This post was written in collaboration with UOB. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best recommendations and advice in order for you to make personal financial decisions with confidence. You can view our Editorial Guidelines here.

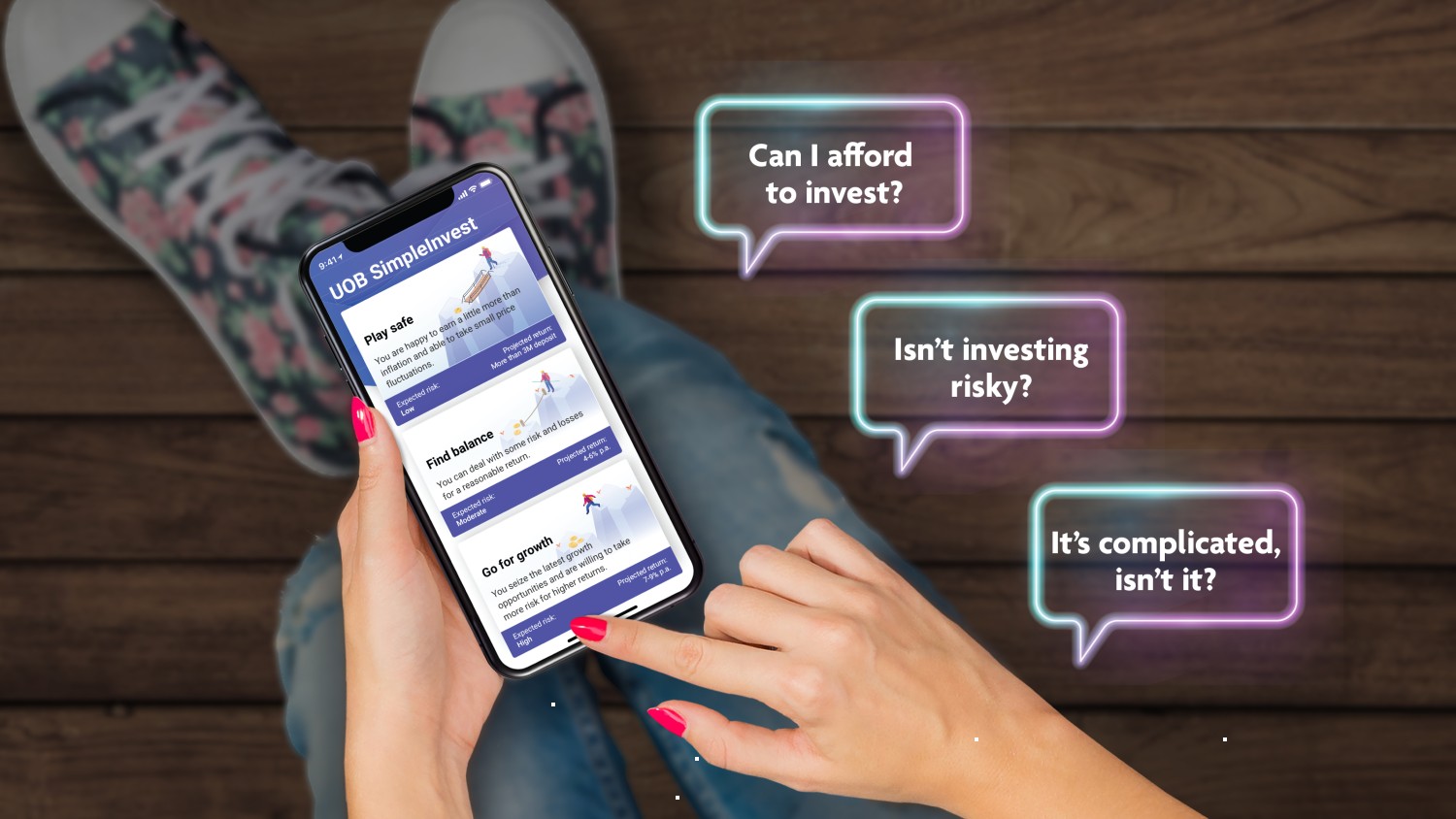

As a relatively new investor, I recall my initial struggles clearly. There were many barriers that prevented me from starting to invest, such as:

- My own fears (“Will I lose money? What happens if the value of my investment falls below what I put in?”)

- My personal money beliefs (“The most secure place for my money is the bank.”)

