Some things in life just work better in pairs—like a good book and a rainy afternoon, or coffee and a quiet morning. In the world of credit cards, the right pairing can be just as satisfying. Choose wisely, and you’re not just doubling your perks—you’re creating a tag team that covers each other’s blind spots and boosts your rewards game to new heights.

Whether you’re chasing cashback, stacking miles, or racking up rewards points, certain credit cards make far more sense together than apart. Think of them as the dynamic duos of your wallet, ready to turn every spend into a bigger win.

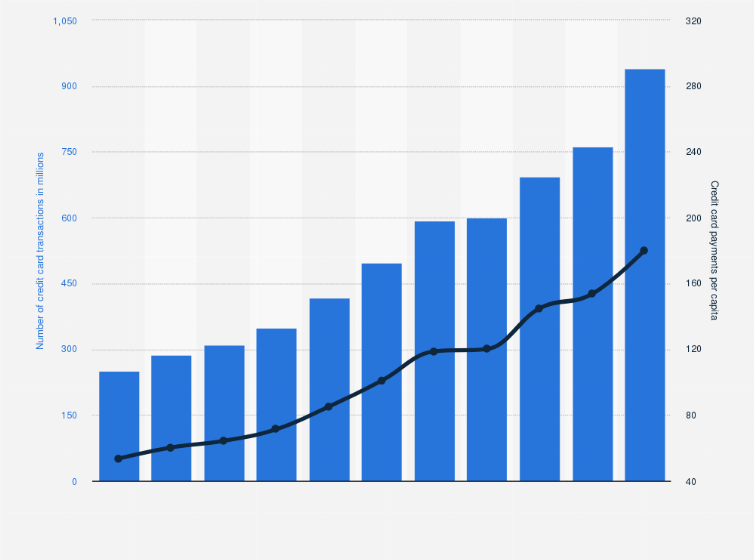

Why is this important? Credit card payment is the most common mode of payment in Singapore at a 80% penetration rate according to Singapore Business Review. Just look at how the volume of credit card transactions has grown from 2013 to 2023:

Image: Statista

Why credit cards? For most people, the draw is simple—convenience and rewards. Cash might be straightforward, but it doesn’t give you anything back. Pay with a credit card instead, and you can earn rebates or rewards on the spending you’d be doing anyway.

But if there’s another thing that Singaporeans like, it’s efficiency. Some credit cards work better together to compliment your spending habits and rebate goals. Which credit cards pair best with other credit cards? Across earn rates, earn categories, and minimum spends, there’s a lot to consider. So let us do the leg work for you. After comparing dozens of credit cards, here are my top credit card pairings I’d recommend in Singapore for cashback, miles, and rewards.

1. TL;DR—Summary of the best credit card pairings in Singapore

Here’s a summary of the credit card pairings I’ve picked out. For the cashback, miles, and rewards pairings below, I found that UOB and Citibank credit cards tend to pair well together.

Best cashback credit card pairing: UOB EVOL Credit Card + Citi Cash Back+ Card or OCBC INFINITY Cashback Card

Cashback credit card | Bonus rebate | Why they are a great combination |

10% cashback on online, mobile contactless, selected gym, telco and streaming spend | The UOB EVOL credit card gives you a capped 10% cashback. After you hit $800 spend on this card, use a fuss-free unlimited cashback card like the Citi Cash Back+ Card or OCBC INFINITY Cashback Card to earn 1.6% cashback. | |

1.6% unlimited cashback |

Best miles credit card pairing: UOB PRVI Miles Card + Citi PremierMiles Card

Miles credit card | Bonus rebate | Why they are a great combination |

UOB PRVI Miles Card (Mastercard / VISA / Amex) | – 8 miles per $1 spend (UNI$20 per S$5 spend) on major airlines and hotels booked through Expedia and Agoda | For your plane tickets, use the UOB PRVI Miles Card to earn 8 mpd on airlines when you book through Expedia or Agoda. For accommodation, use the Citi PremierMiles Card for 10 Citi Miles per S$1 spent on Kaligo or 7.2 Citi Miles per S$1 spent on Agoda. |

– 10 Citi Miles per S$1 spent on Kaligo |

Best miles credit card pairing: UOB Lady's Card + Citi Rewards Card

Rewards credit card | Bonus rebate | Why they are a great combination |

– 10X Points for online purchases (online grocery, food delivery, ride-hailing and more) | Earn bonus rebates on up to $2,000 monthly spend between these 2 cards. The Citi Rewards Card offers a large range of bonus categories, while the UOB Lady’s Card gives you the flexibility to choose your bonus category each quarter. Both have the same earn rate of 4 mpd on bonus earn categories. | |

– Up to 25X UNI$ per $5 spent on your preferred rewards category |

Before we proceed, I want to be upfront about some assumptions I’m making in this article:

- You’re only getting 2 credit cards for one rebate category.

