Tiq Pet Insurance positions itself as an affordable, flexible plan with some surprisingly strong perks—especially for young pets. Premiums start from $355.20 for dogs and $296.00 for cats, placing it in the mid-range of Singapore’s pet insurance market.

One standout feature? You can enrol your pet from just 8 weeks old—a minimum age matched only by Liberty PetCare. Add in a generous no-claim discount of up to 20%, complimentary hereditary coverage, and solid accident benefits across all tiers, and Tiq quickly becomes an interesting contender.

But while it offers strong flexibility and meaningful perks, coverage limits are generally more modest than top-tier plans like Income or MSIG. Let’s break it down.

[ms-toc title="Shopee pet insurance—MoneySmart review (2026)"]

1. How much does Tiq Pet Insurance cost?

- Premium: Starting from $355.20 (dogs) / $296.00 (cats)

- Eligible age: 8 weeks to below 9 years

Annual premiums:

Tiq pet insurance annual premiums | ||||

Pet/plan tier | Pawsome | Pawmazing | Pawtastic | Pawfect |

Dog | $355.20 | $568.30 | $668.38 | $782.01 |

Cat | $296.00 | $473.59 | $556.98 | $651.67 |

Compared to other insurers in Singapore, Tiq pet insurance’s pricing is in the middle tier. It sits below Income Happy Tails pet insurance and MSIG PawEasy pet insurance at the higher tiers, but above Shopee’s budget pricing. The key question isn’t just price—it’s how far those benefit limits stretch.

Looking to get your fur kid protected? Check out our other pet insurance reviews and guides.

