In the 3rd instalment of a mini-series on the major robo advisors in Singapore, we’re going to look at AutoWealth, which is probably the 3rd most popular robo advisor after Stashaway and Smartly.

Frankly, it’s hard to tell them apart from one another on a purely theoretical level. Furthermore, they all perform differently depending on how you fund your investment, your risk tolerance, investment goals, etc.

Ultimately, the best way to assess them is to put some money in each one and see which one works out for you.

So, without going into the technicalities of the platform or the performance of my investments, I'm going to simply report what it's like for a novice to use AutoWealth.

Disclaimer: I'm just a pok gai writer. It's a very bad idea to take this article as financial advice.

Some background on AutoWealth Singapore

At first glance, all 3 platforms are kind of same-y. All of them are marketed with the glamour of fancy algorithms, and promise to be cheaper than (yet just as good as) “traditional” investing.

But after a bit of investigation, it should become quite obvious that AutoWealth is quite a different animal from its counterparts.

For a start, AutoWealth has a higher minimum investment amount, different fee structure, a different set of safeguards and a more complex account setup procedure. All these seem to signal that it’s more for serious investors rather than those who just want to play with their money.

So what’s different?

In terms of background, AutoWealth presents as a slightly more legitimate investment company than Stashaway or Smartly.

For example, its founder Ow Tai Zhi is an ex-GIC investment banker, which should be sufficient “pedigree” to Singaporeans awed by government-linked companies… Whereas Smartly was founded by a couple of Estonian dudes, and Stashaway by the ex-CEO of Zalora. (To be fair, Stashaway also has an experienced investment banker as CIO.)

But I’d personally take all this posturing with a pinch of salt. After all, this is a robo advisor we’re talking about; it’s not like the CIO is going to personally manage your fund.

What is AutoWealth’s investment strategy?

As with the other robo advisors, the point of AutoWealth is to grow your funds with the market in general, rather than try to pick individual stocks and assets. This passive long-term approach is shared by all robo advisors, so nothing new here.

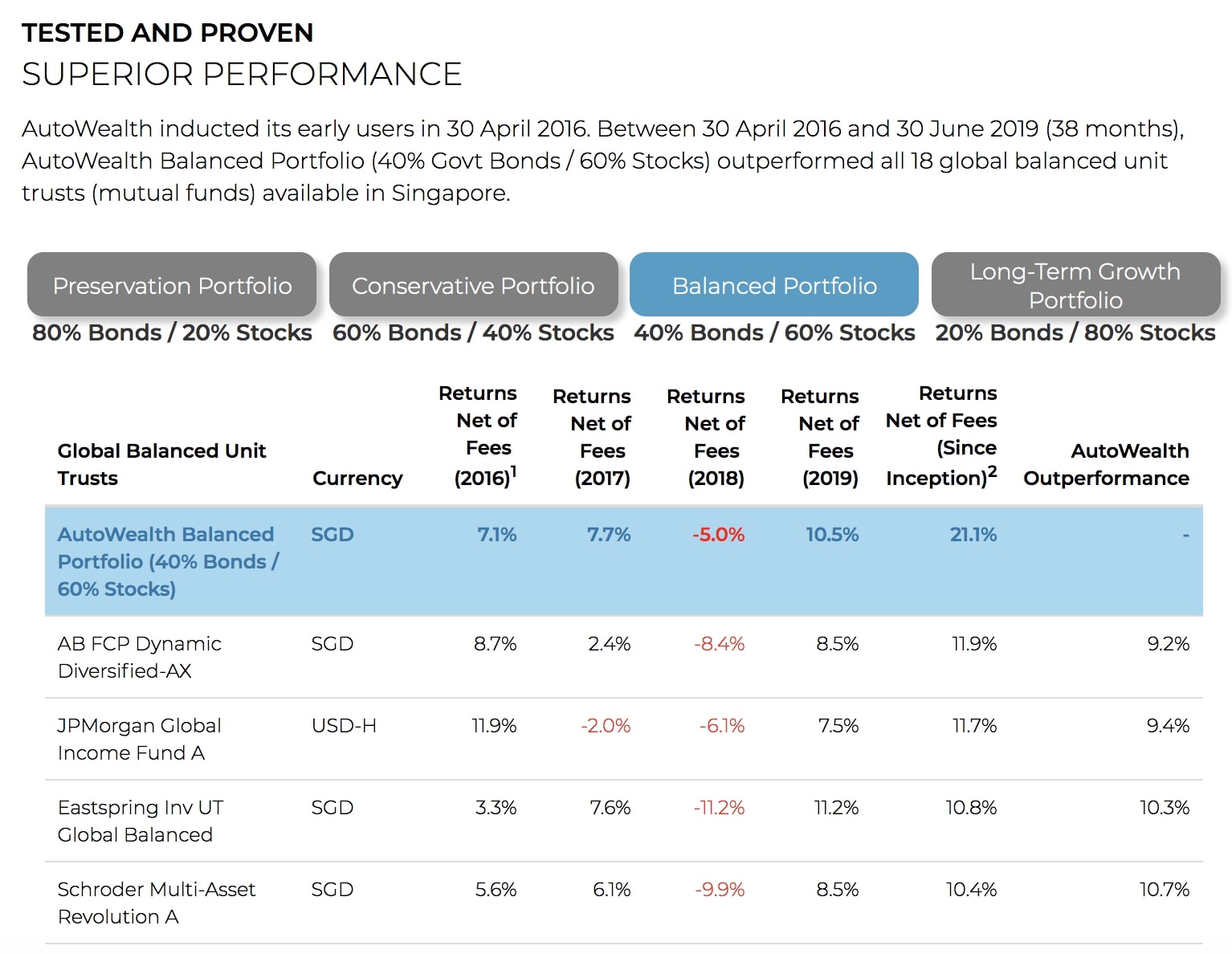

AutoWealth offers 4 main types of portfolios with pre-set ratios of bonds to stocks allocation:

AutoWealth Portfolio | Bonds | Stocks |

Preservation | 80% | 20% |

Conservative | 60% | 40% |

Balanced | 40% | 60% |

Long-term Growth | 20% | 80% |

Stocks correlate to higher risk, higher growth portfolios, while bonds correlate to low risk conservative portfolios. Again, this is pretty common to most robo advisors.