- You’re focused on only the rebate benefits of these 2 cards, even though many come with other benefits too, such as lifestyle deals, lounge access, and complimentary travel insurance.

- Cashback/miles/rewards are your priority over credit card promotions. (But do check those out; they can be very generous!)

- You are eligible for at least entry-level credit cards, which usually require that you draw an annual income of $30,000 (for Singaporeans) or $40,000 – $45,000 (for non-Singaporeans). This list will only include entry-level cards.

- There are 3 main rebate categories:

- Cashback: You earn cashback on your spending that is either automatically offset in the same or next month’s statement or that you can redeem to offset your next statement.

- Miles: You either earn miles directly or rewards points that can be redeemed for miles. Either way, these cards are optimised to earn you miles for your travel spending, especially on spend categories like flights and hotels.

- Rewards points: You earn rewards points that can be redeemed for lifestyle deals, miles, and more.

- You’re not trying to max out any specific spend category such as food delivery or Grab rides. The cards below are catered for general spending and will include broad spend categories. There are other credit cards out there with higher rates for specific categories.

2. Best credit card pairings for cashback

Cashback credit card | Bonus rebate | Minimum monthly spend | Monthly cap on bonus category |

10% cashback on online, mobile contactless, selected gym, telco and streaming spend | $800 | $80 (but I suggest you DON’T max this out—see why below) | |

1.6% unlimited cashback | $0 | No limit |

UOB EVOL Credit Card

- on Local Online, Mobile Contactless, Telco, Gym, Streaming spend

- 10% Cashback

- FX Fees on overseas FX spend worldwide, with no min spend, no cap

- 0%

- Min. Spend per month for 10% cashback

- S$800

Often, the cards that will earn you the highest cashback limit you to just 1 or 2 spend categories. That isn’t the case with the UOB EVOL Credit Card, which doles out a generous 10% cashback rate on online, mobile contactless, and overseas in-store foreign spend.

UOB EVOL cashback | Cashback cap per statement month |

10% cashback on Online Spend and Mobile Contactless Spend | $30 ($300 spend) |

10% cashback on selected gym, telco and streaming spend | $20 ($200 spend) |

0.3% cashback on all Other Spend | $30 ($10,000 spend) |

Total | $80 ($10,500 spend) |

Source: UOB EVOL Credit Card terms and conditions

There is a catch to this. You do not want to charge $10,500 on your UOB EVOL just to earn a paltry $80 cashback. That means you’re only earning 0.76% cashback!

Instead, charge only $800 to your UOB EVOL, maxing out the 10% cashback categories. You’re not going to max out the full $80 cashback cap, but the $50 you’ll earn works out to an overall cashback rate of 6.25% on your $800 spend.

Beyond that, use a no minimum spend, unlimited cashback card like the Citi Cash Back+ Card.

Citi Cash Back+ Card / OCBC INFINITY Cashback Card

- Cash Back on Eligible Spend

- 1.6%

- Min. Spend per month

- S$0

- Cash Back Cap

- Unlimited

Get S$400 Cash Reward or 6,140 SmartPoints (worth up to S$499 of Gifts) —just spend S$500 within 30 days of card approval with your new Citibank Credit Card! Receive them as quickly as 5 weeks after meeting the spend criteria.

PLUS, double your excitement with a chance to win the ultimate S$15,000 getaway to your dream destination in our exclusive lucky draw! T&Cs apply.

- on eligible transactions

- Earn 1.6% Cashback

- Min. Spend

- S$0

- Cashback Cap

- Unlimited

Get $250 Cash or 3,900 SmartPoints (enough to redeem an Apple AirPods Pro 3 worth S$349) when you apply and spend a min. of S$400 within 30 days! T&Cs apply.

Unlimited cashback cards with no minimum spend are the least stressful cashback cards out there. No calculation tables like the one I did up above, no minimum or maximum spends to stress out over. Just charge your spending to the Citi Cash Back+ Card or OCBC INFINITY Cashback Card and earn 1.6% cashback on it.

Both cards have the same earn rates with no minimum or maximum spends, and they’re also both Mastercard. One difference I would like to point out is that with the Citi Cash Back +, your cashback will be credited into your account and can be redeemed via the Citibank app whenever you like, in increments of $10. With the OCBC INFINITY, the cashback you earn will be automatically credited into your card account the following month.

