If you’ve ever spoken to a financial advisor in Singapore, you’ve probably heard the term MDRT—often mentioned as a mark of achievement, yet rarely explained in plain English. MDRT, short for Million Dollar Round Table, certainly sounds prestigious. But what does it actually mean for you as a client? And should it influence how much you trust an advisor?

To get clarity, we spoke to Edwin Ooi, MoneySmart Financial’s Senior Financial Advisory Manager and a 3-time MDRT qualifier (2024, 2025, 2026). With his help and expertise, we break down what MDRT really represents—and what your advisor’s MDRT badge does (and doesn’t) say about the quality of advice you receive.

[ms-toc title="MDRT explained: What is MDRT and why should you care?"]

1. What MDRT is

MDRT stands for Million Dollar Round Table—a global, independent association that recognises top-performing financial advisors. In practice, an advisor qualifies for MDRT by meeting specific annual production benchmarks, typically measured through commission, premium, or income. In other words, MDRT is a performance-based industry recognition, awarded yearly to advisors who hit a clearly defined sales threshold.

A useful way to think about MDRT is like the Michelin Guide—an industry-led recognition, not a government regulator. It’s prestigious and widely respected within the industry. However, there’s one important difference: Michelin is based on the customer experience, while MDRT is largely based on sales performance.

2. What MDRT is not

MDRT does not mean your advisor is a millionaire. As Edwin puts it, “many people think that the ‘Million Dollar’ part in ‘MDRT’ refers to the advisors”—but this is untrue.

It’s also not a regulatory certification. Edwin notes that some people “misunderstand that MDRT is a stamp of approval from a regulatory sense.” It isn’t issued or endorsed by MAS, so it shouldn’t be treated as an official trust badge—or a guarantee of advice quality.

3. What does an advisor need to do to get into MDRT?

To qualify for MDRT, an advisor has to meet a minimum sales target for the year—based on how much commission, premium, or income they earn.

- Commission: The fee an advisor earns when you buy a financial product through them.

- Premium: The amount you pay for an insurance policy (usually monthly or yearly).

- Income: The advisor’s total earnings from their work over the year (including commissions and other qualifying revenue).

To get into MDRT, advisors only need to qualify through one of these routes.

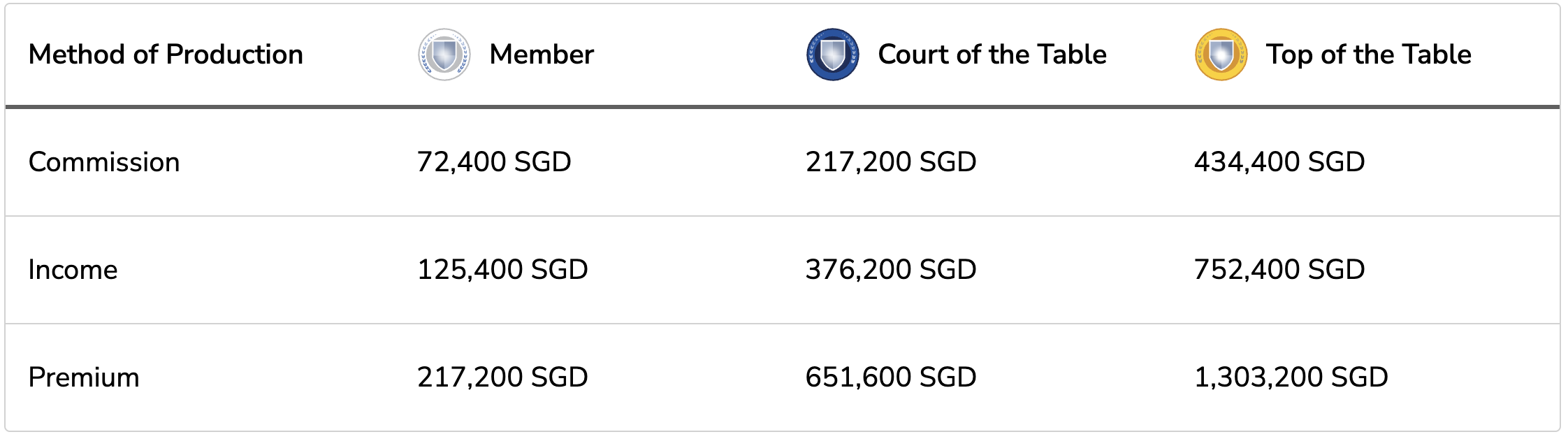

MDRT also has 3 achievement levels: MDRT, Court of the Table, and Top of the Table, each requiring progressively higher performance.

