When we first wrote about the DBS NAV Planner update in July, it was already a powerful personal finance tool that could help us take stock of our finances, keep tabs on our investments and much more.

When we first wrote about the DBS NAV Planner update in July, it was already a powerful personal finance tool that could help us take stock of our finances, keep tabs on our investments and much more.

There’s recently been another upgrade to DBS NAV Planner — this time in the form of nifty new feature Map Your Money.

Built directly into your DBS digibank, this easy-to-use tool conveniently provides insight into your cashflow projection as far as 50 years ahead, to help you plan for your financial goals, especially ahead of major financial decisions (buying a big-ticket item, looking to invest a 5-figure sum, or even budgeting for home renovations) or life changes.

By being able to visualise your long-term cashflow, you can stay on track to meet whatever financial goals you may have — long-, mid- or short-term — without needing to “guesstimate” things like how much your current funds will last should *touch wood* anything happen, or help those closer to retirement age take stock of all of your assets across multiple financial institutions so they can distribute these assets smoothly.

The cashflow projection helps you plan for major decisions like buying a house or paying for your dream wedding. Input how much you intend to spend and you get a clear idea of how this major decision impacts your cashflow and future goals.

Here are 5 new financial insights DBS NAV Planner’s new feature Map Your Money provides:

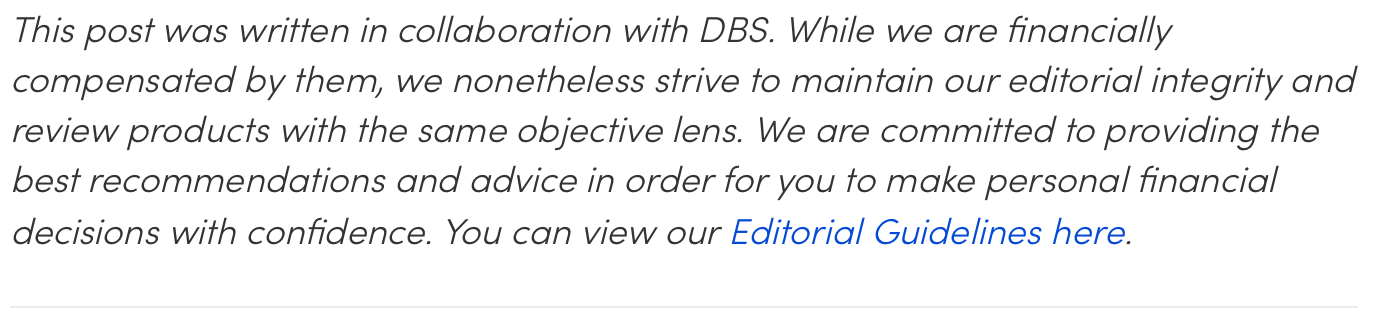

1. Project your cashflow for years ahead

First off, Map Your Money is extremely simple to set up, especially if you’re an existing DBS digibank user and have been actively using DBS NAV Planner.

First off, Map Your Money is extremely simple to set up, especially if you’re an existing DBS digibank user and have been actively using DBS NAV Planner.

Cashflow refers to the net amount of cash and cash-equivalents (aka your assets) that are being transferred in and out of your account. Also known as the sum of your money-in-money-out (MIMO), it can be positive, negative, or at the breakeven point.

Of course, it’s always best to have positive cashflow. This means that what you have grows over time, and you can achieve your financial goals. If it’s negative... Uh oh, you may either need to relook your current lifestyle and cut back on certain things, or worse, borrow money so that you can pay your bills.

What’s good about Map Your Money is that it gives you a good at-a-glance view of your investments, cash and even CPF. Even assets such as those held under the Supplementary Retirement Scheme (SRS) scheme are also accounted for.

By integrating baseline CPF and SRS rules, DBS customers will have greater clarity around your financial future. This stamp of approval from the CPF Board gives Map Your Money the advantage of comprehensiveness and rigour to best serve DBS digibank customers’ needs.

Now that you’ve projected your MIMO and total assets, you’ll get a better idea of any gaps you’ll need to fill. What’s nice about NAV Planner being on DBS digibank is that it’s a full-service solution — for every financial gap, there’s a whole suite of solutions, from investment and insurance, that everyone can access to boost their portfolios.