- Lack of financial knowledge and information overload (“I’m not sure where to begin.”)

- Lack of funds (“I need tens of thousands of ‘extra’ dollars to begin.”)

- And so on…

It was tough to break these mental walls, but I eventually embarked on my investing journey a year ago, thanks to the reassurance I received from like-minded friends and colleagues here at MoneySmart.

Increasingly, it’s much easier these days to get started with investing, as easily digestible financial information becomes more widely available online. Not to mention, investment platforms are more beginner-friendly with less jargon, friendlier interfaces, fewer complicated processes, lower minimum capital and so on.

During this one year of investing, I’ve also gained the realisation that there is no perfect time to start. It’s all about taking the first step, but it helps to get started on the right foot.

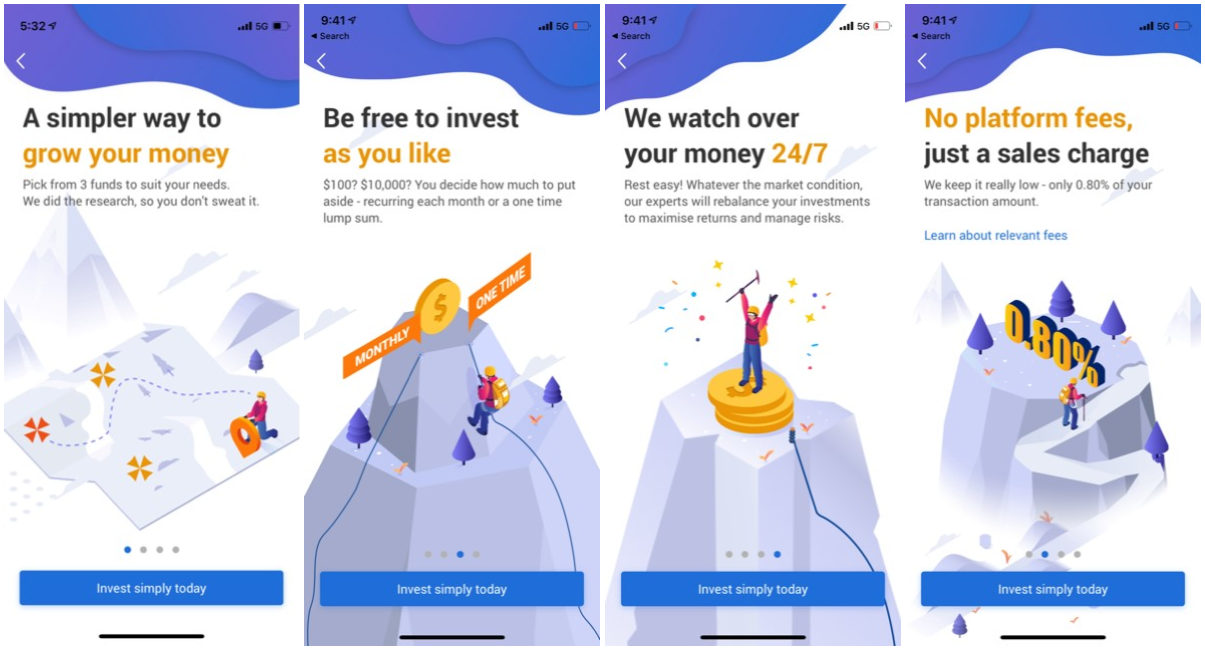

One of the newbie-friendly platforms I’ve discovered that really helps me push through my fears and inertia is UOB SimpleInvest, which can be easily accessed via my UOB Mighty app. Here are some ways UOB SimpleInvest helped me and will also benefit other newbie investors looking to embark on their investment journey. Here we go!

1. I’m able to start out at my own comfort level

Isn’t it scary if you muster the courage to try an investment platform, but as you’re all ready to transfer your funds, it tells you that the minimum investment is some 4- or (gasp) 5-figure sum? Yeowch!

With UOB SimpleInvest, I only had to invest a minimum of S$100 to get started (I can also set a regular investment amount of S$100/month if I’m looking to invest a larger sum but don’t have the upfront capital to do so). That’s low by today’s standards — S$100 would barely buy you: 1 cup of bubble tea every day for a month, a week’s worth of groceries if you cook every day or a lunch-time budget omakase meal.