For 2025, the official qualification criteria are shown below:

Image: MDRT

As Edwin explains, “these are the criteria that are set within the professional body, and if you meet these criteria, then you'll be attributed a certain ‘badge’ or ‘label’. It’s very black and white.” I think of it like going up ranks in a game—it’s fully transparent what numbers you need to hit to earn the next title.

Importantly, note that qualification resets every year, so advisors need to consistently hit these benchmarks to remain MDRT members.

4. Does MDRT say anything about the quality of advice?

As Edwin explained, a common misconception is treating MDRT like “some kind of absolute quality label”. In truth, MDRT is a recognition of production, not a guarantee of advisory skill. It shows that an advisor has achieved a high level of annual sales, but it doesn’t measure how well they listen, plan, or recommend suitable products.

MDRT does require members to follow a professional code of ethics, but it doesn’t assess client outcomes, financial planning rigour, or long-term service quality. As Edwin stressed, MDRT “doesn't mean the advisor is rich or infallible, it means they have hit a high sales mark and pledged to operate under a professional code.” It’s a “strong indicator of sales success, but not a direct score card of advice quality.”

In other words, MDRT can tell you that an advisor is high-performing in sales and has followed the set professional code, but it cannot guarantee you whether they are the right advisor for your needs, your risk profile, or your financial goals.

5. Can MDRT targets influence the kind of products an advisor recommends?

Edwin notes that “because MDRT is a sales performance benchmark, it is inevitable that it can influence how some advisors prioritise products.” In other words, the drive to meet specific production thresholds can push some advisors to prioritise higher-premium or higher-commission products in order to qualify.

However, Edwin also stressed that this is where professionalism matters: “It comes down to how we marry that sales performance driving and the code of ethics within.” In other words, a responsible advisor should not let MDRT goals override suitability.

6. What questions should you ask an MDRT advisor before buying anything?

Whether your advisor is MDRT or not, the questions you ask matter far more than the title they hold. MDRT tells you an advisor has hit strong sales targets, but it doesn’t reveal how well they understand your needs or whether their recommendations suit your situation. Before committing to any product, make sure you probe deeper with clear, structured questions.

Here are the essentials to ask of any advisor:

- How do you get paid?

Understand whether commissions or bonuses might influence recommendations. - Why are you recommending this product for me specifically?

Push the advisor to link the suggestion to your goals, budget and life stage. - What alternatives did you consider, and why not those?

A good advisor should show they’ve compared options. - What are the risks or downsides I should be aware of?

This reveals the transparency and robustness of advice. - How will you support me after the policy is sold?

Helps you gauge long-term service—not just the initial sale.

Any good advisor should welcome these questions and answer them clearly and confidently.

7. So… should you care about MDRT at all?

Yes–and no. MDRT can be a useful signal, as it shows an advisor has reached a high level of consistency and professionalism in their sales performance. These are qualities that often correlate with strong client service.

However, MDRT is not a universal badge of quality. Titles alone can’t tell you whether an advisor listens well, recommends suitable products or provides reliable long-term support. As Edwin reminded us, MDRT is not “some kind of absolute quality label.” It’s simply one data point. In some cases, it may even warrant caution if an advisor relies heavily on titles rather than demonstrating understanding, suitability and transparent planning.

Crucially, MDRT “doesn’t directly measure suitability nor the quality of ongoing service.” An advisor’s true value still comes through conversation, clarity, and trust—traits you should look for, whether they are MDRT or not.

If you’d like help understanding what MDRT means in the context of your financial decisions, you can speak with Edwin or any of MoneySmart Financial’s licensed Financial Advisory Specialists. They can walk you through your options, clarify how different products work and help you make informed, confident choices.

Found this article useful? Share it with anyone who might come across the term "MDRT".

For more guides and the latest promotions, visit MoneySmart, Singapore’s best and trusted personal finance platform.

This article was first drafted with the help of AI and later reviewed and refined by the author.

Related Articles