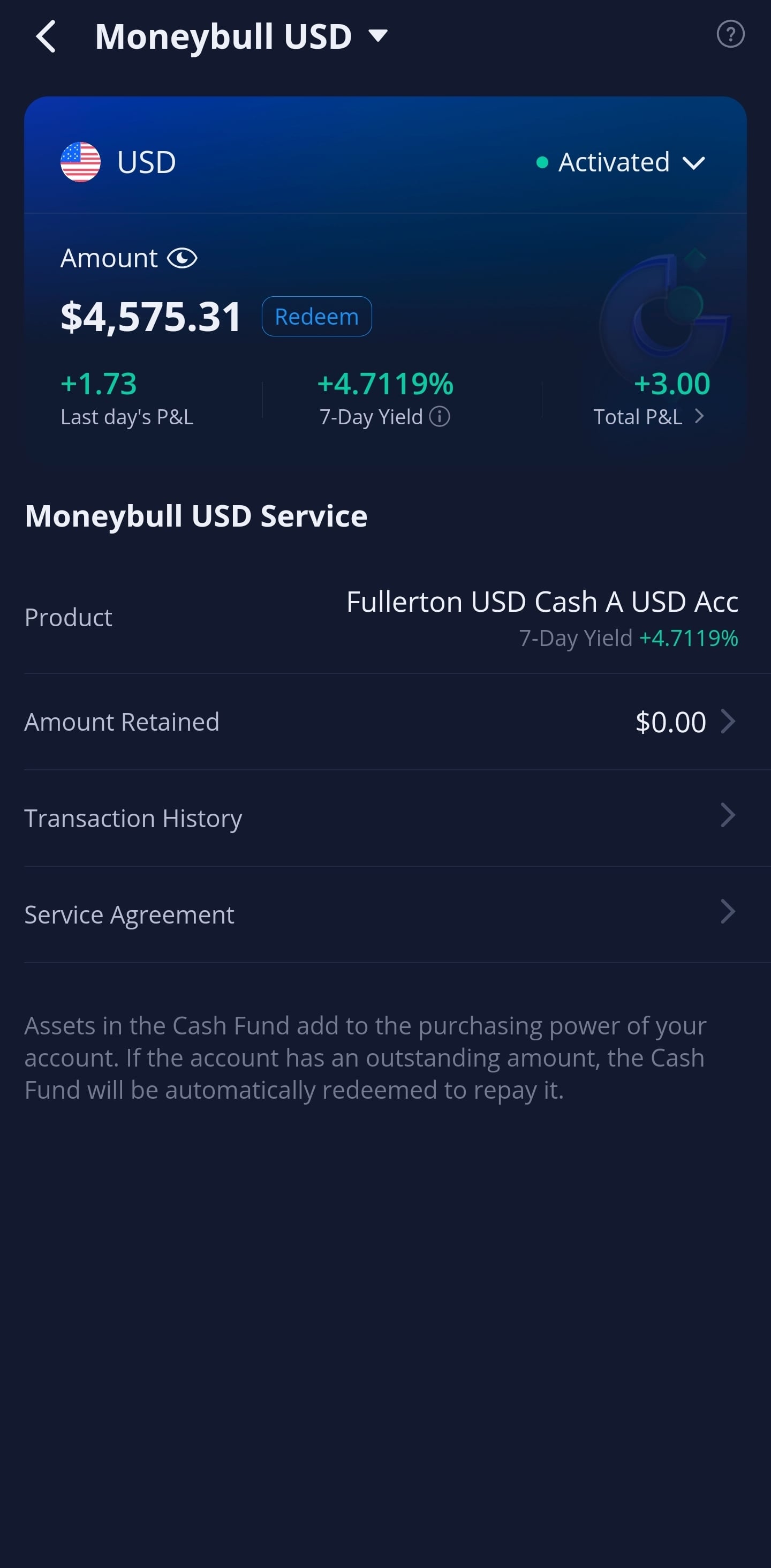

Let’s look at some screenshots of the Moneybull interface of a sample account that has invested both SGD and USD, as well as their 7-day yield.

Online Promo:

- Enjoy 0 commission^ for US trades and receive 5 free shares worth up to US$500 when you fund and maintain ANY amount in your Webull account for 30 days

- Receive up to US$300 worth of free shares when you invite 1 friend to open and fund ANY amount

- Climb the Webull Referral Leader Board to win up to USD3,888 worth of TSLA Shares

- Receive a BONUS reward of up to 100 free shares when you complete 5 successful referrals!

T&Cs apply. Promo valid until 28 April 2023.

Find out more on how to keep your idle cash working with Moneybull today.

- True zero fees for US Stocks

- US$0*

- Min. Commission Fee for SG Stocks

- S$0*

- Platform Fee

- US$0*

Invest, trade and get REWARDED 💥

Get up to S$230 Cash via PayNow

• OR Apple Airpods 4 with ANC (worth S$249)

• OR Garmin Forerunner 165 Watch (worth S$379)

• OR TTRacing Swift X Pro Gaming Chair (worth S$429)

OR choose from many more rewards when you meet invest, trade and maintain the min. deposit.

T&Cs apply.

[Webull Welcome Promotion]

• Get up to S$1,888* in Welcome Rewards. T&Cs apply.

• Enjoy 0% Platform Fees on US stocks, US options, and HK trades.

^Terms and conditions apply. For detailed terms and conditions and full disclaimer, please refer to the Webull website at https://www.webull.com.sg/. This advertisement has not been reviewed by the Monetary Authority of Singapore.

This post was written in collaboration with Webull Singapore. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best information in order for you to make personal financial decisions with confidence. You can view our Editorial Guidelines here.