This post was written in collaboration with Syfe. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best recommendations and advice in order for you to make personal financial decisions with confidence. You can view our Editorial Guidelines here.

It’s sooo easy to put off the things we should be doing till later: “I’ll run tomorrow lah”, “Diet starts next week”, or even, “I’ll invest when I have more money”.

And with great inertia comes great procrastination. How about all those times when “tomorrow”, “next week” or “later” just never seems to happen? Before you know it, half the year has passed...How is it June already but I’ve barely touched my goals for 2021?!

Despite our busy schedules and pressing daily tasks (for example, deciding what to dabao for dinner is indeed a pressing need), we should take a long, hard look at what we MUST do in order to reap the long-term benefits.

For example, investing. If you’ve been living from paycheck to paycheck, the financial uncertainty of this pandemic may have been a wake-up call, especially if you suddenly find yourself digging through your drawer for misplaced dollar notes. Meanwhile, the friends around you who’ve been investing steadily may be better off with their dividends to tide them through.

Ready to proceed so you can start your resolutions anew? Here are some simple things that you can start doing now to reap the rewards of long-term gains:

1. Eat healthier

This is a given, but how many of us actually persevere with this?

We all know this and the importance of eating healthier to reduce the risks of getting long-term health conditions. An unhealthy or nutritionally deficient diet can lead to a whole host of chronic conditions such as diabetes, kidney failure, high blood pressure, heart disease and even osteoporosis (bone disease).

This could mean more doctor visits to undergo treatment and buy medication, and more financial burden in the long run. MediSave doesn’t cover treatment fully; you still have to co-pay 15% of your bill in cash, which could add up to a lot over time.

Less serious but still as damaging, if you have a weakness for sweet treats, you may also end up at the dentist’s office more often for procedures more pricey than your usual scaling and polishing.

Let’s look on the bright side: It’s easier to eat healthy these days as people and the F&B industry become more health and planet conscious. And who says you must eat bland salads either and feel miserable? There are many healthy food options out there!

2. Get regular exercise

The keyword here is regular. And working out doesn’t mean you need to go full out, running 10km or diving into strenuous HIIT routines a la F45 or the insanity workout.

The World Health Organisation (WHO) recommends for adults aged 18 to 64 to do “at least 150 to 300 minutes of moderate-intensity aerobic physical activity or at least 75 to 150 minutes of vigorous-intensity aerobic physical activity”. This might mean brisk walking, dancing to your favourite K-pop tune, or even going for a little jog with Fido… If cleanliness is your jam, doing household chores will also work up quite a sweat!

Stack those bonuses! Staying fit goes hand-in-hand with eating healthier (point 1) to prevent the onset of chronic conditions and other more serious diseases. There’s also lots of research out there that says leading a healthy lifestyle can help reduce healthcare costs significantly, including this New York Times article stating that even just 30 minutes of walking, 5 days a week, can help you save about $2,500 in medical costs.

3. Make sure you’re insured

Hospitalisation costs are no joke especially if you have chronic diseases (see above points on eating healthy and exercising regularly). To make matters worse, your financial burden goes up if you have no insurance to cover your hospitalisation and treatment costs.

We mentioned MediSave and MediShield alleviating some of the financial burden earlier, but if you’d prefer treatment from a private hospital, it’s best to look for an integrated shield plan to cover the costs. And what if you need long-term disability care in the far future?

For instance, kidney dialysis treatment at home already starts from $1,100 per month. For another condition like cancer, chemotherapy costs begin from $463 and can go up to nearly $2,000. And that’s just for one session.

To avoid making things difficult for yourself in the long run, look into buying insurance for hospitalisation and critical illness now. It’s also better to buy when you’re young and free from any illnesses, so that 1) your premiums can be lower, and 2) the insurance policy can cover you for a variety of medical conditions. If you have pre-existing conditions, you may not be eligible for coverage, or your insurance premiums could sky-rocket.

4. Start investing...early

We cannot stress this enough.

The earlier you start, the better, because you can start building on the power of compound interest. Yes, even if it’s putting aside $100 every month into an investment vehicle rather than letting it rot in your bank account.

These days, there are many types of investment products that you can invest in from exchange traded funds (ETFs) to REITs to meme stocks.

But if you’re looking for an easy way to start investing — think no minimum investment, no lock-in period, and minimal effort, roboadvisors like Syfe are a great starting point. Not sure where to begin? You can’t go wrong with a classic portfolio of stocks, bonds and gold.