There are only 4 risk levels with AutoWealth, which is a good feature for a robo advisor to have, since the point is that you shouldn’t customise your portfolio too much. This is an improvement over Smartly, for example, which has 10 risk levels to choose from.

Overall, I like AutoWealth’s simple and clear investment philosophy / strategy, because I think it’s important for any investor to understand what’s going on with their money.

Interestingly, AutoWealth also posts the historical performance of their investment portfolios, something that neither Stashaway nor Smartly does. Note that it’s a comparison against traditional unit trusts though, so it’s not a very good metric for choosing between robo advisors.

What are AutoWealth’s fees & minimum investment?

All robo advisors market themselves as low-cost alternatives to traditional unit trusts / mutual funds, where you’d expect to pay at least about 2.5% of your investment in assorted fees. Obviously, that eats into your profits (if any).

While Stashaway and Smartly have a simple one-fee structure, AutoWealth is a bit more complicated.

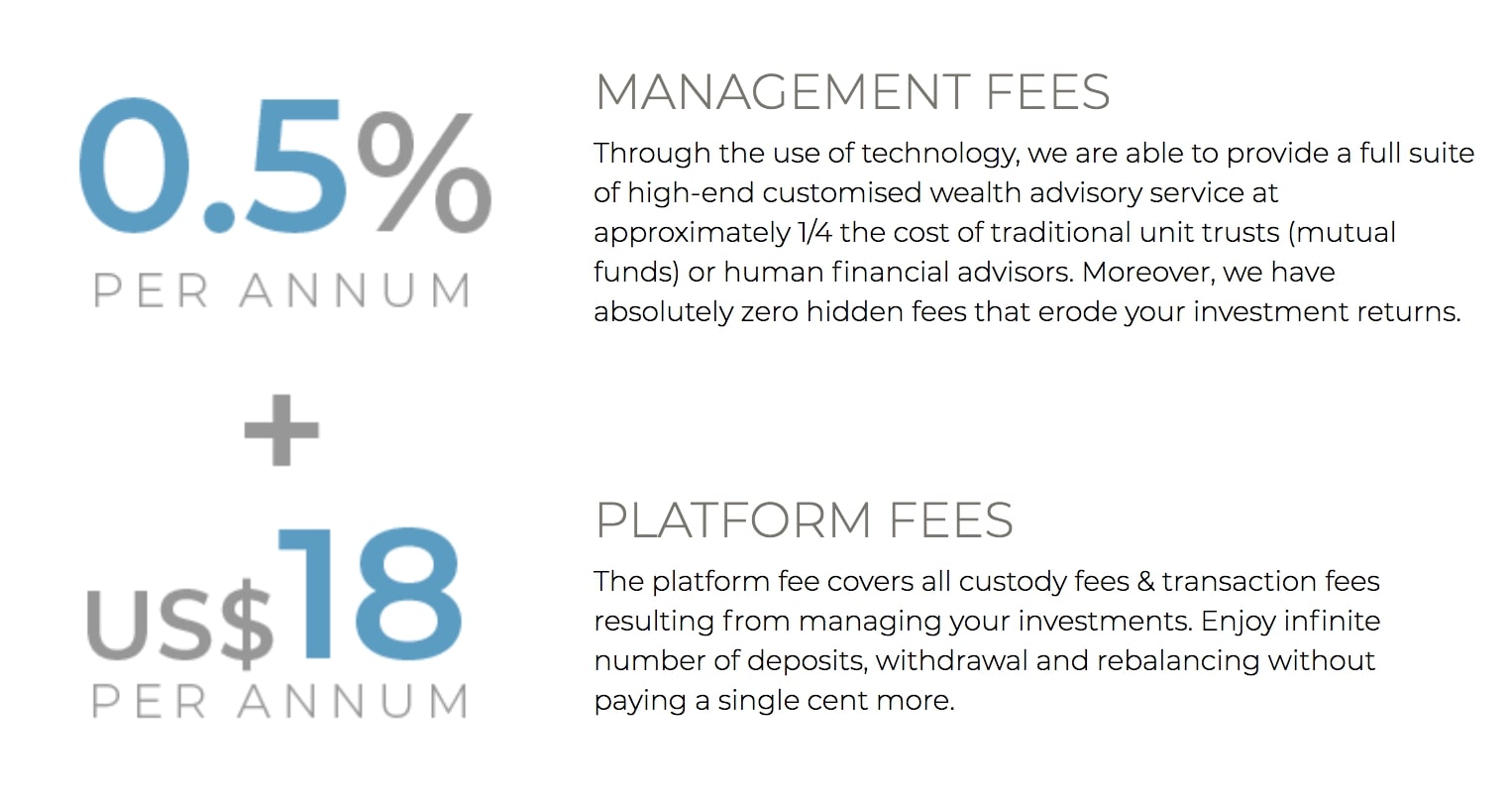

AutoWealth's annual commission is just 0.5% of your investment, but you have to pay US$18 a year to use their platform.

In addition, they have a much larger minimum deposit amount of $3,000, compared to virtually nothing at Stashaway and Smartly. (That said, the $3,000 can be withdrawn at any time with no penalty.)

Here’s a summary:

Robo advisor | Annual fee | Minimum investment |

AutoWealth | US$18 + 0.5% of investment | $3,000 |

Stashaway | 0.8% (up to $25,000) | $0 |

Smartly | 1% (up to $10,000) / 0.7% (>$10,000) | $50 |

So what does that actually look like? As it turns out, AutoWealth actually has the lowest fees among the 3 as long as you’re investing somewhere between $5,000 to $20,000. (For simplicity’s sake, let’s take US$18 = S$25.)