While 1.6% cashback isn’t a lot, it’s a good option if (a) you’re making a large purchase that will grossly overshoot the bonus caps on your other cards, or (b) you won’t hit the minimum spends on higher cashback credit cards.

BONUS: Instead of the Citi Cash Back+ Card or OCBC INFINITY, you could also consider another unlimited cashback card—the CIMB World Mastercard. The catch? While this card covers a broad range of categories—Wine & Dine, Online Food Delivery, Movies & Digital Entertainment, Taxi & Automobile, Luxury Goods—the Citi Cash Back+ Card covers more. Also, it has a minimum monthly spend of $1,000.

Why they're a great combination

After you make use of the higher 10% cashback on the UOB EVOL credit card, spending more on it will only earn you a meagre 0.3% cashback. So past $800 spending, use the fuss-free, $0 minimum spend, unlimited Citi Cash Back+ Card to earn 1.6% on your other spending for the month.

3. Best credit card pairings for miles

Miles credit card | Bonus rebate | Minimum monthly spend | Monthly cap on bonus category |

UOB PRVI Miles Card (Mastercard / VISA / Amex) | – 8 miles per $1 spend (UNI$20 per S$5 spend) on major airlines and hotels booked through Expedia and Agoda | $0 | No cap |

– 10 Citi Miles per S$1 spent on Kaligo | $0 | No cap |

UOB PRVI Miles Card

- on agoda and Expedia bookings via UOB PRVI Miles website.

- S$1 = Up to 8 miles

- on Overseas Spend

- S$1 = Up to 3 miles

- on Local Spend

- S$1 = 1.4 miles

The UOB PRVI Card is a powerhouse in the miles card game. It gives you a generous 8 miles per $1 (mpd) on airlines and hotels you book through Expedia and Agoda, which, to my knowledge, is currently the highest in the market for air tickets. On top of that, its local and foreign spend earn rates are collectively also the highest base rates around, at 1.4 mpd and 2.4 mpd respectively.

You earn miles in the form of UNI$, UOB’s rewards points currency. Note that you earn per every $5 spent, and UNI$ expire 2 years from the last day of each periodic quarter in which the UNI$ was earned.

Citi PremierMiles Card

- Local Spend

- S$1 = 1.2 miles

- All Foreign Currency Spend including Retail and Online

- S$1 = Up to 2.2 miles

- Selected Online Hotel and Flight bookings

- S$1 = Up to 10 miles

Get S$400 Cash Reward or 6,140 SmartPoints (worth up to S$499 of Gifts) —just spend S$500 within 30 days of card approval with your new Citibank Credit Card! Receive them as quickly as 5 weeks after meeting the spend criteria.

PLUS, double your excitement with a chance to win the ultimate S$15,000 getaway to your dream destination in our exclusive lucky draw! T&Cs apply.

The highest miles earn rate for hotel bookings belongs to the Citi PremierMiles Card, coming in at 10 Citi Miles per S$1 spent on Kaligo. You can also get 7.2 Citi Miles per S$1 spent on hotel bookings worldwide on Agoda. While its regular local and foreign spend miles earn rates are average at best, there’s the added benefit of the fact that Citi Miles never expire. If you don’t travel often, don’t sweat it. Take your time to accumulate your Citi Miles.

Why they're a great combination

If you’re looking at miles cards, I think it’s safe to assume you have travel on your mind. That means 2 major expenditures: air tickets and hotels. For your plane tickets, use the UOB PRVI Miles Card to earn 8 mpd on airlines when you book through Expedia or Agoda. Then for your accommodation, whip out your Citi PremierMiles Card for 10 Citi Miles per S$1 spent on Kaligo or 7.2 Citi Miles per S$1 spent on Agoda. For all other general expenses, use the UOB PRVI Miles Card for 1.4 mpd earnings on local spend and 2.4 mpd earnings on foreign spend.

4. Best credit card pairings for rewards points

Rewards credit card | Bonus rebate | Minimum monthly spend | Monthly cap on bonus category |

– 10X Points for online purchases (online grocery, food delivery, ride-hailing and more) | $0 | $1,000 | |

– Up to 25X UNI$ per $5 spent on your preferred rewards category | $0 | $1,000 |

Citi Rewards Card

- on Online Grocery, Food Delivery, Ride-Hailing

- S$1= 10X Points

- for in-store shopping purchases at Department Store, Clothing Stores

- S$1= 10X Points

- for all other purchases

- S$1= 1X Point

Get S$400 Cash Reward or 6,140 SmartPoints (worth up to S$499 of Gifts) —just spend S$500 within 30 days of card approval with your new Citibank Credit Card! Receive them as quickly as 5 weeks after meeting the spend criteria.