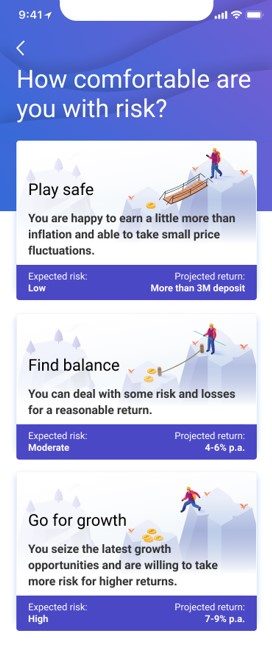

I could also take my pick from 3 simple solutions aligned with my personal investment goals and risk appetite. These are the Liquidity, Income and Growth solutions. Of course, the higher the risk level, the higher the possible returns — but just like how I live my life, I decided to just take the middle ground and find balance with the Income solution. If you have a low risk appetite and want to give investing a try, you can consider starting with the Liquidity solution. You can always choose another option or switch from your current one if you have a different investment objective in the future.

I like how UOB SimpleInvest brings me to a screen that showcases the projected return — or how much you can expect your investment to grow on average — for the different solutions and some further details. With some concrete details to look at, it feels like I’m jumping into a swimming pool (where there’s a lifeguard on watch and no scary waves) instead of the big sea.

It’s also nice that SimpleInvest has a friendly and clean interface (the more technical investment brokerages have apps that cram tonnes of numbers on screen with no clear guide or indication of risk level). This eases testy users like myself in and doesn’t scare me away due to my lack of financial knowledge and inability to interpret what I see on screen.

2. I have ‘human’ wealth managers instead of robots

Having played quite a few MMORPGs or simulator-type games when I was younger, I know that sometimes the code goes wonky, my character gets stuck, or a process I’m letting run (auto-levelling) could somehow fail on me and I see my character back in town with lesser EXP when I return one hour later.

So I’m not 100% comfortable with being entirely reliant on computer algorithms, such as what many robo-advisors offer. Yet, I do admit I enjoy the convenience of dealing with a digital interface any time I want.

It’s a nice touch that UOB SimpleInvest helps us invest through digital means, much like a robo-advisor. Yet, I feel relieved that the investments are still managed by experts from renowned asset managers who constantly monitor my investments and make adjustments when market conditions change. At a time when market movements can be unpredictable or sudden, having a human come in to make changes definitely trumps bots that may only rebalance investments at fixed intervals.

Despite UOB SimpleInvest’s involvement of human wealth managers, I don’t need to fork out a lot of money. I was pleasantly surprised that the fees are affordable — a sales charge of up to just 0.8% of my investment amount with no platform fees (it’s more affordable than many other actively managed investment solutions out there).

Which brings me to my next point...

3. I can actively invest while letting the experts do the work

Thanks to the experts with tonnes more financial experience than myself, my investments in UOB SimpleInvest are active investments, instead of passive investments. In the past, I’ve usually been focused on passive investing, due to my lack of market knowledge (I don’t know when to buy/sell and how to rebalance my own portfolio) and time to spare.

Passive investing: You put your funds in investments that track benchmarks such as the Straits Times Index, and you usually stick with this for the long haul. Hopefully it grows with time, due to inflation and with the market’s average returns. There’s usually minimal buying and selling (unless you want to cash out on surprising gains or need to take out funds for an urgent need).

Active investing: This requires a hands-on approach, with a goal to exceed financial markets’ average returns and capitalise on specific market opportunities. Those who do this need to actively monitor the market landscape and have deep knowledge in order to maximise returns.

Thus, instead of letting my investments be buffeted according to market movements and hoping it will rise in the long run, I can leave it to the pros to help me maximise my returns with their active investment strategies. It’s kinda like I’m on a ship with a captain steering us to land, instead of drifting along with the waves.

By being active with my investments (through the experts that are managing the SimpleInvest solutions), I’m able to capture opportunities, as well as megatrends that I’d usually miss out on if I passively tracked the market. Whoohoo!

And the best thing is, I don’t even need to be an expert myself yet I can invest like one.

4. I’m able to diversify from the start

One challenge new investors like myself face is that I can’t buy certain asset classes from the start (for example, due to the high entry point for bonds), or that I can’t buy into certain markets due to my lack of financial knowledge and trading experience.

