You’ve probably heard the old saying, “Save for a rainy day.” Well, in Singapore, that could mean anything from a sudden downpour drenching your lunch plans to an unexpected financial storm. And that’s exactly what an emergency fund is for—your financial umbrella when life throws you a curveball.

An emergency fund is a stash of money set aside for, well, emergencies—medical mishaps, sudden job loss, or any unexpected expense that your regular paycheck can’t immediately cover.

Financial pros often recommend having at least 3 to 6 months’ worth of salary saved up. But is that enough? Some say no, and here’s why: When a crisis hits, it’s not just about how much you’ve saved—it’s also about how quickly and easily you can access it.

The hidden flaws of an emergency fund

An emergency fund is a financial lifesaver, but it’s not perfect. If you’re not careful, it can lose value, slow your financial growth, or even become an excuse to spend.

First, there’s an opportunity cost. Cash sitting in an emergency fund usually earns minimal interest, and inflation quietly eats away at its value. Over time, this means your safety net might not stretch as far as you think when you actually need it.

Then, there’s the false sense of security. Having a financial cushion is great, but it can also make you too comfortable. If you know there’s backup cash, you might feel less urgency to increase your income or cut back on unnecessary spending—stalling your financial progress in the long run.

And let’s talk about discipline. Without clear rules, it’s easy to justify dipping into your emergency fund for things that aren’t real emergencies. A last-minute holiday? A new phone? A “limited-time” deal? Before you know it, your safety net turns into a glorified spending account.

At the end of the day, an emergency fund is there for when things go wrong—not for whenever you feel like treating yourself. Keep it protected, use it wisely, and make sure it’s there when you need it.

Mitigating these drawbacks

A well-managed emergency fund keeps you prepared without holding you back. Here’s how to make sure yours works for you, not against you.

1. Keep the right balance

Aim for 3 to 6 months’ worth of expenses, but don’t let extra cash sit idle. If your income, expenses, or inflation rates change, adjust your fund accordingly. Any surplus? Park it in smarter financial instruments instead of letting it collect dust in a regular savings account.

2. Protect your savings from inflation

Instead of keeping everything in a low-interest savings account, diversify into liquid yet growing assets. Options like money market accounts, short-term bonds, or high-yield savings accounts keep your funds accessible while offering better returns. The goal? Easy access and steady growth.

3. Set clear spending rules

Your emergency fund is for actual emergencies—medical bills, job loss, urgent home repairs. If you don’t set boundaries, it’s easy to convince yourself that a new phone or a last-minute vacation somehow qualifies. Pro tip: Define what counts as an emergency before you need to tap into your fund.

4. Have backup liquidity options

Even the best emergency fund might not cover everything, so it’s smart to have other options:

- Credit cards can help in a pinch—but only if you can pay off the full amount on time to avoid interest charges.

- Borrowing from friends or family is an option if you’re comfortable with it. Otherwise, it could strain relationships.

- Personal/Instant loans often come with lower interest rates than credit cards, making them a structured fallback for bigger, unavoidable expenses.

Managing an emergency fund isn’t just about saving—it’s about making sure your money works for you while staying ready when life throws a curveball.

