What would you do if the $12,000 you’d earmarked for childcare disappeared overnight?

That’s what happened to one new parent who posted on Reddit:

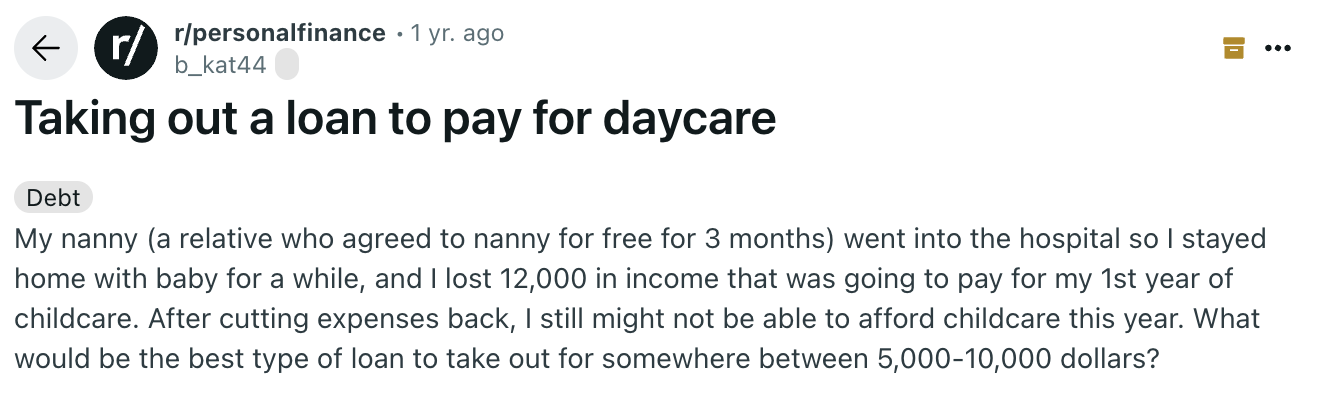

Image: Reddit

Though this Redditor is from overseas, it’s a story that hits close to home for many new parents in Singapore. The costs of having a baby—hospital bills, baby gear, nursery set-up, and more—are already high. Add a sudden change in income or support, and the numbers can get overwhelming.

This is where some turn to personal loans—not as a rash decision, but as a buffer to tide them over during difficult times. In this article, we explore how a loan can support baby-related expenses without draining your savings, based on real-life scenarios from the parents of Reddit.

Using a personal loan to manage baby expenses

- Scenario #1: Affording childcare

- Scenario #2: Supporting temporary loss of income

- Scenario #3: Paying for fertility treatments

- Scenario #4: Taking a loan to support a housing upgrade

Scenario #1: Using a personal loan to afford childcare

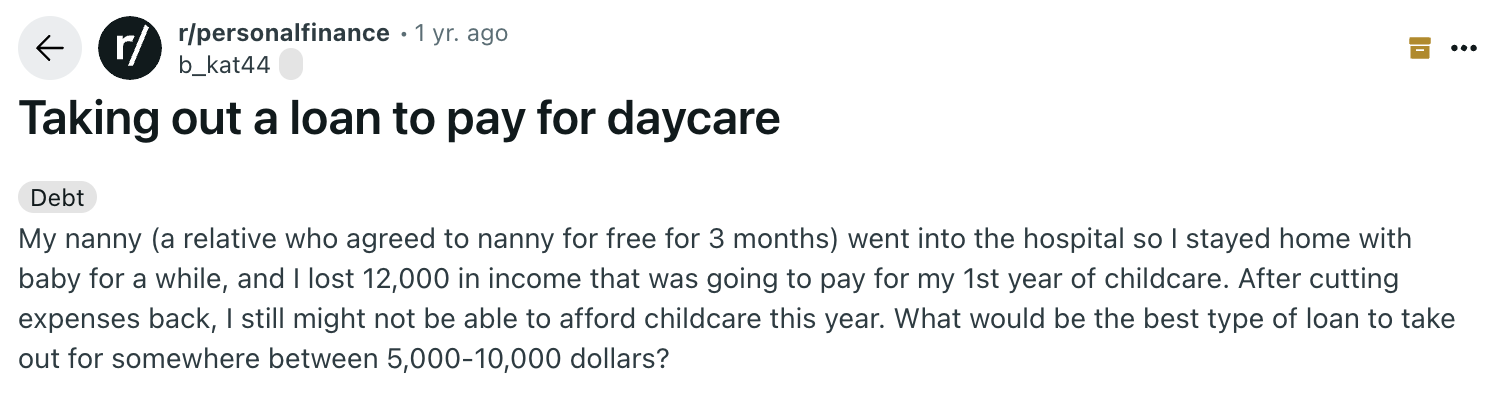

Image: Reddit

Let’s start with the Redditor who lost the $12,000 they had mentally set aside for childcare needs. This was an unexpected development as their relative—who had agreed to provide free nanny care—had to be hospitalised. This new parent thus had to stay home with the baby, which led to the loss of $12,000 in income that they had originally set aside for a year of childcare. They’re now considering a $5,000 – $10,000 loan to help close the gap.

