Gig workers are the “most financially stretched” group in Singapore, according to a 2023 DBS study. With expenses outpacing income, the average gig worker spends 112% of what they earn every month—far higher than the 57% spent by the typical salaried worker.

It’s a tough balancing act, especially as savings continue to shrink. By May 2023, the median gig worker had just 1.7 months’ worth of expenses saved, down from 1.9 months the year before and well below the 3.5 months saved by most Singaporeans. DBS recommends at least 12 months’ savings for those with unpredictable incomes—a target that feels out of reach for many.

With all this financial juggling, getting approved for a credit card might seem impossible. But the right credit card can actually help gig workers smooth out cash flow, earn useful rewards, and be better prepared for emergencies—if you know where to start.

Credit cards for gig workers in Singapore (2025)

- Challenges gig workers face with credit cards

- Eligibility criteria: How can gig workers get a credit card?

- Tips to improve credit card approval odds for gig workers

- The best credit cards for gig workers in Singapore (2025)

- Conclusion

1. Challenges gig workers face with credit cards

Gig workers are people who earn money from short-term, flexible, or on-demand jobs rather than a fixed salary. Examples include freelancers, commission-based sales agents, private-hire drivers, delivery riders, and part-time tutors.

For many gig workers, getting approved for a credit card isn’t easy. Here’s why:

Irregular income and lack of payslips

Most gig workers don’t have the luxury of a fixed monthly salary. Your income might change week to week, depending on the jobs you take. This makes it tricky to provide the regular payslips or consistent proof of income that banks usually want.

Traditional banks’ hesitance with non-salaried applicants

Many banks still prefer full-time employees with stable jobs. If you’re self-employed or working gigs, banks may see you as a higher risk. This can mean stricter eligibility requirements, longer approval times, or lower credit limits—even if you’re a responsible spender.

Higher financial stress and more credit risks

When your income isn’t predictable, it’s harder to keep up with monthly payments or clear your credit card bills in full. Even a short dry spell can lead to late payments, extra fees, or mounting interest. Without a steady financial cushion, missing a payment can hurt your credit score and make it even harder to qualify for cards or get good credit limits in the future.

2. Eligibility criteria: How can gig workers get a credit card?

Getting a credit card as a gig worker in Singapore is definitely possible—but there are a few important hoops to jump through. To get approved, you’ll need to:

- Meet the income requirements—MAS sets minimum income guidelines that banks generally stick to, but they can also offer credit cards with lower income requirements and a strict credit limit of $500.

- Pass additional checks by the bank—every bank has its own way of assessing applications, and may ask for extra proof of income flows and employment status.

- Submit the relevant documents—ensure these are timely and up-to-date so that banks can verify your financial standing and accurately assess your eligibility.

Income requirements for gig workers applying for a credit card

Depending on your age, these are the MAS guidelines for credit card eligibility. These apply to everyone, whether you’re salaried, self-employed, or working gigs:

Age group | Minimum annual income | Alternative options |

Up to 55 years old | $30,000 | Net personal assets > $2 million, or net financial assets > $1 million |

Above 55 years old | $15,000 | Net personal assets > $750,000, or guarantor with annual income ≥ $30,000 |

Note: “Income” can include non-employment income such as rental or investment income. If you use a guarantor, your credit limit will be based on the guarantor’s income.

While the Monetary Authority of Singapore (MAS) generally requires a minimum annual income of$30,000 for most unsecured credit cards, it allows for exceptions in certain cases—particularly for cards with low credit limits. Banks can offer cards with a maximum credit limit of $500 to applicants who do not meet the $30,000 income threshold. This helps those who are new to credit, have variable income (like gig workers), or lack a credit history to safely access credit without taking on excessive debt.

Additional checks by the bank: What else do banks look for?

Banks will usually go a step further. On top of MAS rules, they’ll assess your annual income, check for a stable source of funds, and review your credit history.

Most banks assess your application based on:

- Minimum annual income: Many banks require gig workers to have a higher minimum annual income of $40,000 instead of the $30,000 minimum required for salaried workers.

- Proof of income: Since regular payslips aren’t an option, you’ll need alternative documents.

- Credit history: A good credit score and timely bill payments always help.