Why a flexible loan like Trust Instant Loan can be a smart safety net

Fast cash when you need it

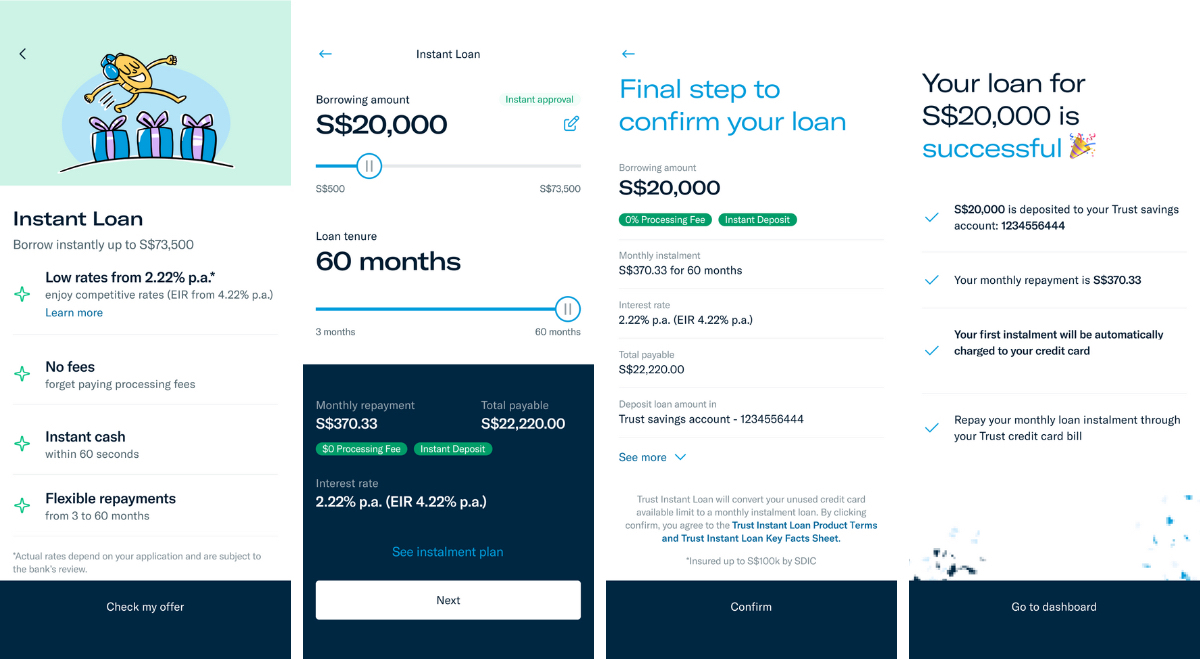

Emergencies don’t wait, and neither should you. Trust Bank’s Instant Loan ensures you get instant approval and cash in just 60 seconds—so you’re covered exactly when you need it.

If you’re already a Trust customer, the funds go straight into your Trust savings account^ within a minute. New to Trust? No stress. Just sign up with Singpass—the whole process is fast, and no tedious paperwork or credit score documents are needed.

The Trust app allows users to open an account, receive a digital card within minutes, and access instant personal loans in just 60 seconds. Image: Trust

Plus, you can use the in-app loan calculator to check your monthly instalment before committing. Once approved, track everything—your repayment schedule, outstanding balance, and more—directly in the Trust App.

^ Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law.

Flexibility on repayments

Unlike many traditional loans that set rigid repayment schedules, Trust Instant Loan gives you the flexibility to choose a loan tenure between 3 to 60 months. You can also tailor your repayment date to fit your pay cycle so you’re never caught off guard. For example, setting the repayment day just after you receive your salary can help you manage your finances better and avoid unnecessary spending.

Save on interest by repaying early

Don’t need as much as you initially thought? Paying it off early can save you on interest—even with a small early repayment fee. Here's an easy example:

Sara takes a Trust Instant Loan of $10,000 to pay off emergency medical bills.

The loan details are as follows:

- Loan Amount: $10,000

- Interest Rate: 2.22% p.a.

- Effective Interest Rate: 4.22% p.a.*

- Loan Term: 60 months

If Sara pays off the loan over 60 months, she will pay a total of $11,110 (including interest).

Item | Amount |

Loan amount | $10,000 |

Monthly repayment | $185.17 |

Total interest paid (based on 2.22% p.a. (EIR 4.22% p.a.*)) | $1,110.00 |

Total amount paid | $ 11,110.00 |

*Effective Interest Rate (EIR) is calculated based on a loan amount of S$5,000 and loan tenure of 60 months from 1 Jan 2025.

Now, let’s see what happens if Sara repays early, after 8 months.

The early repayment fee is 3% of the outstanding principal, and she’s already paid some interest during those 8 months.

Item | Amount |

Total amount paid (8 months) | $1,481.36 |

Interest paid in 8 months | $266.30 |

Remaining Principal to repay | $8,784.94 |

Early repayment fee (3%) | $263.55 |

Total Amount Paid | $10,529.85 |

Here’s the difference Sara pays.

Scenario | Total Paid |

Without early repayment | $11,110.00 |

With early repayment (8 months) | $10,529.85 |

Amount Paid Difference | $580.15 |

Important disclaimer

Actual savings depend on how your loan is structured, how interest is calculated, and any additional fees your lender might charge. Bottom line? Always check with your bank or lender before making an early repayment—you want to be sure it’s saving you money.

Being financially prepared isn’t just about saving

Being financially prepared isn’t just about stashing away savings for a rainy day—it’s about having options when the unexpected hits. An emergency fund is your first line of defence, but having flexible financial tools, like the Trust Instant Loan, can help you weather the storm with ease. It’s all about maintaining control over your finances without adding stress to an already stressful situation. After all, sometimes backup plans need backups too.

Per Month

S$286

- Interest Rate*

EIR: From 2.28% p.a. - From 1.00% p.a.

- Total Amount Payable

- S$10,300

- Processing Fee

- S$0

- Per Month

- S$286

Sign up via MoneySmart and claim:

Up to S$1,700 Cash via PayNow OR 19,050 SmartPoints (enough to redeem Apple iPhone 17 Pro Max and more) T&Cs apply.

Bonus promotion 1:

- Get S$10 FairPrice E-Vouchers (use promo code MONEYSMT)

- New-to-Trust customers only. T&Cs apply.

Bonus promotion 2:

- Get up to S$10,000 Cashback Scratch Card

- New-to-Trust & selected Existing customers only. T&Cs apply.

For a limited time only, grab a bonus of S$250 cash on top of your exclusive welcome rewards when you apply for the Trust Instant Loan with MoneySmart.T&Cs apply. |

Need a flexible personal loan? Check it out here.

Related Articles