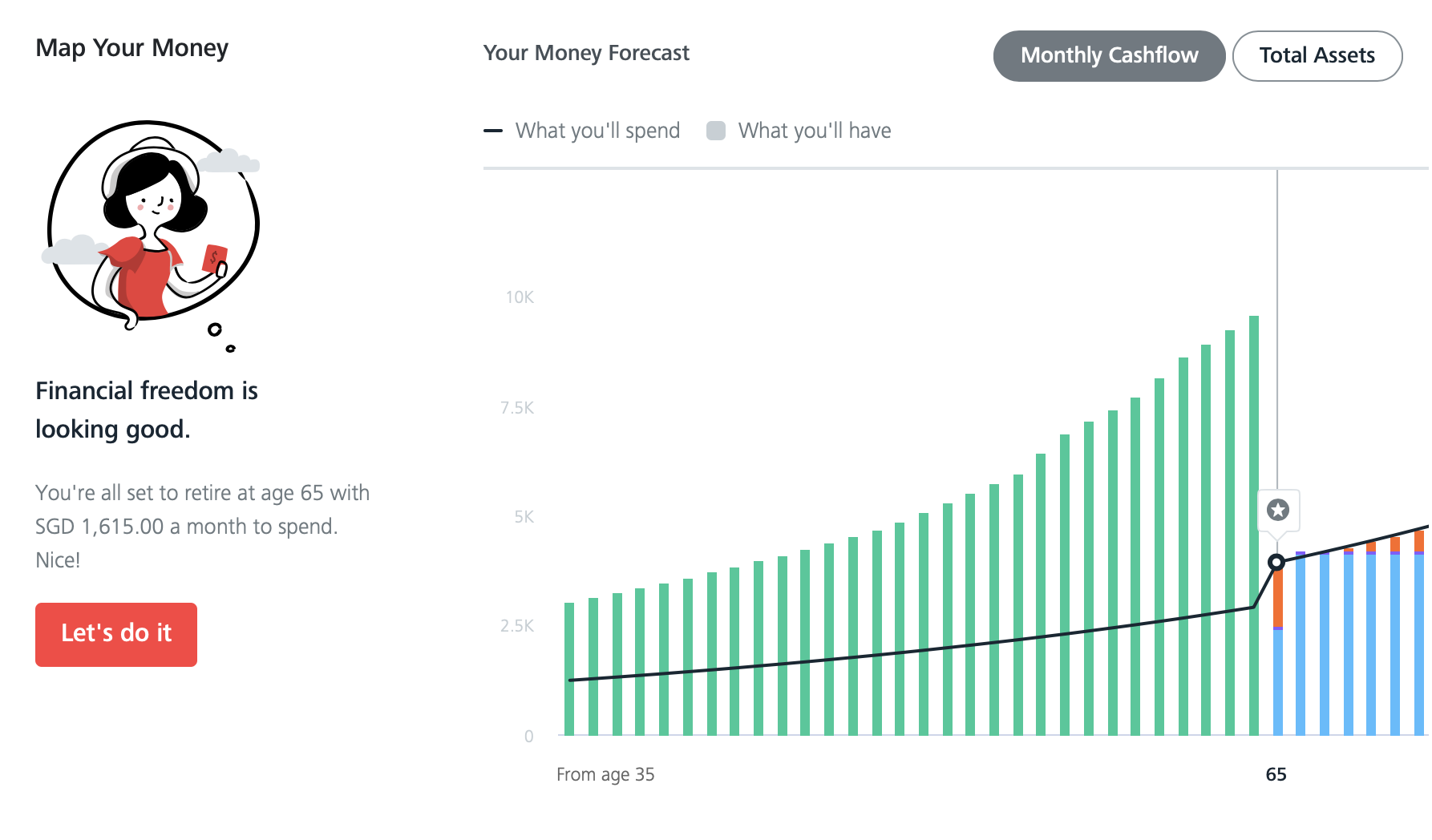

2. Be prepared for milestones

With Map Your Money, you can now set money goals. Planning to get married in a few years? Set a goal. Want to put your (future) kid through university? Set a goal. Want to splash out on a much-deserved vacation once Covid-19 blows over? Set a goal!