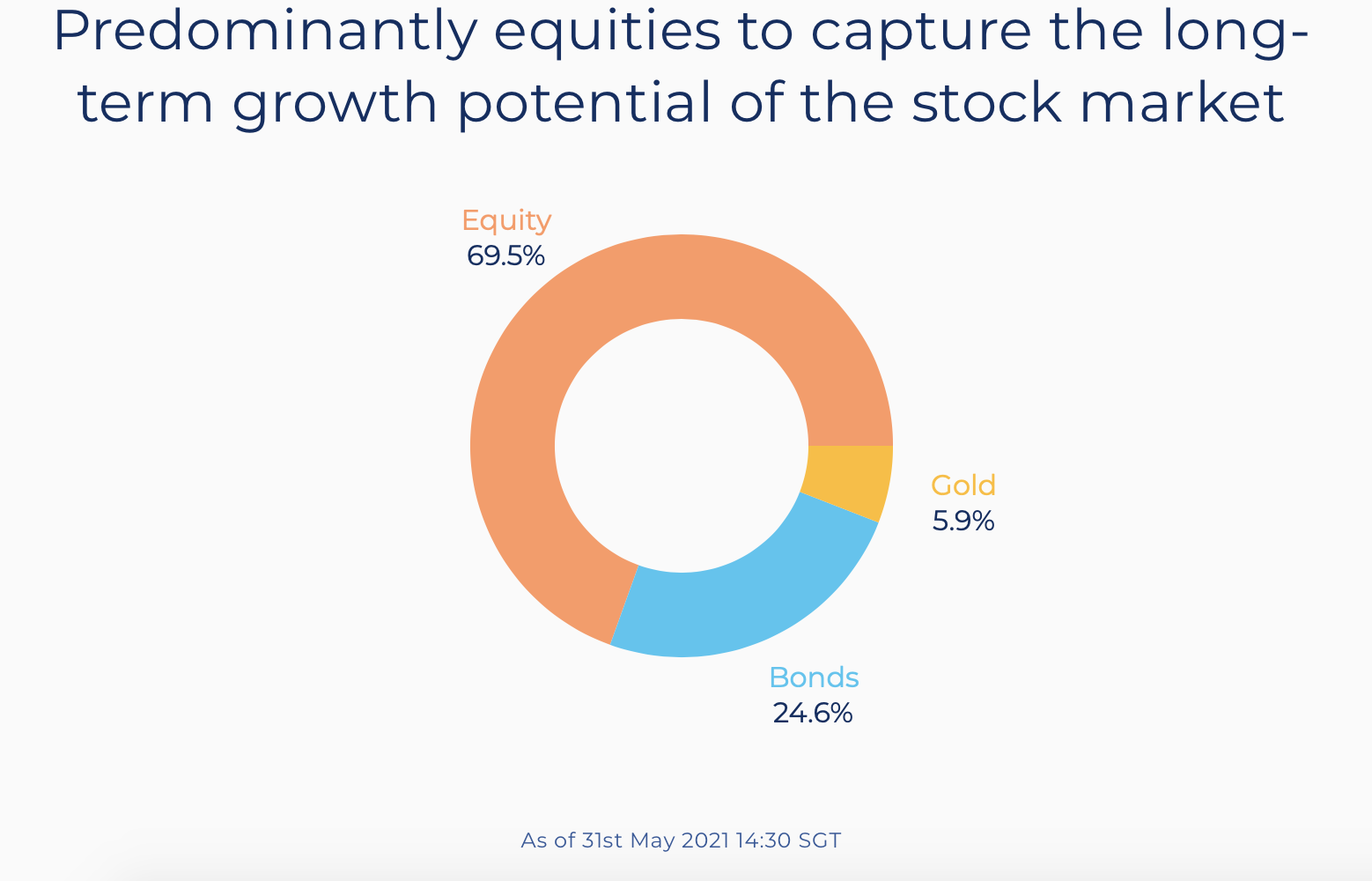

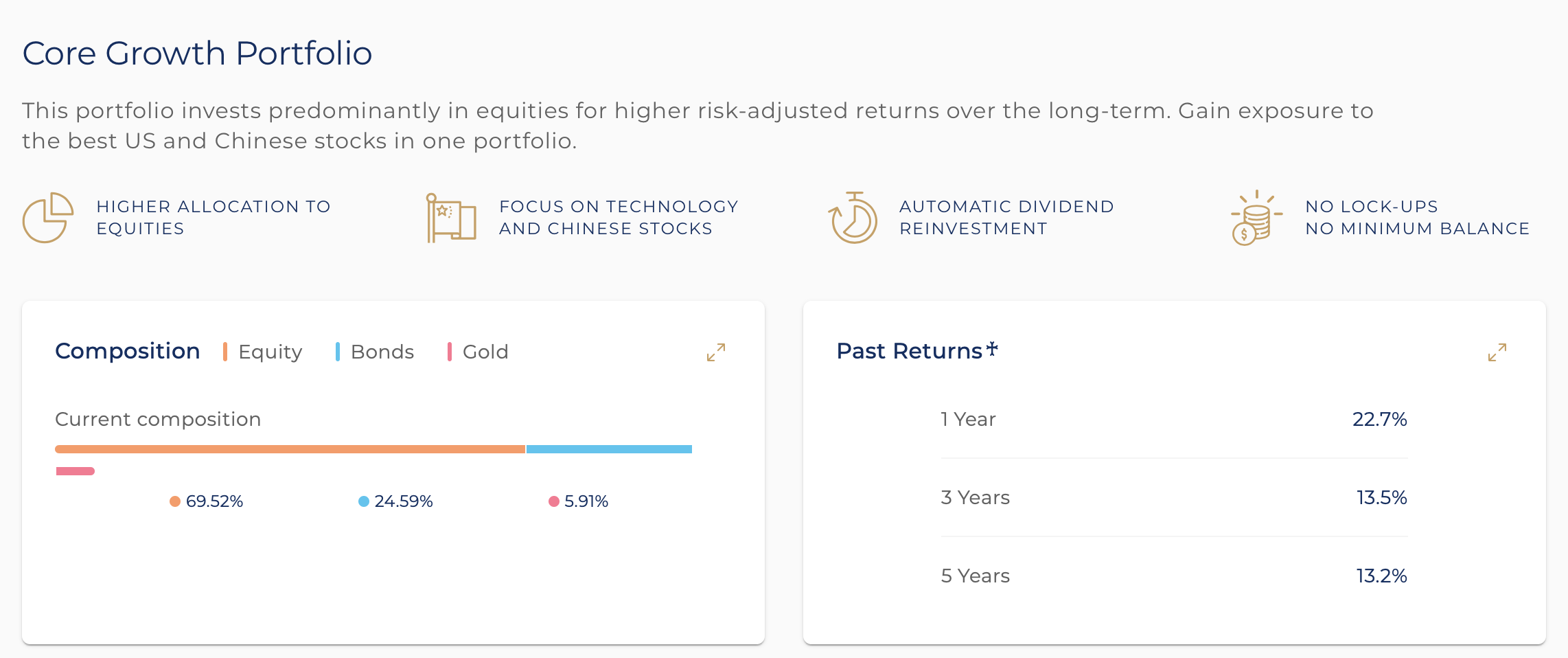

One option is Syfe Core Growth, a portfolio specifically geared for long-term gains. It comprises stock ETFs that give you exposure to more than 3,500 stocks of some of the world’s top performing companies. This includes tech behemoths in the US and China, such as Google, Alibaba, Microsoft, Amazon, JD.com, Tencent and many more.

The basic idea is that, as these companies grow and become more successful over time, you are also sharing in their success through their stock (by buying shares, you kinda own a part of their company).

In addition, the Syfe Core Growth portfolio allocates 24.6% to bonds and 5.9% to gold for diversification. Bonds are known for their stability, while gold seems to do well whenever the economy is down. This portfolio is designed to maximise long-term risk-adjusted returns — which is basically just a fancier way of saying you should be comfortable with market volatility in the short term, but in the long run, the growth of the portfolio will outweigh any short term loss.

TL;DR: Hold long long and you’ll make money in the long run.

Who is the Syfe Core Growth portfolio for?

As it’s designed for long-term gains, Core Growth may not fit if your goal is to make a lot of money in the shortest amount of time. But if you want to build wealth consistently, this portfolio can give high returns — about 11.4% annually over the past 8 years. With the wide geographical exposure to stocks in other countries, it’s also a one-stop shop if you are not too savvy with investing.

It’s also easy to sign up (you can do it through MoneySmart). It takes just 3 minutes using your Singpass and there’s no minimum investment needed.

- Annual Management Fees

- 0.25% - 0.65%

- Minimum Deposit

- S$0

- Platform Fees

- S$0