Annual fees for… | AutoWealth | Stashaway | Smartly |

$1,000 investment | — (can’t invest) | $8 | $10 |

$5,000 investment | $50 | $40 | $50 |

$10,000 investment | $75 | $80 | $100 |

$20,000 investment | $125 | $160 | $140 |

TL;DR: If you don’t want / have $3,000 to invest, you can’t invest with AutoWealth. Anything from $3,000 to $5,000, Stashaway may be cheaper, but once you pass the $5,000 mark, AutoWealth is likely to charge the lowest fees.

How do you set up an AutoWealth account?

On paper, AutoWealth ticks all the boxes: It’s founded by someone with investment experience, its investment philosophy is simple to understand, and the fees are very affordable.

But the one area where AutoWealth falls short of both Stashaway and Smartly is ease of setting up an account. Given that robo advisors are supposed to automate investing with the help of technology, it’s a shame that AutoWealth’s account setup procedure isn’t quite so high-tech.

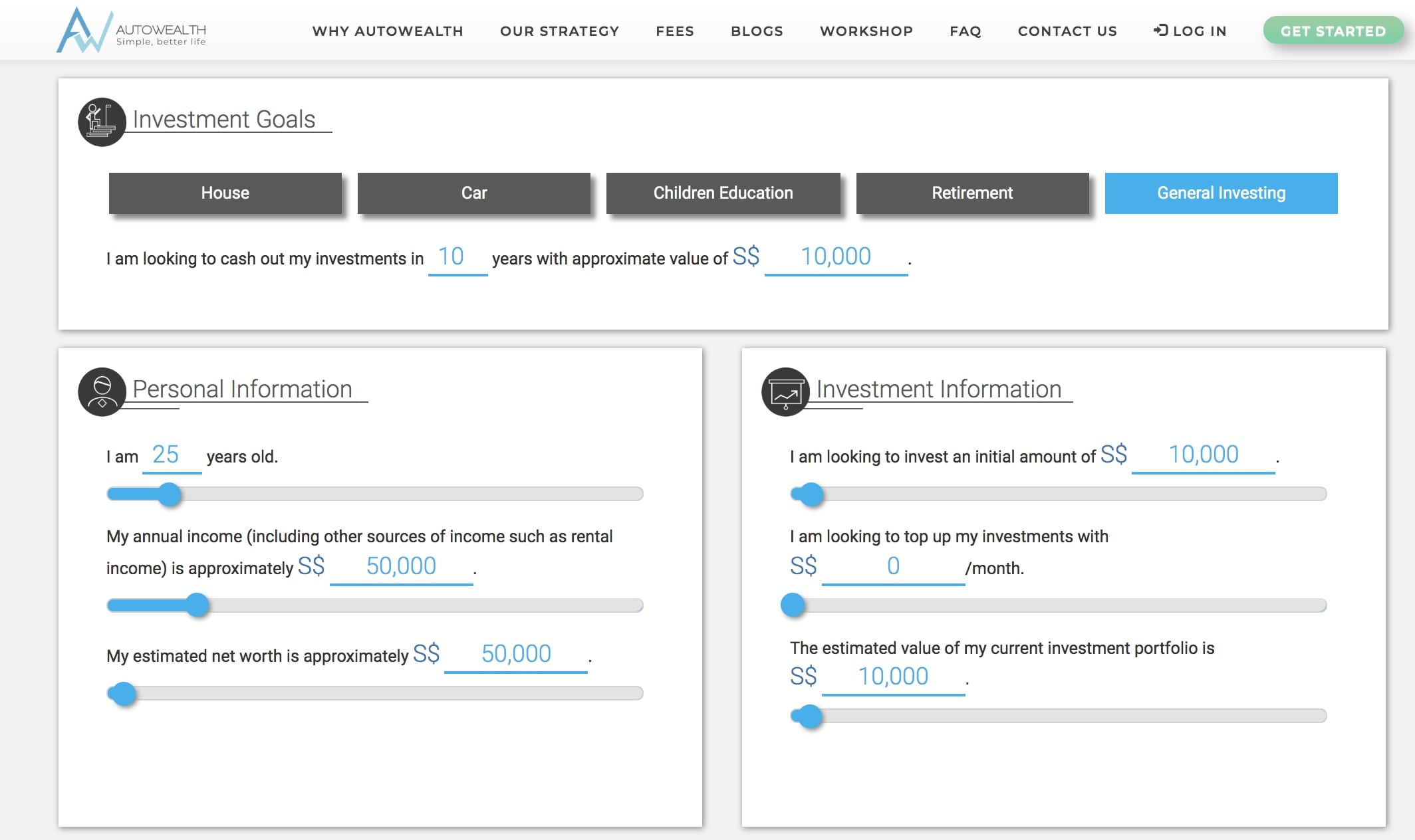

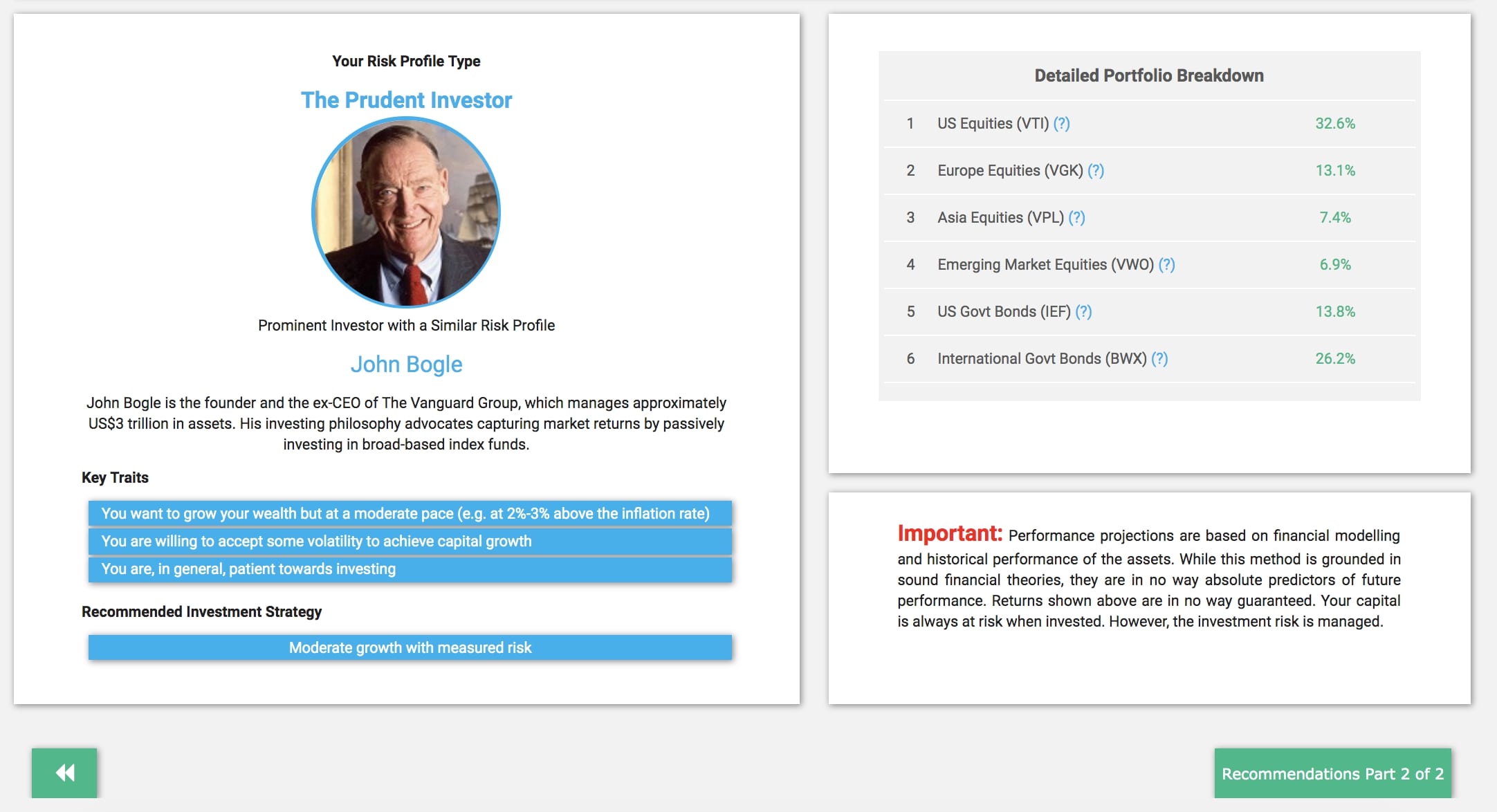

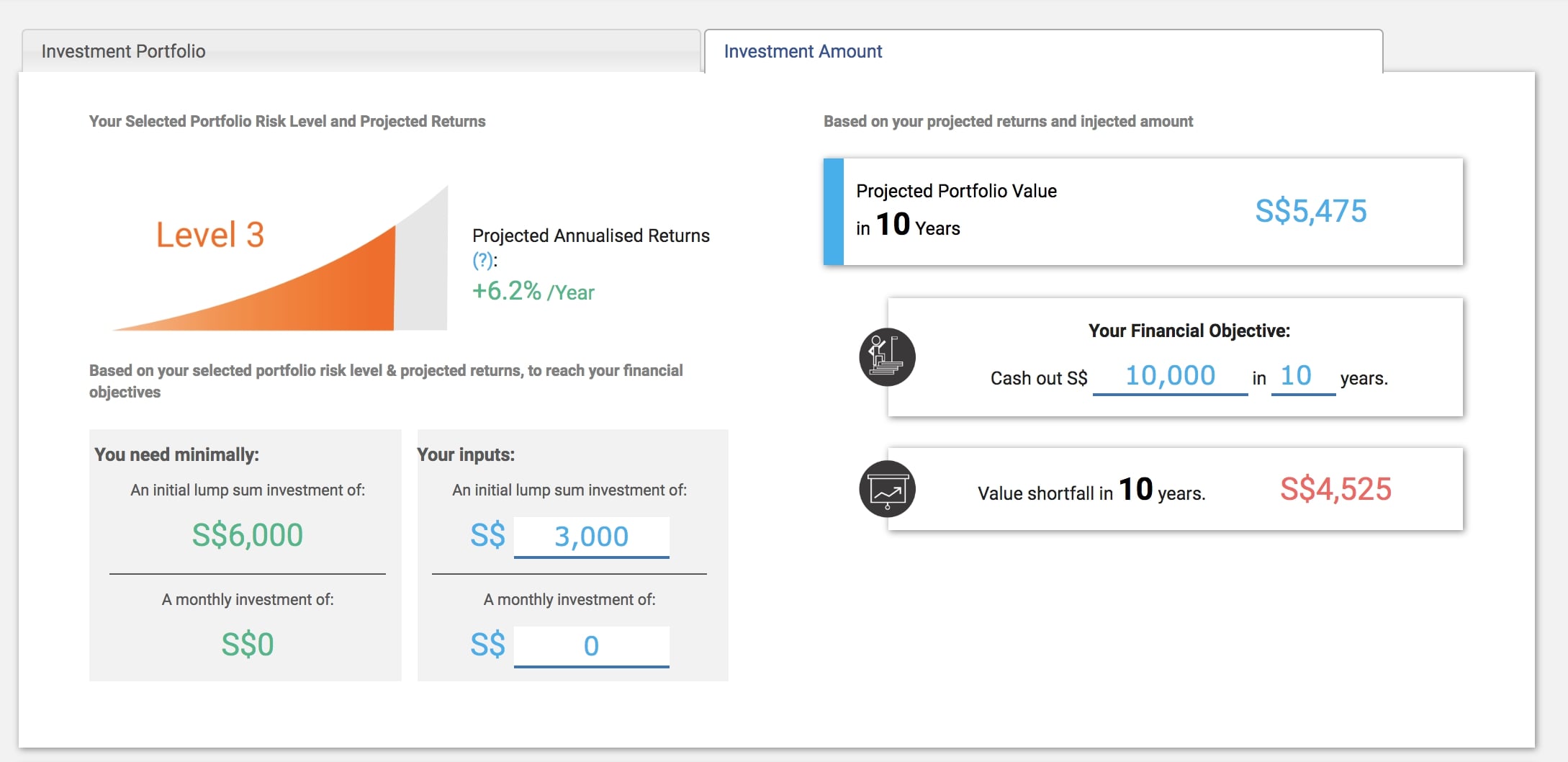

Before you can open an account, you have to go through a goal setting / risk assessment exercise to determine your investment portfolio. AutoWealth will also make recommendations if the projected returns cannot hit the financial goal that you want (if it was specified).

