You're at an overseas payment terminal, card out, and the screen asks: "Pay in SGD or local currency?"

SGD feels safer. You know the number. You select the option to make your payment. Did you know you just paid 5% more than you needed to? Your receipt won't tell you that.

Here’s the thing about travel spending mistakes in 2026: most of them are invisible. They don't show up as obvious fees or error messages. They're baked into exchange rates, buried in weekend markups, and dressed up as convenience.

Singapore clocked 10.4 million overseas trips last year—and a good chunk of that travel budget quietly leaked out through habits that made sense a decade ago, but not anymore.

[ms-toc title="Myths about overseas spending in 2026"]

Myth 1: "Pay in SGD"—It feels safer, but it's costing you more

When the terminal asks how you'd like to pay, SGD feels like a reasonable choice. You see a familiar number and know exactly what's leaving your account. There's no uncertainty about the conversion.

That assurance is going to cost you extra.

Choosing SGD at an overseas terminal triggers the Dynamic Currency Conversion (DCC). Instead of your bank handling the exchange, the merchant's bank steps in with their own rate. Unfortunately, the rate offered is almost always 3 to 12% more expensive than the interbank rate, with the markup going straight to the merchant or payment provider.

DCC markups average around 5%. On a $1,000 hotel bill, that's $50 gone for the comfort of seeing a familiar currency on the screen.

Always choose local currency.

Myth 2: Zero FX fees = I'm winning

Zero FX fees felt like a revelation when multi-currency wallets first made it mainstream in Singapore. Watching that 3% surcharge disappear was genuinely exciting. The thing is, the market has moved on since. Zero fees is now the floor, not the ceiling.

What’s even better is earning cashback on top of zero fees.

Here's the practical difference. Say you spend $1,000 in Japan:

Option | FX Fee | Cashback | Net outcome |

Old credit card | –$30 to –$32.50 | None | You lose $30+ |

Zero-fee wallet | $0 | None | You break even |

Zero-fee card with cashback using the Mari Credit Card | $0 | +$15 | You're up $15 |

Breaking even is infinitely better than bleeding 3%. In 2026, zero fees alone isn't a win, it's the starting point. The real question is what else are you getting on top of it.

Myth 3: Changing money in Singapore always gets you the best rate

For a long time, this was actually true.

The Arcade at Raffles Place, Mustafa Centre, People's Park Complex — they offered tight rates and zero visible fees. Meanwhile, credit cards charge 3% or more on every foreign transaction. Doing the math was easy. The money changer proved to be a better option.

What changed is that credit cards quietly transformed between 2023 and 2026, while the money changers stayed exactly the same. Cards that once bled you 3% on every overseas swipe now come with zero FX fees, competitive exchange rates, and cashback on top. The Mari Credit Card is a good example of what that looks like today.

Zero FX fees—and it's not going away

From 1 January, all foreign currency transactions are fee-free. Not a sign-up promo, or a limited-period waiver. It's a permanent structural feature of the card.

1.5% cashback on overseas spending

Every foreign currency transaction earns 1.5% cashback, up to S$1,500 in overseas spending per month. No minimum spend required, and cashback is credited automatically back to your account. Valid till 31 Dec 2026, refer to the terms and conditions for more information.

Best-in-class rates across Singapore's top travel corridors

Competitive rates built specifically around where Singaporeans actually go: Malaysia, Thailand, Indonesia, Japan, South Korea, Australia, and China. Valid till 31 Dec 2026, refer to the terms and conditions for more information.