|

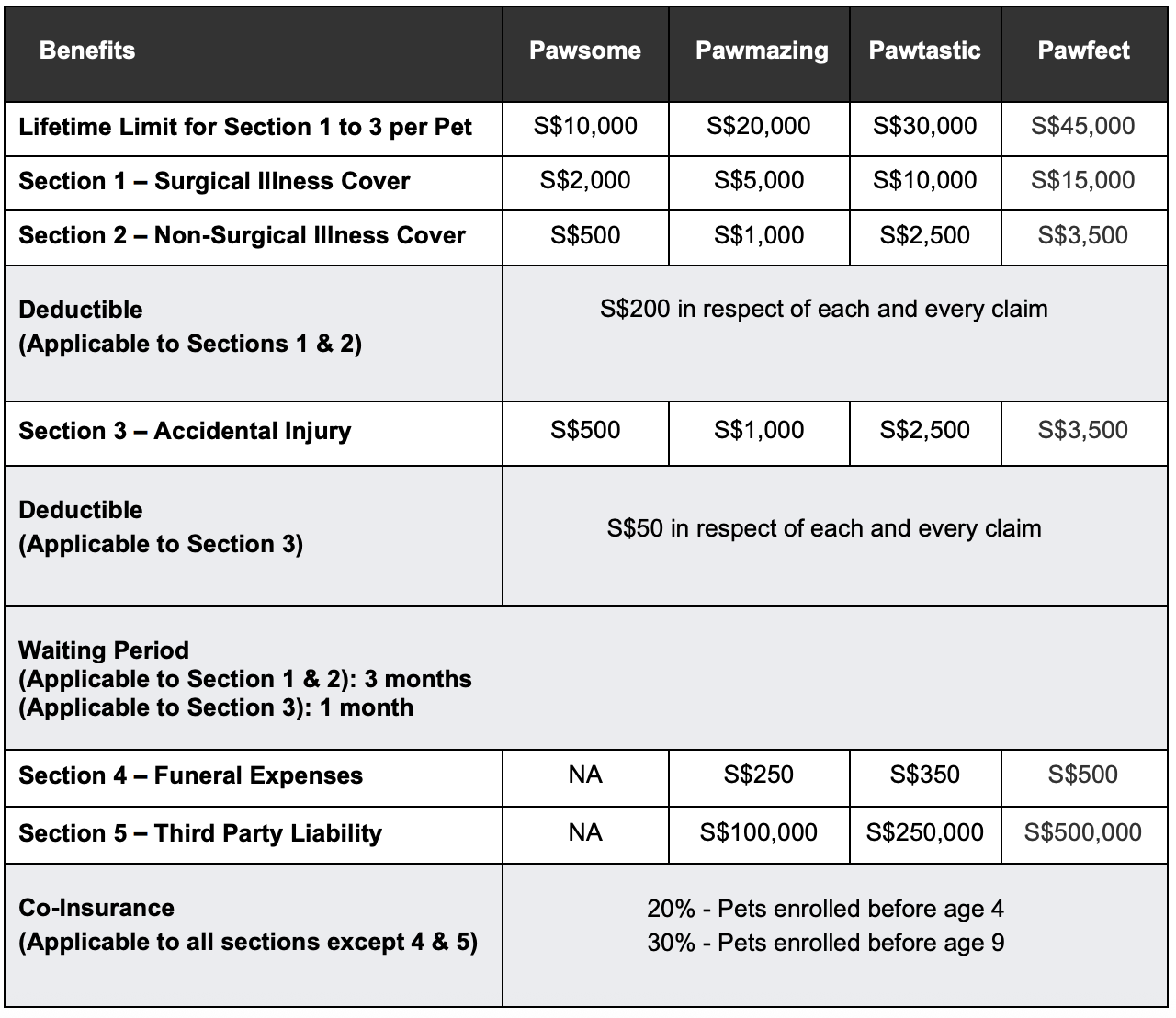

2. What does Tiq Pet Insurance cover?

Image: Tiq

Tiq divides medical expenses into 3 main categories:

- Surgical illness

- Non-surgical illness

- Accidental injury

Across these 3 categories, there’s a combined lifetime limit of up to $45,000 per pet (Pawfect plan).

That lifetime structure is different from annual-reset models like Income’s. It works well for owners seeking long-term protection, but you’ll want to be mindful that major early claims reduce the remaining lifetime pool.

Surgical illness cover

- $2,000 to $15,000 (depending on tier)

These limits are adequate but not market-leading. For comparison, Income’s top surgical benefit reaches $22,000 per year, and MSIG’s hospitalisation and surgery goes up to $20,000 annually.

Tiq’s coverage is solid for moderate procedures but may feel tighter for complex surgeries.

Non-surgical illness cover

- $500 to $3,500

This covers treatments that don’t require surgery—such as medication, diagnostics, and ongoing care.

Limits are modest compared to some competitors, but inclusion across all tiers is helpful.

Accidental injury cover

- $500 to $3,500

Here’s where Tiq shines. Accident cover is available at every tier, unlike Income, which restricts accident coverage to its top plan and caps it at $2,500.

Even better: the deductible for accident claims is just $50, significantly lower than Income’s $250.

For active dogs or adventurous cats, this is a meaningful advantage.

Funeral expenses and liability cover

Tiq does not provide:

- Death benefit

- Theft benefit

However, it includes:

- Funeral expenses: $250 to $500 (not available on lowest tier)

This is competitive within the market—though Income’s $750 to $2,500 final expense benefit remains more generous.

Third party liability is also only available from the second tier (Pawmazing) onwards, with limits from $100,000 to $500,000.

For most pet owners, Pawmazing or higher offers more balanced protection.

3. What will you actually pay when claiming from Tiq pet insurance?

As far as deductibles and co-insurance go, Tiq applies:

- $200 deductible per claim (for surgical and non-surgical illness)

- $50 deductible per accident claim

On top of that, co-insurance applies:

- 20% if enrolled before age 4

- 30% if enrolled before age 9

For example, if your pet undergoes surgery costing $5,000 under the Pawmazing plan:

- You pay the first $200 (deductible)

- Then 20% or 30% of the remaining $4,800

That means your out-of-pocket cost could range from $1,160 to $1,640, depending on enrolment age.

So while premiums are moderate, you’ll still share a meaningful portion of large medical bills.

4. Tiq Pet Insurance—complimentary hereditary and congenital coverage

One of Tiq’s biggest differentiators is that it includes coverage for certain hereditary and congenital conditions, subject to:

- A 12-month waiting period

- A required clinical examination

- No pre-existing diagnosis

Covered conditions include:

- Hip and elbow dysplasia

- Luxating patella

- Glaucoma

- Cherry eye

- Intervertebral disc disease (IVDD)

- Femoral head and neck excision

Not all insurers include these conditions automatically, so this is a genuine value-add—especially for pedigree breeds prone to joint or eye conditions.