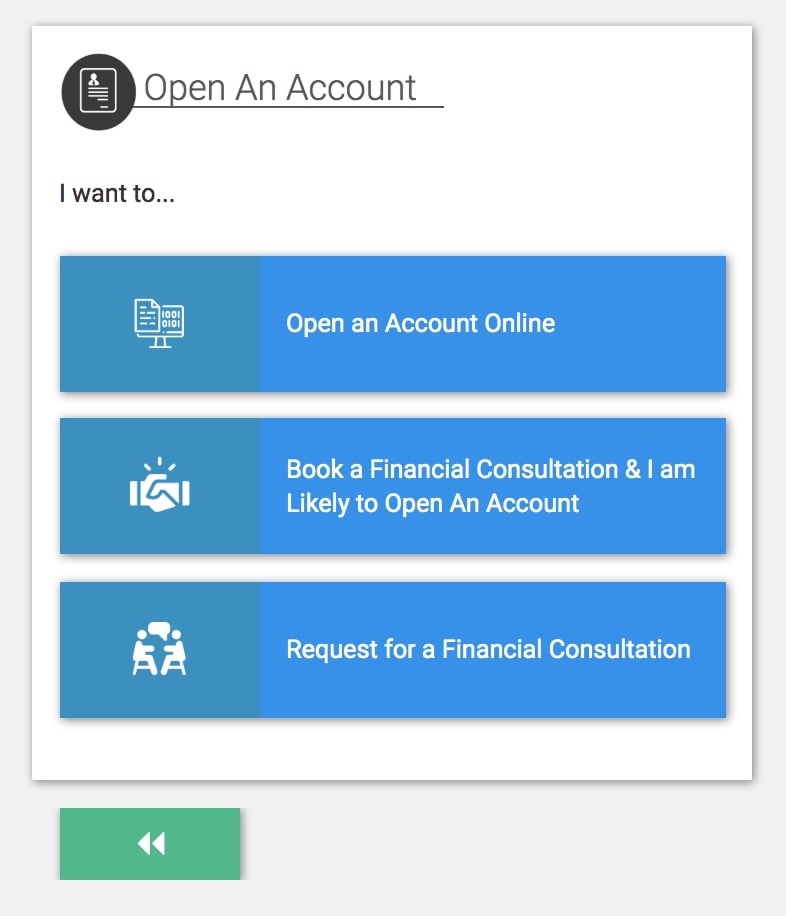

Afterwards, you can opt to open an account online, or arrange for a “financial consultation” with a “wealth manager”. (This turned out to be a WhatsApp chat when I tried it.)

I think the chance to speak to a real person is known as one of the key benefits of AutoWealth, but, actually, Stashaway has this feature too — the “WhatsApp us” button is always hovering around in the app.

In any case, I personally think there’s nothing much a real person can do for you in this case, because ultimately it’s an algorithm that’s handling your investment portfolio.

OK, so what happens after that?