With Map Your Money, you can now set money goals. Planning to get married in a few years? Set a goal. Want to put your (future) kid through university? Set a goal. Want to splash out on a much-deserved vacation once Covid-19 blows over? Set a goal!

Setting black-and-white goals can really help you plan ahead, alert you on your progress and segment key funds from your everyday spending (or splurging) so you will keep to a budget. This helps you avoid a situation where you just procrastinate on your goal and start panicking a month before you need the cash.

Although there’s always a personal loan to turn to, why pay interest if we can avoid it? A clear list of goals also allows you to prioritise them and put them on hold, if cashflow is an issue. When you put a goal on hold in DBS NAV Planner, the cashflow projection removes that particular goal from your simulation so you see how much more wiggle room you have with your finances.

One of the longest-term milestones you can also plan for is retirement. In addition to using Map Your Money projections to manage your financial expectations, DBS’ retirement planning portal has tons of resources to help you along and ensure you don’t miss any blind spots when it comes to retirement.

Learn more about estate planning, access relevant services such as CPF nomination, will writing, and setting up a Lasting Power of Attorney.

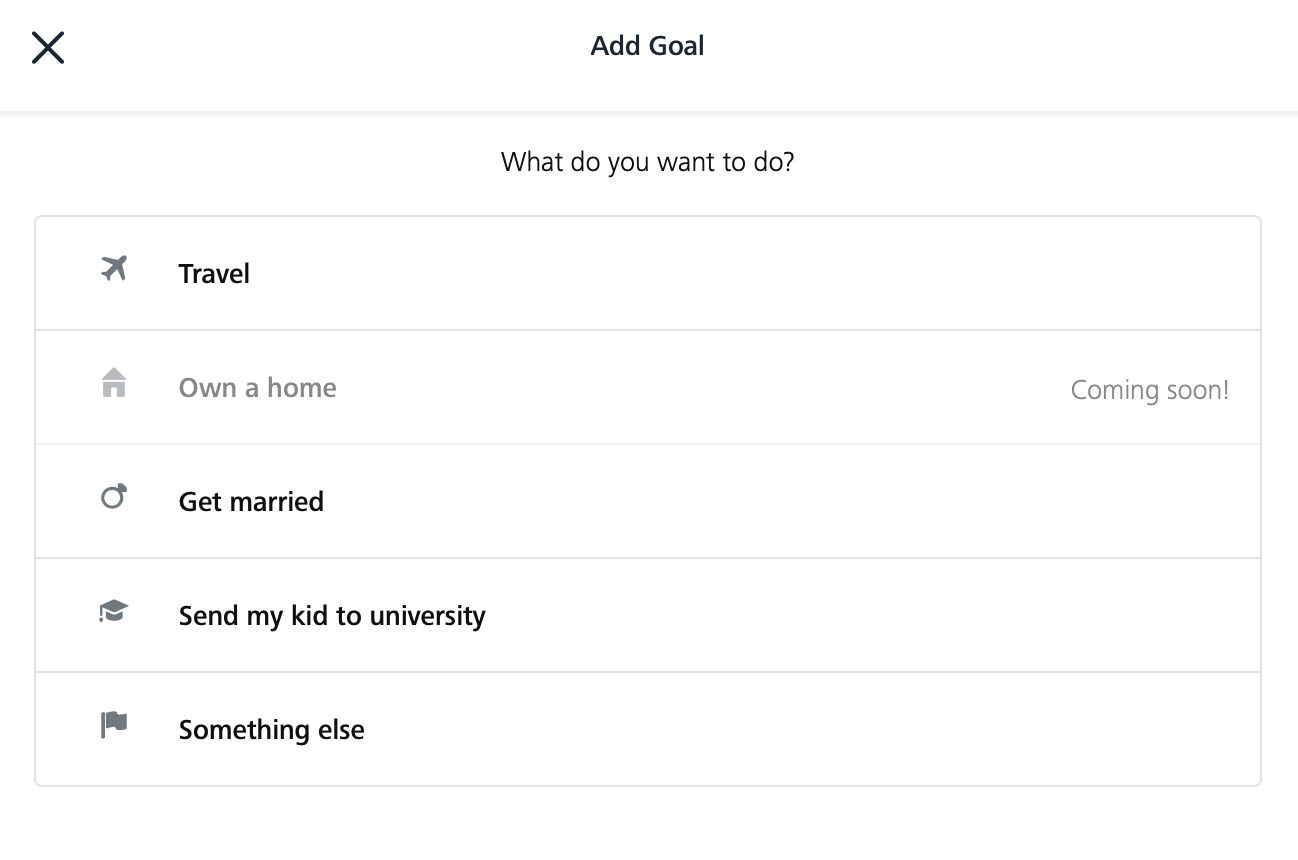

3. Project your investments

Did you know that there’s also an investment simulator? Look for “Make Your Money Work Harder” in NAV Planner - Investments.

Did you know that there’s also an investment simulator? Look for “Make Your Money Work Harder” in NAV Planner - Investments.

DBS has also included a market price feed feature, which allows you to input all your investments into DBS NAV Planner (yes, even those outside DBS) and get updated portfolio values! For example, if you bought 100 units of a stock on the SGX, DBS NAV Planner can automatically display its value for you — no more logging in and out of multiple ecosystems just to get a sense of your net worth!

If you’re considering any new investments but haven’t actually bought them yet, you can even input them and use the market price feed feature to monitor their prices.