ALSO READ: How Does Pet Insurance Work in Singapore? 10 Frequently Asked Questions

5. No-claim and multi-pet discounts for Tiq Pet Insurance

Tiq offers one of the most generous no-claim discount structures in Singapore:

Renewal year | No-claim discount |

First | 5% |

Second | 10% |

Third and fourth | 15% |

Fifth and beyond | 20% |

Most pet insurance providers cap their no-claim discounts at 15%, so Tiq’s structure rewards long-term, low-claim pet owners more meaningfully over time.

This can make a real difference to affordability. For example, if you’re paying $568.30 for a mid-tier dog plan, a 20% discount eventually brings that down by over $110 per year. Over several years, that adds up.

For multi-pet households, Tiq also offers:

- 5% off for 2 pets

- 10% off for 3 pets

Unlike some insurers that require separate applications with no bundling benefit, Tiq actively rewards multi-pet families—making it particularly appealing for owners with both dogs and cats.

6. Eligibility for Tiq Pet Insurance: Which pets can apply?

To apply for Tiq Pet Insurance, the following requirements must be met:

- Your pet must be residing with you in Singapore

- You must be a Singapore Citizen, Permanent Resident, or a foreigner holding a valid Work Permit, Employment Pass, Dependant’s Pass, or Long-Term Visit Pass

- Your pet must be microchipped and have completed required vaccinations

- Your pet must be at least 8 weeks old and below 9 years old at policy start

- Your pet must not be a working pet (e.g. guide dog, hunting dog, attack dog) or racing pet

- Your pet must not be used for breeding

Importantly, Tiq does not require a medical examination for its base insurance coverage. A clinical exam is only required if you opt in to the complimentary congenital and hereditary cover.

This makes the base plan relatively straightforward to apply for, while still maintaining medical underwriting safeguards for higher-risk hereditary benefits.

7. Pros and cons of Tiq Pet Insurance

Tiq strikes a thoughtful balance between affordability and meaningful protection—but it’s not built as a high-limit, premium-tier medical shield. Here’s how the trade-offs play out.

Pros

- Early enrolment from 8 weeks

- Strong accident coverage across all tiers

- Low $50 accident deductible

- Complimentary hereditary coverage (with rider conditions)

- No-claim discount up to 20%

- Multi-pet discounts available

Tiq’s biggest strength is its practicality. Accident coverage is available across all tiers—not locked behind a premium plan—and the $50 deductible makes smaller accident claims less painful. The hereditary coverage inclusion (subject to conditions) is also a genuine differentiator in a market where many insurers exclude these entirely.

Cons

- Modest surgical and non-surgical limits

- No death or theft benefit

- Funeral and liability unavailable on lowest tier

- Co-insurance up to 30%

- Lifetime limit structure may reduce long-term flexibility

Because Tiq operates with a lifetime limit rather than annual resets, large early claims could meaningfully reduce the pool available later in your pet’s life. Owners seeking high annual medical ceilings may find Income or MSIG more suitable.

8. Who should buy Tiq Pet Insurance?

Tiq is particularly attractive for:

- New puppy or kitten owners (from 8 weeks old)

- Multi-pet households looking for discounts

- Owners concerned about hereditary conditions

- Those who prioritise accident protection

- Budget-conscious owners who still want structured coverage

If your pet is young and healthy, enrolling early allows you to lock in lower co-insurance rates and maximise the benefit of the hereditary cover waiting period. Over time, the no-claim discount can also meaningfully improve affordability.

However, if your priority is the highest possible annual surgical limits or very large third party liability coverage, you may want to compare higher-tier alternatives.

9. Final verdict: Is Tiq Pet Insurance good value?

Tiq offers a compelling middle-ground option in Singapore’s pet insurance market. It may not boast the highest medical limits, but it compensates with early enrolment eligibility, strong accident coverage across all tiers, generous no-claim rewards, and complimentary hereditary protection.

For owners who want structured, sensible coverage without paying top-tier premiums, Tiq delivers solid value—especially if you start early and maintain a claim-free record.

MoneySmart verdict: Tiq provides affordable, flexible protection with standout perks for young pets and multi-pet households, though its modest medical limits and co-insurance mean it’s best for owners comfortable sharing part of major vet bills. |

For more information, view Tiq pet insurance policy wording.

This article was first drafted with the help of AI and later reviewed and refined by the author.

Found this article useful? Share it with your fellow pawrents!

Related Articles