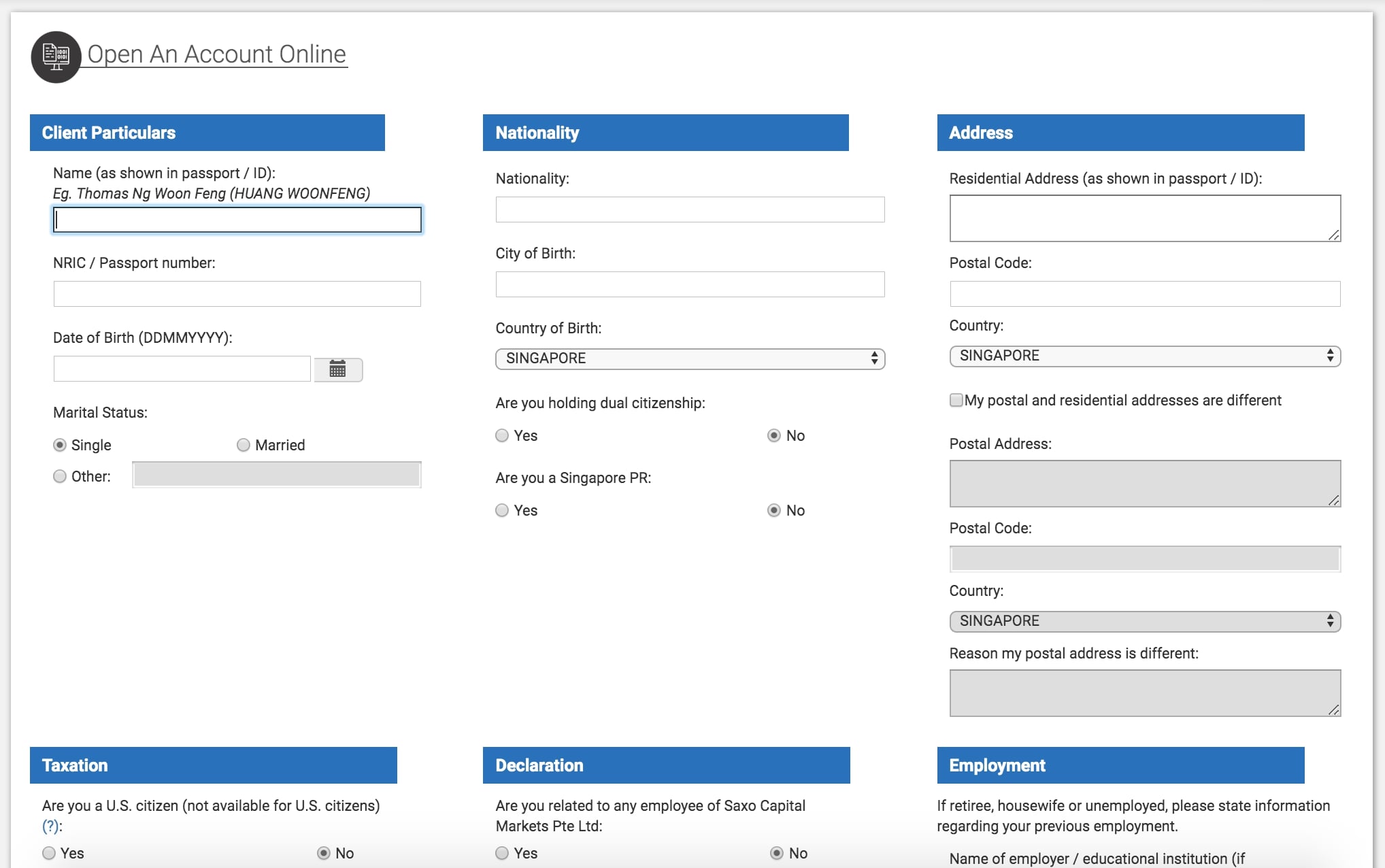

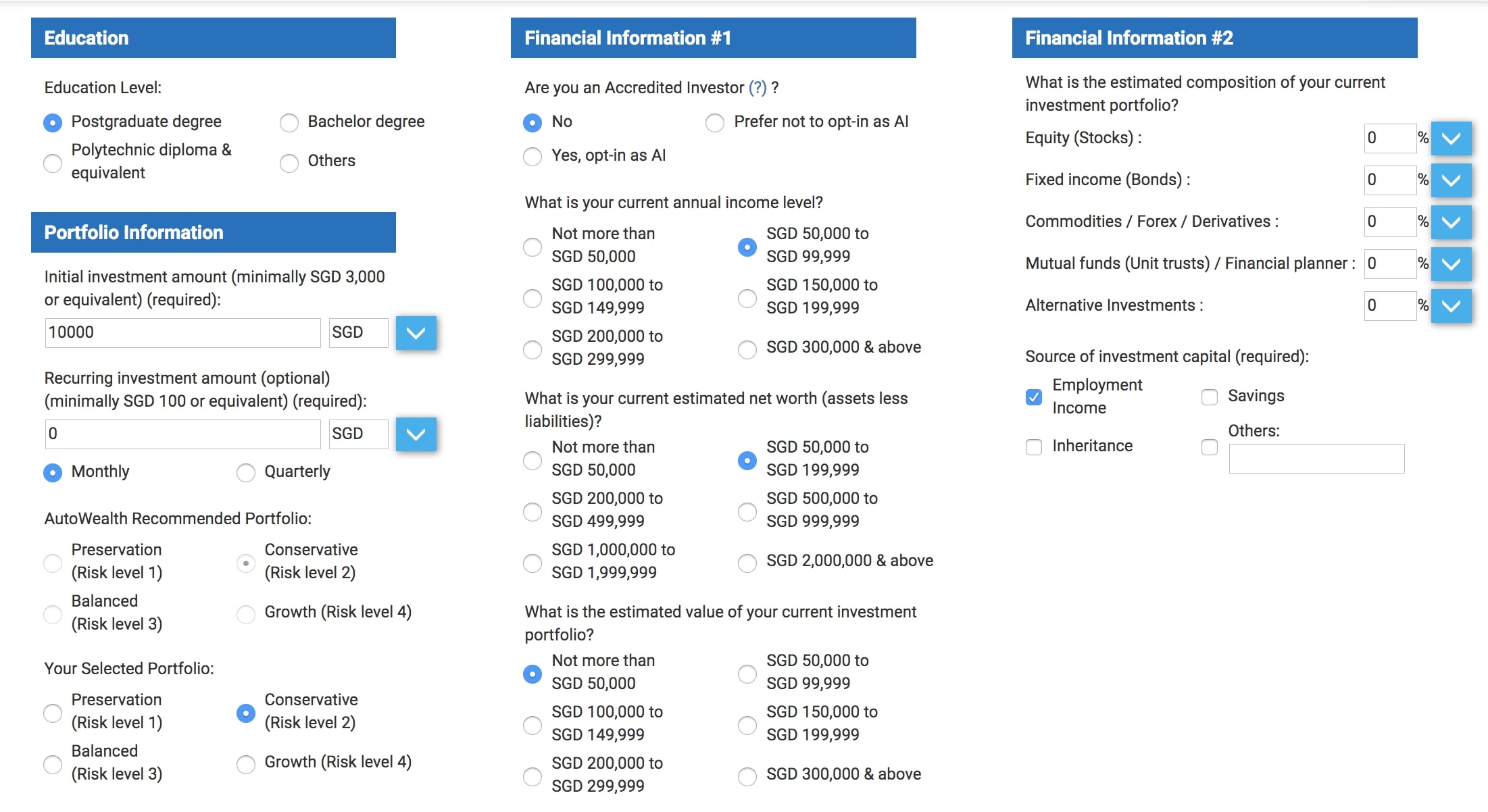

The realAutoWealth account setup procedure happens only after you click through to “Open an Account Online.”