In Singapore, childcare costs can be up to $720 and $800 per month respectively for anchor and partner operators. If you’re looking at premium childcare centres, monthly fees can even exceed $2,500!

If we take $1,000 as a ballpark figure, it’s reasonable to assume a new parent needs $12,000 to pay for 1 year of childcare. This is no small sum—and it’s a sum that can feel even more insurmountable when one has just experienced a sudden loss in income.

Instead of slashing expenses to the bone or hoping for a new high-paying job to appear quickly (can you imagine the stress?), a personal loan can cover the $12,000 childcare cost by spreading it over manageable monthly payments.

Let’s say our new parent takes a $12,000 GXS FlexiLoan, which interest rates start at 2.88% p.a. (EIR from 5.45% p.a.), over 3 years (36 months). Here’s how it could look:

- Monthly repayment: $362

- Total interest paid: $1,036.80

- Total repayment over 3 years: $13,036.80

Instead of struggling to pay $1,000 every month, the parent only needs to come up with $362—a smaller, predictable, and more manageable sum. That breathing room can be a game-changer—it reduces financial stress, preserves emergency savings, and allows parents to focus on adjusting to life with a new baby, rather than scrambling to plug every gap at once.

Plus, if this parent finds a higher-paying job later, they can repay the loan early without penalty—this is one of the GXS FlexiLoan’s unique features.

Per Month ²

S$362

- Interest Rates ¹

EIR: From 1.84% p.a. - From 1.00% p.a.

- Total Amount Payable

- S$13,036.80

- Processing Fee ²

- S$0

- Per Month ²

- S$362

Scenario #2: Using a personal loan to support temporary loss of income

Image: Reddit

This next parent-to-be has a different problem. While the previous was trying to figure out how they could afford childcare, this one has no affordable childcare in sight. She’ll likely be home for 6 to 12 months after giving birth—while juggling a newborn and full-time MA studies. She says remote jobs are scarce, and her time is even scarcer with a newborn on her hands. So now she’s wondering: could a personal loan help bridge the income gap this year?

Let’s say the author’s partner earns $4,000 a month. The author herself is a full-time Masters student, so I’m assuming she won’t have time to work—even remotely. Here’s a breakdown of some key first-year estimated baby- and pregnancy-related costs:

Expense | Low estimate | High estimate |

Maternity clothes | $350 | $400 |

Baby clothes and products | $1,500 | $1,500 |

Diapers | $900 | $1,500 |

Formula | $1,600 | $3,600 |

Maternity insurance | $390 | $870 |

Delivery and hospital stay | $4,240 | $17,260 |

Confinement Nanny (1 month) | $2,800 | $3,900 |

Postnatal massages (5-day treatment) | $300 | $500 |

Total | $12,080 | $29,530 |

Let’s take the midpoint value of around $20,800 for the first year. The couple would need to come up with around $1,733 each month, which is a sizable chunk especially when you consider they may only have a single income to live off while the author does her MA. Not to mention, a lot of the $20,800 needs to be paid upfront—delivery and hospital fees, the confinement nanny and postnatal massages can easily come up to a 5-figure sum already.

Instead of struggling to cough up the money, the couple can take a CIMB Personal Loan of $21,000. With interest rates from 2.68% p.a. and no processing fee, their total repayment would be $22,688.40 over the loan tenure.

That works out to about $630 per month, which can be easier to manage than scrambling for lump sums or draining emergency savings. Plus, there's no early repayment penalty—so if their income improves sooner (say one parent lands remote work or completes studies), they can pay off the balance early and save on interest.

Per Month

S$601

- Interest Rate

EIR*: From 1.94% p.a. - From 1.00% p.a.

- Total Amount Payable

- S$21,630

- Processing Fee

- S$0

- Per Month

- S$601

This loan doesn’t just plug a gap—it gives the couple predictability, peace of mind, and the flexibility to plan the year ahead without panic budgeting.