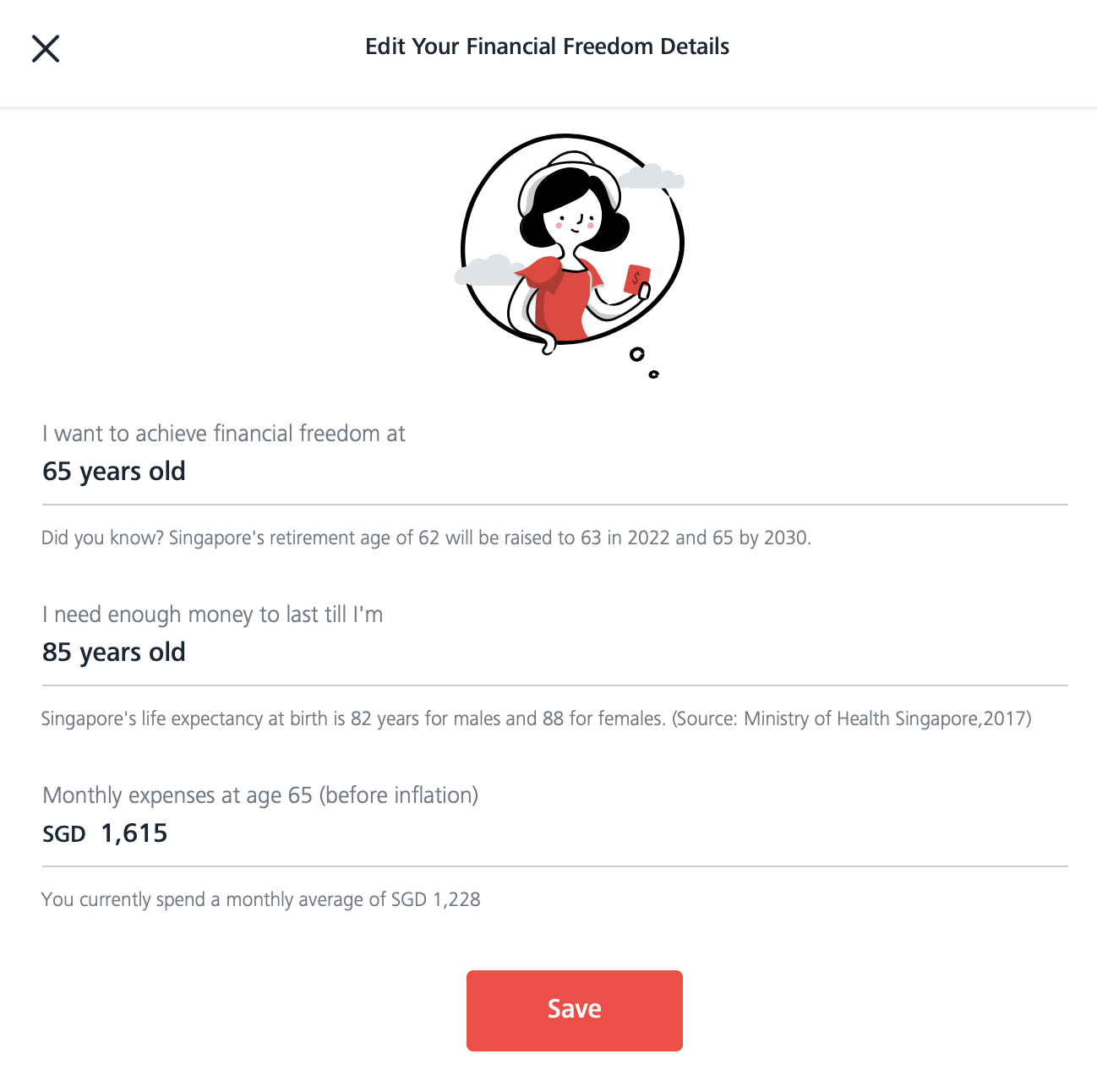

4. See if you’re REALLY ready for retirement

With Map Your Money, you can easily edit your financial freedom details, get an instantly-updated at-a-glance look at your cashflow projection — and also eyeball if the projected amount of money is enough for your golden years.

With Map Your Money, you can easily edit your financial freedom details, get an instantly-updated at-a-glance look at your cashflow projection — and also eyeball if the projected amount of money is enough for your golden years.

Map Your Money also takes into account complex CPF rules — this is a first-of-its-kind collaboration between the CPF Board and a bank — so all of your assets will be accounted for when you visualise your retirement at your preferred retirement age.

No need to go back and forth to check and do messy calculations as it’s all taken care of by Map Your Money. If you’ve been holding a permanent job since you graduated, you should amass a good amount of CPF in your Retirement Account that goes towards your CPF LIFE payouts.

However, if the projection shows that you aren’t on track to hit your desired retirement lifestyle or your preferred retirement age, you’ll at least be mentally prepared and have enough lead time to actively make changes to your finances such as saving more, spending less, and investing more.

Who says you can’t shape your future?

5. Take action as soon as possible

If you’re still thinking Map Your Money is all fun and games, and a one-off projection tool just to satisfy your financial curiosity, think again. You can go from understanding your finances to taking action to improve it, in just a few taps. DBS has digital solutions at your fingertips and they can be accessed through digibank too, where DBS NAV Planner sits.