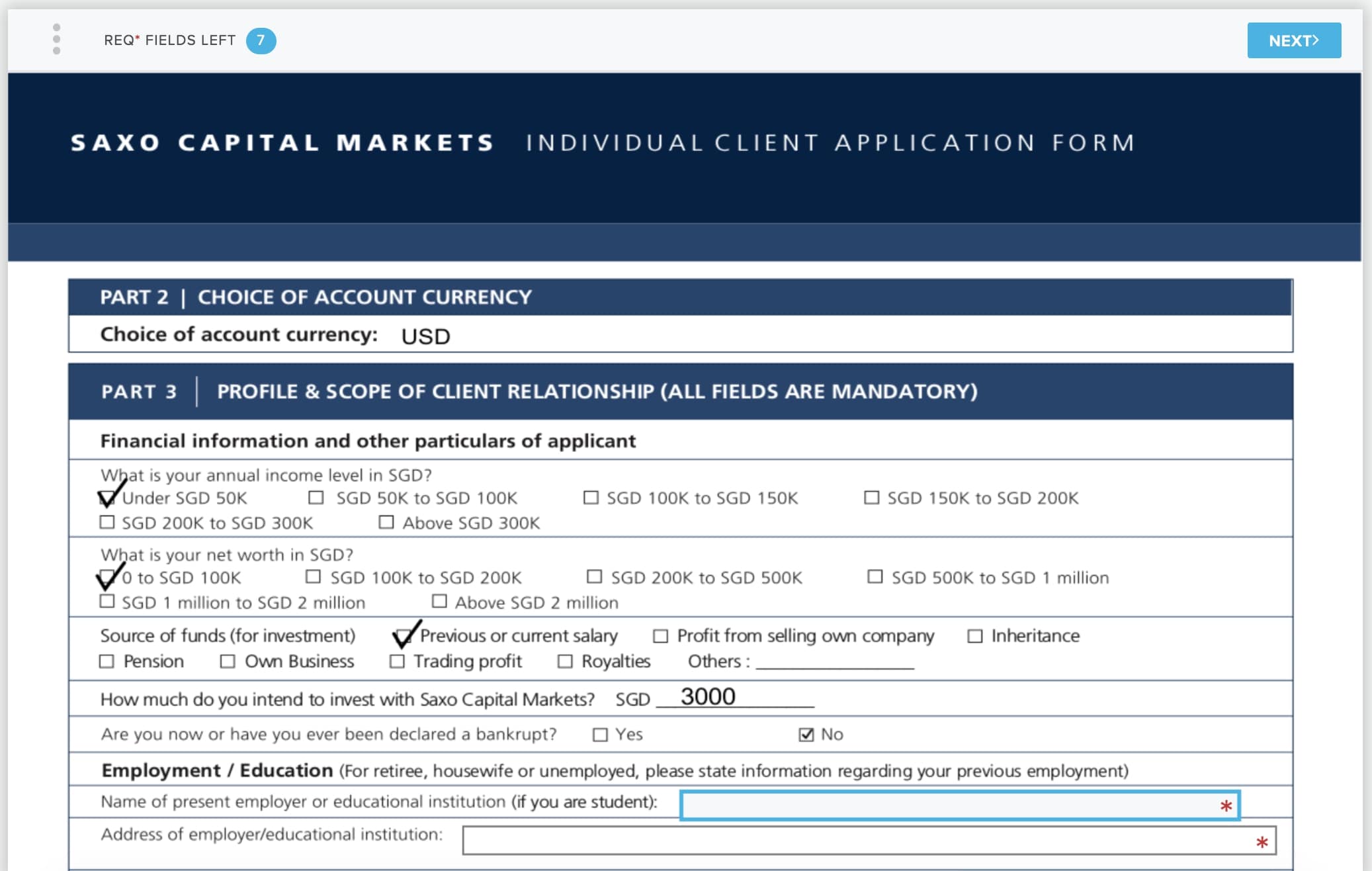

You have to submit a great deal of information here, from your NRIC to residential address to employment details. It’s a LOT more than what both Stashaway and Smartly require.