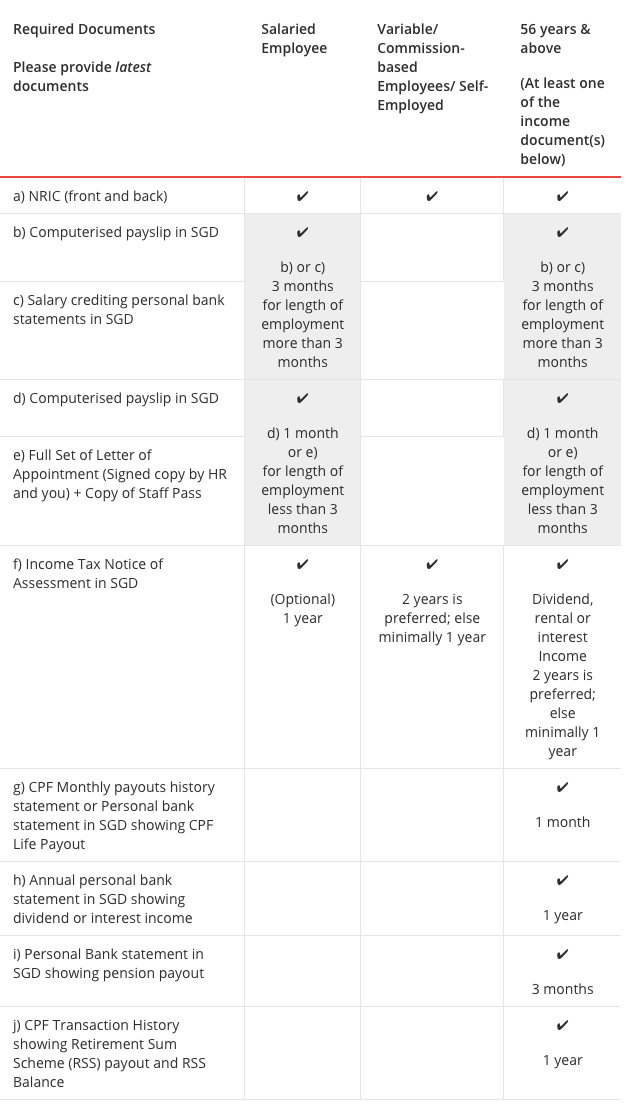

Documents gig workers can use

Unlike salaried employees, gig workers don’t have monthly payslips—but banks accept a range of alternative documents to prove income and financial stability. When applying, gig workers can typically submit documents such as:

- Income Tax Notice of Assessment (usually 1–2 years): Essential for showing annual income, especially for variable or commission-based workers.

- Latest 12 months’ CPF contribution history statement: Especially useful if you make regular CPF contributions as a self-employed person.

- Bank statements (usually last 3 months): Personal bank statements showing your income deposits, including commission payments, gig income, or regular transfers.

- Computerised payslips (latest 1–3 months): If you receive any payslips (for part-time or commission work), include these.

- Company letter certifying employment/income (dated within 3 months): Especially for those with a new employment of 3 months or less

- Annual bank statement showing dividend or interest income: For those who supplement gig income with investment returns.

- CPF monthly payout statement, personal bank statement showing CPF Life payout, or pension payout: Especially relevant if you’re over 55 or semi-retired.

Exactly which documents are required depend on your type of employment and citizenship status. Foreigners need to submit more documents than Singaporeans and PRs. Here’s a sample credit card application checklist from DBS for reference:

Image: DBS

3. Tips to improve credit card approval odds for gig workers

Getting a credit card as a gig worker can be challenging, but these simple tips can boost your odds.

Watch your balance-to-income (BTI) ratio

Under MAS regulations, your total unsecured credit limit—including all your credit cards and personal loans—cannot exceed 12 times your monthly income. If your combined outstanding balances go over this limit for 3 months in a row, all your credit card and unsecured credit accounts could be suspended. This means you won’t be able to charge new amounts, request higher limits, or apply for new cards until you bring your balances down. Always keep an eye on your overall borrowing to stay in good standing.

Pay off outstanding debts first

When you apply for a new credit card, banks will review your existing loans and credit card balances. By paying down your current debts, you’ll lower your balance-to-income ratio, boost your credit score, and show banks that you’re a responsible borrower who can handle credit wisely. This not only increases your approval odds, but also helps you qualify for better credit limits and interest rates in the future.