Scenario #3: Using a personal loan to pay for fertility treatments

So far we’ve talked about expenses post-baby, but let’s take a step back now. Way back. What if you’re looking at a loan to help you conceive?

Image: Reddit

Here we have a Redditor describing their friend, who is single, supported by her parents, and wants to have a baby. She’s deciding to make this happen via in-vitro fertilisation (IVF), which is a process where an egg is fertilised outside the body and then placed into the womb to help start a pregnancy.

If that sounds complicated and difficult, the cost of IVF shows it too. According to SMG Women’s Health, one IVF cycle can cost $13,000 to $15,000 if you go the private route. You can use MediSave to offset some of the costs, but up to withdrawal limits of $6,000 for the first cycle, $5,000 for the second, and $4,000 for the third and subsequent cycles. That means your first 3 cycles can still cost up to $9,000, $10,000, and $11,000 respectively, or a total of $30,000.

One way to fund this $30,000 treatment is through a personal loan. One of the lowest interest rates now is the Standard Chartered CashOne loan, which interest rates start from 1.90% p.a. (EIR: 3.63% p.a.). The Redditor’s friend isn't in Singapore, but if she were and took up this loan, she could borrow $30,000 to be repaid over a set tenure of 3 years with no processing fees. With interest, the total cost comes to $31,710, and she only has to pay a monthly repayment of $881.

(1).png)

Per Month

S$856

- Interest Rate

EIR*: From 1.75% p.a. - From 0.90% p.a.

- Total Amount Payable

- S$30,810

- Processing Fee

- S$0

- Per Month

- S$856

Sign up via MoneySmart and claim:

Up to S$5,725 Cash OR 19,050 SmartPoints (enough to redeem Apple iPhone 17 Pro Max and more) T&Cs apply.

Bonus promotion:

- Up to 1.61% cashback of your loan amount

- Only applicable to loans over S$18,000 with a 3 to 5 year tenure

- New-to-card and new-to-loan customers only

T&Cs apply.

While sinking $30,000 into IVF treatments is a big commitment, the loan makes this deeply personal goal possible—without waiting years to save up or draining her monthly income. It also spreads out the cost into manageable payments, allowing her to pursue parenthood on her own terms, while maintaining stability in her lifestyle.