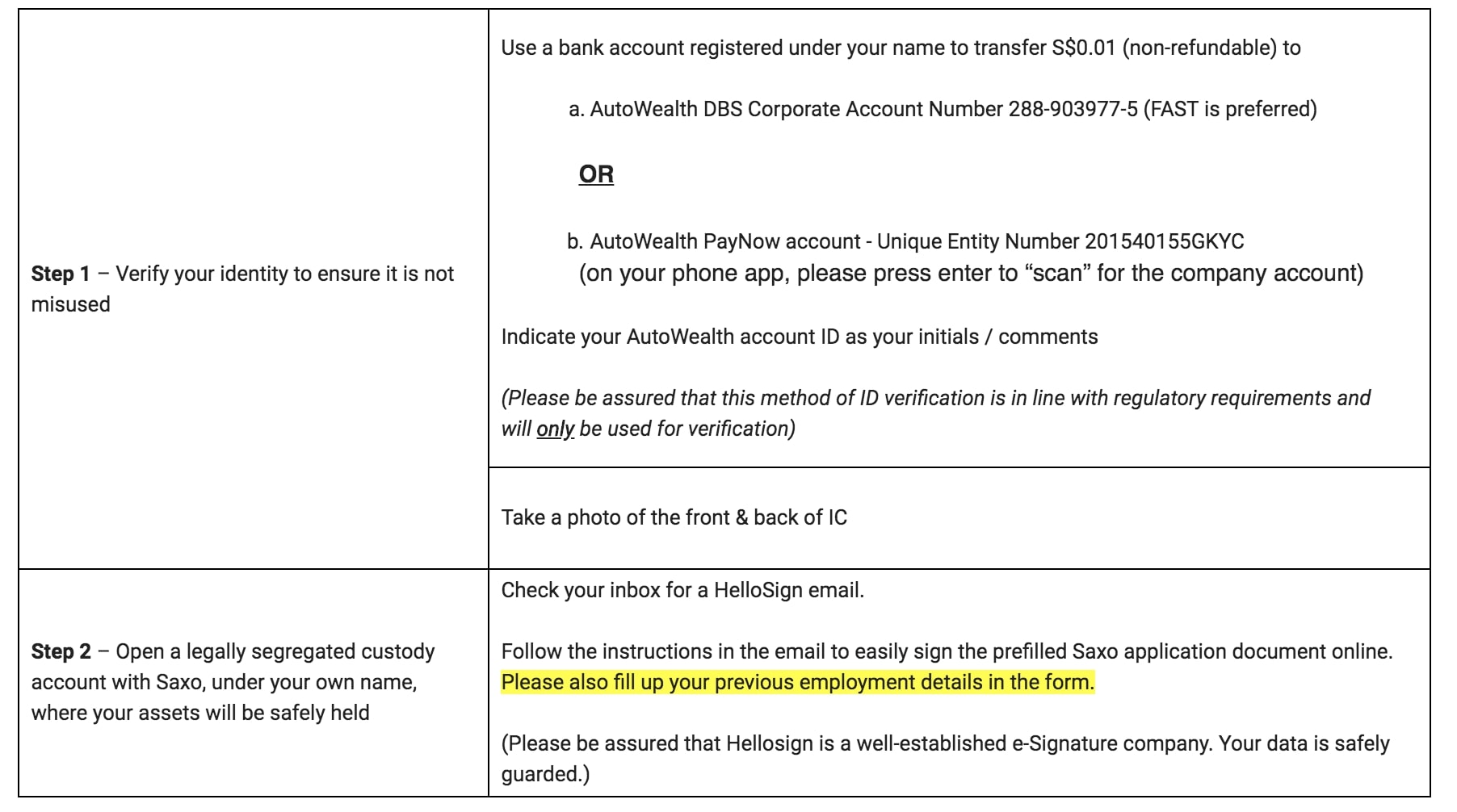

Furthermore, after submitting the online form, you have to get verified by transferring $0.01 (non-refundable) to the AutoWealth bank account and sending in a photo of your NRIC. You also need to sign an agreement with Saxo Capital, the custodian of your funds.

Email from AutoWealth

With PDPA guidelines constantly being hammered into my brain at work, I was a little surprised that AutoWealth wanted to collect this much personal data.

According to the wealth manager I was speaking to (texting), the stringent checks are meant to “prevent money-laundering”. That’s reasonable, but from a regular user’s point of view, it’s still a lot of hoops to jump through compared to, say, the baby-bottom-smooth onboarding process at Stashaway.

Some people might dismiss the sign-up user experience as trivial, but I don’t think I’m alone. Surely I’m not the only person in Singapore to expect a “Netflix” or “Grab” level of intuitiveness and ease of use from their robo advisor?

Wait, what’s this about signing an agreement with Saxo Capital?

When you invest with any kind of investment brokerage, be it a bank-based service like DBS Vickers or something like Phillip Securities / POEMS, the brokerage is not the one holding on your funds or your assets.

Instead, Singapore brokerages typically require you to open a Central Depository Account (CDP account), which allow you to be the legal owner of your shares.

With most robo advisors, though, the investments are held in “custodian accounts” — in this case, the custodian is Saxo Capital.

Saxo safeguards your investments so that, in the event that the robo advisor goes kaput, your assets are still there. It’s also simply good practice to keep customers’ assets clearly separate from that of the robo advisor’s own funds.

- Min. Commission Fee US Stocks

- US$1

- Min. Commission Fee SG Stocks

- S$3

- Min. Funding

- S$0

[SmartRewards | MoneySmart Exclusive]

Get S$180 Cash via PayNow

• OR Apple AirPods 4 (worth S$199)

• OR Sennheiser Accentum Plus Wireless Headphones (worth S$349)

• OR TT Racing Swift X Pro Chair (worth S$429)

OR choose from many more rewards when you deposit a min. of S$3,000, maintain the funds for 30 days, and execute 1 trade within 14 days of account opening.

T&Cs apply.

Use SmartPoints to redeem your favourite product from our Rewards Store today.

While all 3 robo advisors work with Saxo Capital, AutoWealth goes a step further by opening a separate custody account under the individual investor’s name.

That means your assets are not held in a communal trust (as with Stashaway and Smartly), but are tied to your legal name. Supposedly, this makes it easier and quicker to get your assets back in a scenario where the robo advisor becomes insolvent.

While I can’t say for certain that this is the case, it’s just good to know what you’re getting out of the extra administrative work you put into setting up your AutoWealth account.

Soo… Is AutoWealth any good?

There are some things I like about AutoWealth. For a start, it has some of the lowest fees (among the big 3 robo advisors) for small-time investors (up to $20,000). With long-term passive investing, low fees are key to maximising your profit.

AutoWealth also seems more secure against insolvency / bankruptcy than the other robos. Although more troublesome, the payoff is that your assets are held in a personal custodian account rather than a communal one.

I think my only real objection is that it's a pain in the ass to set up an account, compared to Stashaway and Smartly.

Don't get me wrong; I don't think it’s a bad thing that AutoWealth has higher barriers to entry. As I’ve mentioned in previous reviews, these robo advisors, while seductively easy to use, actually play in an intermediate investment space. They invest in USD and expose you to global stocks, bonds and commodities, which are things that a complete investing novice may not understand the risks of.

But I think the user journey, design and consumer-facing copy could be a lot more user-friendly and pleasant to use, considering it’s a digital-first investment platform. In that area, AutoWealth has a lot to learn from Stashaway.

Have you used AutoWealth to invest your money? What do you think of it?

Related Articles