Don’t apply for too many cards at once

According to Bankrate, every credit card application triggers a hard inquiry on your credit report, which can temporarily lower your score. There are no strict rules on timing, but it’s wise to wait 3 to six 6 between applications—or until your credit score has improved to the next tier—before trying again. This helps you look like a more reliable borrower and improves your chances of approval.

Submit documents that are up to date

When applying for a credit card as a gig worker, it’s essential to provide the most recent copies of your CPF statements, bank records, and tax documents. Banks rely on up-to-date paperwork to confirm your current income and financial stability. Submitting recent documents helps speed up the approval process and reduces the chances of delays or requests for additional information.

Build your credit score

Your credit score is a key factor banks use when deciding whether to approve your card application. To grow your score, make sure you pay all your bills—credit cards, loans, utilities—on time, every time. Even a single missed payment can hurt your score. Keeping your credit usage low and clearing outstanding balances regularly also boosts your score, making it easier to qualify for credit cards and get better terms in the future.

4. The best credit cards for gig workers in Singapore (2025)

With so many credit cards out there, it’s important for gig workers to focus on what really matters for their unique situation. Here are three key factors to consider before picking a card:

- Flexible eligibility requirements: Choose cards that accept alternative income documents, making approval easier for gig workers.

- Low fees and manageable interest: Opt for cards with minimal fees or flat-rate charges to avoid extra costs during slower months.

- Rewards and benefits that match your lifestyle: Pick cards that offer cashback or perks on everyday spending like transport, dining, and online shopping.

Bearing these in mind, here are my top credit card picks for gig workers.

GXS FlexiCard

The GXS FlexiCard is Singapore’s first credit card with a flat monthly fee—no interest charges—making it a smart pick for gig workers with variable income. Designed for those new to credit or lacking credit history, it offers a $500 limit and no income requirement. Enjoy unlimited instant cashback (up to $3 per $10 spend), no foreign transaction fees, and flexible repayments with just a $5 fee if you can’t pay in full.

Why it’s good for gig workers: No income requirement and flat fees mean even those with unpredictable earnings can access credit without worrying about mounting interest charges.

Why it’s not so good: The low $500 limit may be too restrictive if you need a higher credit line for larger or more frequent purchases.

CIMB AWSM Card

The CIMB AWSM Card is a standout for young gig workers, thanks to its low minimum income requirement—just $18,000 a year for applicants under 35. It offers unlimited 1% cashback on dining, entertainment, online shopping, and telco bills, with no annual fees. Open to Singaporeans and PRs, it’s a great starter card for those just building their income and credit history.

Why it’s good for gig workers: Lower income threshold makes it much more accessible for younger gig workers just starting out.

Why it’s not so good: While the cashback is unlimited, the cashback rate is only 1%. You can get higher rates with select debit cards, as you’ll see below.

DBS Visa Debit Card

Though not a credit card, the DBS Visa Debit Card stands out for gig workers who want strong rewards without the risk of borrowing. You’ll earn 4% cashback on online food delivery, 3% on local transport, and 2% on overseas spending. To unlock these perks, spend at least $500 per month, with a $20 cashback cap and a $400 monthly withdrawal limit. Perfect for everyday spenders who want great rewards, not credit.

Why it’s good for gig workers: No income requirement (it’s a debit card after all) and lets you enjoy generous cashback on daily essentials with no risk of debt or interest charges.

Why it’s not so good: If you need the credit facility of a credit card (i.e. you need to borrow money), this card won’t do you good. Plus you won’t build a credit history since it’s not a credit card.

ALSO READ: The Best Debit Cards in Singapore (2025)

5. Conclusion

Gig workers in Singapore face real financial challenges, but getting the right credit card—or even a rewarding debit card—is possible with a little know-how. Remember to look for cards with flexible eligibility, manageable fees, and rewards that fit your lifestyle. Always submit up-to-date documents, keep your borrowing healthy, and focus on building your credit score over time.

Ready to compare more options or find the card that’s truly right for you? Visit MoneySmart’s credit card comparison page for the latest offers.

This article was first drafted with the help of AI and later reviewed and refined by the author.

Related Articles