Also, if I choose the DIY route, I would need to spend a lot of money to diversify my investments into all the companies and sectors I’m interested in (if I buy stocks, the minimum lot size is 100 and I’d need to pay a separate fee for each if I’m buying a la carte). Also, it’s difficult for newbies to diversify when we don’t have the knowledge of diversification from the get-go. All these factors limit our investment options and exposure in the market.

However, with UOB SimpleInvest, newbie retail investors like myself get access to a wide range of asset classes, such as equity, fixed income and multi-asset funds that cover global markets and different sectors. This helps me diversify my investments, which is important to consider because we never know how a certain sector might perform if something happens to the market. For example, Covid-19 rocked many sectors in the market that we thought were stable and previously doing well.

One thing to note is I don’t need to pay a lot either. Remember the S$100 I mentioned earlier? Yes, this applies to my diversified portfolio too! Plus, all of these is without me having to tear my hair out while trying to research the whole universe of investments myself.

As a newbie “player”, It’s like getting an overpowered item with top stats, so that I can get an edge from the very beginning of my quest. I’m loving this advantage!

5. No need to jump through multiple hoops to sign up

Surely there is some catch amid all the simplicity of UOB SimpleInvest, you ask? As someone who had to physically fill up and submit a form by post to open an account to make other investments, UOB SimpleInvest is by leaps and bounds quicker.

- As an UOB account holder, I only need to log in to my UOB Mighty app and tap on SimpleInvest to get started.

- Following which, I select the solution aligned with my investment objectives and risk appetite and complete a short knowledge assessment.

- It took me all of 3 minutes and my funds were deducted directly from my UOB account. No need to be physically present to open an investment account.

- My funds are invested rather quickly, in just 2 to 3 business days. Once that’s done, I can view my funds at a glance in the app. It shows me how much my investment has grown, and there is even a “Simple Insights” section that shares updates on how markets have been faring.

- I’ve also got the flexibility to withdraw my funds at any time. This means I can exit or redeem my investments freely without paying any exit or redemption fees. This is great news for my anxiety as I’m always worried about fees.

Note: As a beginner, it’s okay to “fail” the knowledge assessment. This means that UOB SimpleInvest is protecting your interests by not letting you invest in products you’re not ready for...yet. If you “fail” the knowledge assessment, you’ll still be able to invest in UOB SimpleInvest’s Liquidity solution.

Growing my investment confidence

In addition to helping me grow my money, UOB SimpleInvest also helps me grow my confidence as a newbie or newly-minted investor. For those who have yet to break the barriers of fear and overcome their investing inertia, taking the first step is really key.

The best way is to make this first step as comfortable as possible, by choosing the right platform from the get-go. It can be a super-safe baby step, but the objective is to take that step.

With UOB SimpleInvest’s friendly user interface, low investment amount and affordable fees, human experts managing the solutions and the ability to diversify my portfolio, it builds the confidence for me to venture into the investment world and gradually grow my financial knowledge.

I’m also happy that the platform is fuss-free and truly simple as its name suggests.

Find out more about UOB SimpleInvest and sign up for the UOB Mighty app here.

Disclaimers: The information herein is given on a general basis without obligation and is strictly for informational purposes only. It is not intended as an offer, recommendation, solicitation, or advice to purchase or sell any investment product, securities or instruments. Nothing herein shall be construed as accounting, legal, regulatory, tax, financial or other advice. You should consult your own professional advisors about issues mentioned herein that may be of interest to you as the information contained herein does not have regard to any specific investment objectives, financial situation and/or particular needs of any specific person. The information contained in this publication, including any data, projections and underlying assumptions, are based on certain assumptions, management forecasts and analysis of known information and reflects prevailing conditions as of the date of the article, all of which are subject to change at any time without notice. The views expressed in the articles linked to this publication are solely those of the authors’, reflect the authors’ judgment as at the date of the articles and are subject to change at any time without notice. United Overseas Bank Limited, its subsidiaries, affiliates, directors, officers and employees make no representation or warranty, whether express or implied, as to its accuracy, completeness and objectivity and accepts no responsibility or liability relating to any losses or damages howsoever suffered by any person arising from any reliance on the views expressed or information in this publication. This publication shall not be reproduced, re-distributed, duplicated, copied, or incorporated into derivative works, in whole or in part, by any person for whatever purpose without the prior written consent of United Overseas Bank Limited. Any unauthorised use is strictly prohibited.