Scenario #4: Using a personal loan to support a housing upgrade

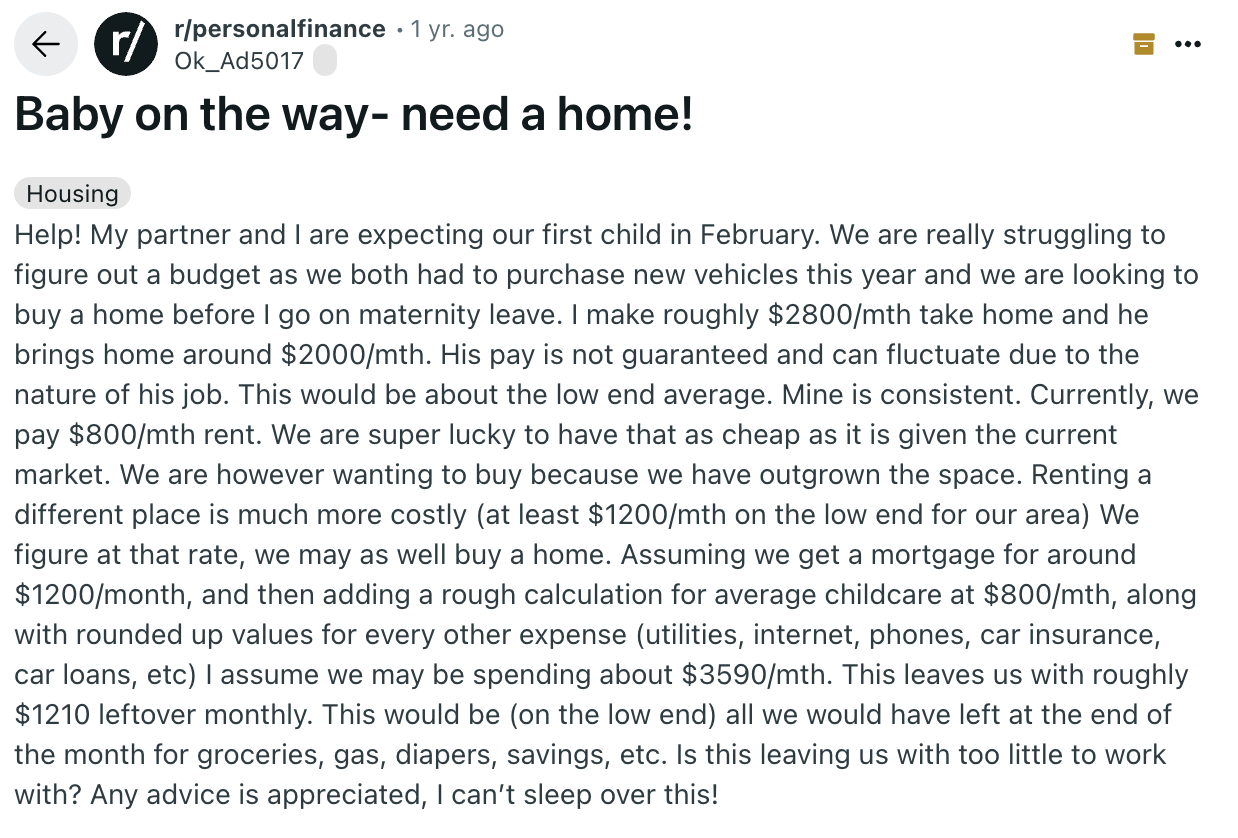

Image: Reddit

This Redditor and their partner are expecting their first child and trying to budget through a series of big financial moves. They both recently bought cars (yup, this isn’t in Singapore) and are planning to purchase a home before maternity leave. Together, they earn about $4,800/month, but only one income is stable. Estimated monthly expenses if they proceed with their house upgrade include:

- Housing: $1,200 per month

- Childcare: $800

- Other fixed expenses (utilities, internet, phone, insurance, car loans, etc.): $1,590

- Total fixed costs: ~$3,590

That leaves just $1,210/month for everything else—groceries, fuel, diapers, and savings. Understandably, they’re losing sleep over whether that’s enough.

Here’s the thing. I can’t speak for their situation where they’re at, but if this were Singapore, even the $1,200 they set aside for mortgage wouldn’t be enough. Let’s assume the couple is going to purchase a $600,000 4-room resale flat.

- Downpayment (25%): $150,000

- Loan amount (75%): $450,000

The downpayment they need to pay upfront is $150,000, which for the sake of continuing this analysis we’ll assume they have in savings or CPF. This leaves $450,000 they need to borrow.

Now assume they take an HDB loan at 2.6% interest and repay it over 25 years—that’s a monthly repayment of about $2,042. (Don’t stress about the math, just use our mortgage calculator.) If we put $2,042 into housing instead of the original $1,200, they’re left with just $368 a month for other everyday expenses. With a baby on their hands too, that sum isn’t going to be anywhere near enough.

I wouldn’t be too quick to advise the couple to take up a personal loan on top of a mortgage if it just leads to them inflating their lifestyle and living situation beyond their means. What they could do instead is to find somewhere to rent for the original $1,200 each month. This upgrades the home environment for their baby, while still giving them a $1,210/month buffer for everything else.

If that $1,210 per month is still tight for them, they could take a personal loan to manage early cash flow—arguably the couple’s biggest challenge. With a new baby, maternity leave, and higher rental fees all hitting at once, a personal loan could help smooth out the first year—covering childcare, baby expenses, or emergency costs while keeping their monthly budget predictable.

For example, the couple could borrow $10,000 with a Trust Instant Loan at 2.22% p.a. interest (EIR: from 4.22% p.a.). As the name suggests, they’ll get their cash instantly for immediate financial relief. They can repay it over 3 years at $296/month (total payable: $10,666, no fees), giving them the breathing room to manage big one-time costs without draining their savings. Think large upfront expenses like hospital bills, infant care deposits, stroller/cot bundles, and maternity confinement meals.

Per Month

S$286

- Interest Rate*

EIR: From 2.28% p.a. - From 1.00% p.a.

- Total Amount Payable

- S$10,300

- Processing Fee

- S$0

- Per Month

- S$286

Sign up via MoneySmart and claim:

Up to S$1,700 Cash via PayNow OR 19,050 SmartPoints (enough to redeem Apple iPhone 17 Pro Max and more) T&Cs apply.

Bonus promotion 1:

- Get S$10 FairPrice E-Vouchers (use promo code MONEYSMT)

- New-to-Trust customers only. T&Cs apply.

Bonus promotion 2:

- Get up to S$10,000 Cashback Scratch Card

- New-to-Trust & selected Existing customers only. T&Cs apply.

For many new parents, the peace of mind that comes from knowing these early essentials are covered—without blowing the budget—is worth the cost of borrowing.

Exploring personal loans? Do it efficiently using our personal loan comparison tool.