If you’re still thinking Map Your Money is all fun and games, and a one-off projection tool just to satisfy your financial curiosity, think again. You can go from understanding your finances to taking action to improve it, in just a few taps. DBS has digital solutions at your fingertips and they can be accessed through digibank too, where DBS NAV Planner sits.

For someone who has made the effort to input all of their financial details into DBS NAV Planner, Map Your Money can be as close to reality as possible. It’s also intuitive, easy-to-use and editable any time, as and when your financial situation changes.

Users also get friendly reminders, tips and encouragement to keep you on track, motivated and pushing forward with their money goals. It’s also a fantastic dashboard if you need to make snappy financial decisions and a quick money forecast for the years ahead.

DBS NAV Planner and Map Your Money is like an always-on, 24/7 with you, superhuman financial planner that just keeps getting better with time as DBS is constantly making upgrades that benefit users.

By keeping it updated, you can also take immediate action to plug any gaps — all within your DBS digibank.

In short, with DBS NAV Planner you can:

- Quickly review your money-in-money-out (MIMO) — set informed goals instead of blindly working towards arbitrary number

- Try the Investment Simulator and from there learn more about growing wealth

- Get a holistic view of cashflow today, tomorrow, and possibly 50 years into the future

- Speedily review your assets and liabilities — get up-to-date values of all your investments in one place

Make your financial future a certainty. Login to your DBS digibank to start using DBS NAV Planner now.

Have the digibank app? Simply login and click on the ‘Plan’ tab to access DBS NAV Planner.

Related Articles