See the live rate before you spend (and no annual fee)

Pull up the MariBank app before your trip and check the exact rate in real time—no surprises at checkout. The card also has no annual fees, so there's nothing to offset before you benefit. Here's how it stacks up against the other zero-fee options most Singaporeans are already using:

Card | FX Fee | Overseas Cashback | Annual Fee |

YouTrip | Zero | None | |

Trust Cashback Card | Zero | None | |

Mari Credit Card | Zero | None |

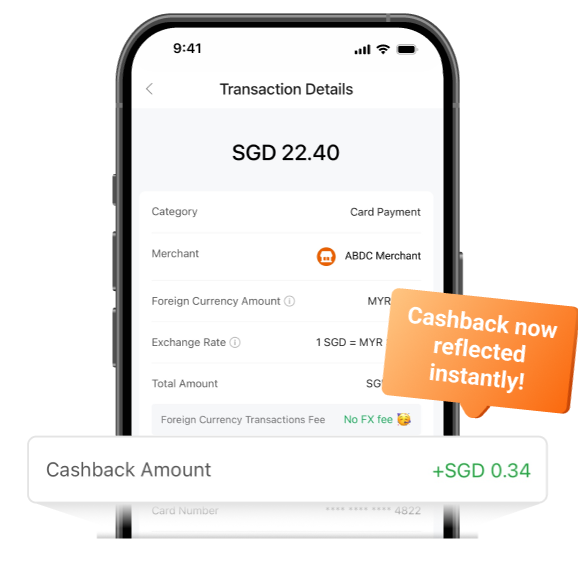

You can even see the estimated cashback received upon a successful transaction:

Image: MariBank

While cash still has its place—visa fees, night markets, and the occasional hawkers that haven't gone contactless yet, the assumption that money changers are always the cheapest is worth revisiting for the bulk of your spending.

Myth 4: Pre-loading currency before you travel is smart planning

The logic behind pre-loading makes sense on the surface: lock in a rate before your trip, spend from a fixed pool, and avoid surprises. It feels like the organised thing to do.

The problem is that you're making a financial decision before you know how much you will spend. Withdraw too much and you're back home with leftover foreign money just sitting there; too little and you're hunting for a top-up in the middle of your trip.

Even if you nail the amount, pre-loading still has a blind spot most people don't think about: wallets don't give you any cashback. Every Baht, Ringgit, and Yen spent earns nothing back. You've avoided the FX fee, but you've given up the upside entirely. A zero-FX-fee credit card offers no loading or guessing, just spend and collect cashback on everything automatically.

Myth 5: It doesn't matter when I top up my travel wallet

Most people treat topping up a travel wallet like topping up an EZ-Link card — something you do whenever it's running low, without much thought about timing.

What's easy to miss is that some wallet apps charge a small markup on weekend currency exchanges, because major FX markets are closed on Saturdays and Sundays. The rate displayed looks the same as any other day — but you could be paying 1% more on the conversion without realising it.

The markup is quietly folded into the exchange rate you see, which is why it's so easy to miss. That 1% adds up faster than it sounds:

- $500 JB top-up on Saturday afternoon = $5 in weekend markup, gone

- Repeat once a month = $60 a year, purely from bad timing

- $1,500 Bangkok trip top-up on Sunday = $15, just for the day

If your travel card is a credit card with zero FX fees, this isn't something you need to think about. The rate doesn't change based on what day it is—you just spend, and the cashback comes back to you regardless - whether it's a Tuesday or a Sunday afternoon before your flight.

The smarter setup in 2026

At some point, the de facto travel advice stopped making sense and nobody sent a memo.

Here's a good reason to review how you actually spend overseas. Does your current card charge 3% on every foreign transaction? Are you still queuing at the money changer for every trip? Topping up your wallet the night before a Sunday departure? Small habits can mean real costs.

FYI. The Mari Credit Card is worth checking out if you're due for an update. New users get up to S$80 in rewards when they sign up. Plus, get extra S$8 with the promotional code [MCCMST26]. Check out their site for more details.

This post was written in collaboration with MariBank. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best information in order for you to make personal financial decisions with confidence.

Found this useful? Pass it along to a friend or family member still doing the Mustafa Centre queue before every trip—they'll thank you for it.

Related Articles