The best part? You don’t have to monitor your investments every day because the Syfe investment team has developed a smart algorithm that manages your portfolio for you. They automatically rebalance your portfolio and reinvest your dividends so there’s no manual trading required from you.

5. Keep learning

Knowledge is power! No matter what life stage you’re at, investing in yourself by constantly learning new things is a surefire way for long-term gain.

If you are new to all this financial stuff, find out how to get started in investing. Plus, Syfe has free webinars on a range of investing topics, featuring guests like The Woke Salaryman and the team at SGX to share their views.

Want to build your passive income stream? Find out how you can grow it to $1,000 of dividends a month to supplement your salary or extra pocket money for when you retire.

Learning new skills can also be a much-needed boost to your career. If you are looking to “future-proof” your job, seek out skills in growth industries such as manufacturing, tech and biomedical sciences. You can also consider upgrading or complementing your current skillsets with transferable soft skills such as management, negotiation or a cloud computing certification like AWS or Azure.

Learning also keeps your mind sharp and active. Hey, if you’ve always wanted to pursue your dream of becoming a barista, baking extraordinaire or just want to cultivate your own home garden, just carve out the time and go for it now!

No matter what it is, it is never too late to start investing in yourself and plan ahead for long-term gains. After all, you only live once, and you want the financial means and good health to enjoy it.

How about you begin with investing your spare cash? It only takes all of 3 minutes to get started with Syfe. Find out more about the Syfe Core Growth portfolio and sign up here.

Related Articles