PLUS, double your excitement with a chance to win the ultimate S$15,000 getaway to your dream destination in our exclusive lucky draw! T&Cs apply.

The chief strength of the Citi Rewards Card is the large range of categories you can earn bonus points on. Earn 10 Citi ThankYou Points per $1 spent on:

- Online purchases, including online spending on groceries, food delivery, ride-hailing and more. Excludes mobile wallet and travel-related transactions.

- Shopping purchases, referring to department stores, clothing stores, shoe shops, and more.

All other purchases earn 1X Point, which is the base rate.

The 10X Points rebate is actually split into 1X Base Point and 9X Bonus Points. While Base Points have no cap, Bonus Points are capped at 9,000 a month, which you’ll hit with $1,000 spend.

Rewards points expire after 5 years. They can be redeemed as cash rebates, used to offset your purchases with Citi Pay with Points, or you can even choose to redeem them for merchandise or shopping vouchers. The conversion rate is 440 Points = S$1 cash rebate. If you do the math, that’s a cashback rate of 2.27%. It’s not a very high rate, but it’s a high spend cap and a large number of categories.

- You spend $100 and earn 1,000 Points

- You redeem 1,000 Points for $2.27

Alternatively, redeem your points for miles at a rate of 10X Points = 4 Citi Miles, where 1 Citi Miles is 1 airline miles/hotel point.

UOB Lady’s Card

- on up to One Rewards Category

- S$5 = Up to 9X UNI$ (equivalent to 3.6 miles per S$1)

- on All Other Spend

- S$5 = 1X UNI$ (or 0.4 miles per S$1)

- Rewards to Miles Conversion, no min. spend

- 1 UNI$ = 2 Miles

The credit card that offers the most flexibility all-round is the UOB Lady's Card, which offers up to 25X UNI$ per S$5 spent (equivalent to 10 miles per S$1) on a preferred category of your choice: Beauty & Wellness, Dining, Entertainment, Family, Fashion, Transport and Travel. If/when you change your mind, you have the flexibility to change your preferred category every quarter. The UOB Lady’s Card also lets you earn bonus rates online, in-stores, locally and overseas, so you can cast your net wide and she will deliver.

The catch is that the generous 25X UNI$ per S$5 spent (10 miles per S$1) carrot that UOB is dangling only applies if you also save with the UOB Lady's Savings Account and deposit at least $100,000. Here’s how the bonus UNI$ stack to add up to 25X UNI$:

UOB Lady’s Card earn category | UNI$ earn rate | Monthly cap |

Base earn rate | 10X UNI$ for every S$5 spent (equivalent to 4 miles per S$1) | No cap |

Bonus with UOB Lady’s Savings Account | Up to 15X UNI$ (equivalent to 6 miles per S$1) | $1,000 |

TOTAL | – 10X UNI$ per $5 spending on your preferred category | – |

On the bright side, there’s no minimum spend required and the monthly rebate cap on Bonus UNI$ is quite high at $1,000 spend per calendar month.

You can choose to redeem UNI$ for over 1,000 rewards across dining, shopping and travel, and have 2 years to do so before they expire. So the UOB Lady’s Card is flexible from earning UNI$ to redeeming them.

Why they're a great combination

Between the Citi Rewards Card and the UOB Lady’s Card, you can earn bonus rebates on up to $2,000 worth of spending each month. Both breach a large number of categories in different ways—the Citi Rewards Card lets you earn bonus points on a large number of online spend categories, while the UOB Lady’s Card gives you the flexibility to choose the category you want to earn bonus UNI$ in each quarter.

Between the 2, assuming you use the UOB Lady’s Card without the UOB Lady’s Savings Account, both have slightly different earn rates but similar redemption conversion rates.

ThankYou Points (Citi Rewards Card) | UNI$ (UOB Lady’s Card) | |

Earn rate | S$1 spend = 10X ThankYou Points | S$5 spend = 10X UNI$ |

Miles conversion rate | 10X ThankYou Points = 4 Miles | 10X UNI$ = 4 Miles |

Cash rebate conversion rate | 4,400 Points = S$10 cash rebate | UNI$1,136 = S$10 cash rebate (under the Auto Conversion Programme) |

If you’re redeeming your points for miles, use either card. But if you’re redeeming them for cash rebates, you’re better off reaching for the UOB Lady’s Card—provided the purchase you’re making falls under the preferred category you chose that quarter. And if you’re gunning for a merchandise or voucher reward, check the UNI$ rewards catalogue and Citi ThankYou Points reward catalogue first. Either way, you should have a good range of options between these 2 cards.

Found this article interesting? Share it with your family and friends!