Looking for a man in finance? As far as money is concerned, there are far worse partners you could choose than someone without a trust fund.

Financial red flags are a dime a dozen. Take this story I read of someone buying a pretty expensive car from his friend before he got his driving licence. We don’t know if he ever got his licence. Yikes.

Then there’s this story of a couple that tried to buy a waterfront apartment when they were collectively swimming in $100,000 of credit card debt. Operative word: tried. They were closer to declaring bankruptcy than getting their mortgage approved!

Financial issues in Singapore are a huge detriment to relationships. Based on a MoneySmart study in Jun 2024, 58% of Singaporeans have argued about money with their partner and at least 1 in 4 have had a relationship fall apart due to financial disagreements. It looks like love can’t weather every storm after all—not when your bank accounts are running dry.

There are lots of fish in the sea, but let’s save ourselves the heartbreak. After all, according to our survey, 60% of Singaporeans wouldn’t even get into a relationship with someone who’s bad with their finances. When you know how to spot a bad fish, you know to go fishing somewhere else.

So what are the biggest financial red flags out there that scream “I’m terrible with money!”? Here are 13 of the biggest money issues we found.

13 Financial Red Flags and Issues for Couples in Singapore

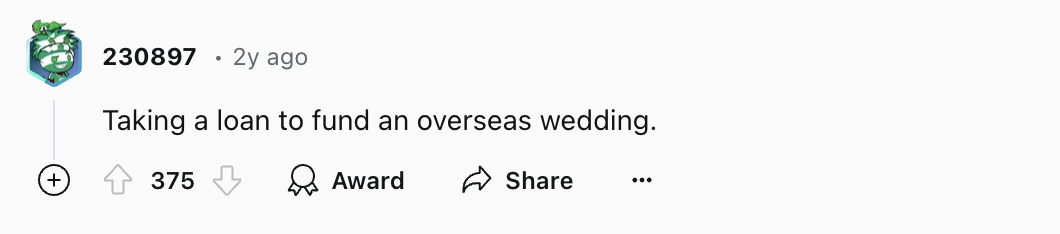

- Red flag #1: Taking a loan to fund your wedding

- Red flag #2: Getting a phone “for free” with a mobile plan

- Red flag #3: Not doing the math

- Red flag #4: Borrowing money from friends

- Red flag #5: Just paying the minimum credit card repayment

- Red flag #6: Buying a flat with a seaview while $100,000 in debt

- Red flag #7: Having babies just for the Baby Bonus

- Red flag #8: Living paycheck to paycheck

- Red flag #9: Buying lottery tickets

- Red flag #10: Smoking

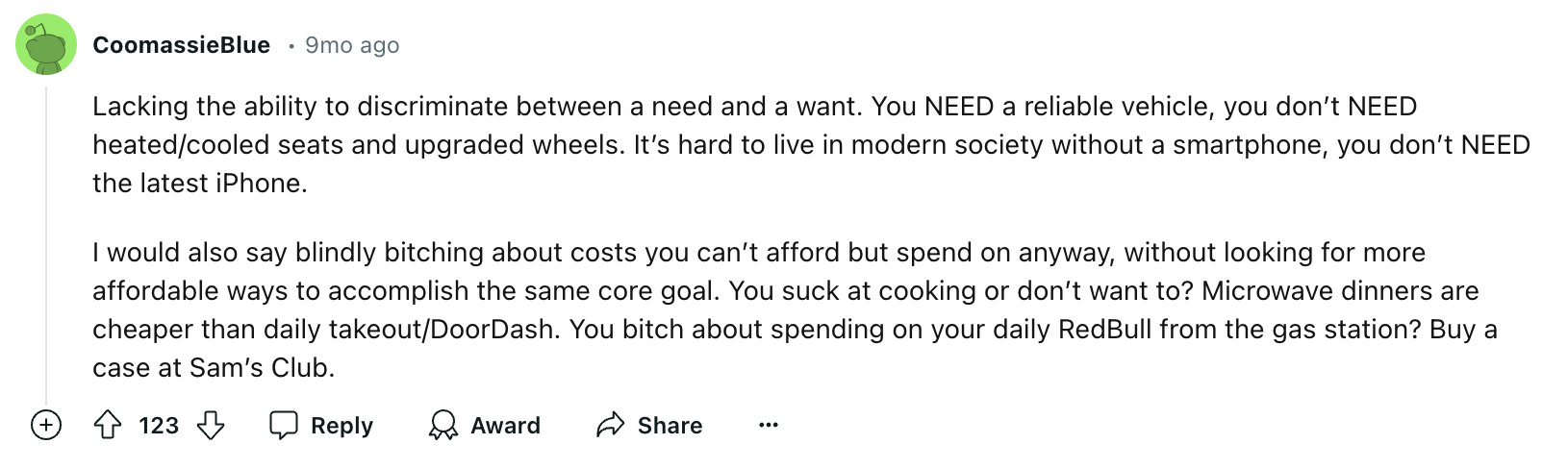

- Red flag #11: Spending tons on flashy cars, Grab, and other unnecessary expenses

- Red flag #12: Rage quitting without securing your next job

- Red flag #13: Being stingy

- So, which is more important—money or love?

Red flag #1: Taking a loan to fund your wedding

Image: Reddit

Loans are not a bad thing in the right context. For example, you might take a home loan to afford your first home, or an education loan to complete your studies. These are good investments because they get you, respectively, a place you can finally call your own and a degree you can proudly hold to your name when you enter the working world. In the long run, these investments are going to bring you bigger returns—your house will appreciate in value, and you’ll have better career prospects for a more competitive salary. I can’t say the same about taking a personal loan out for a destination wedding.

Why it’s a red flag:

Your wedding is just the start of your lives together—after this, you’ll still need to service your mortgage, pay utility bills, and maybe even start a family. You don’t want to start married life already in debt.

So if your partner wants an overseas wedding that you both can’t afford without getting into debt, I strongly suggest you don’t agree to it. If they still insist on taking a loan, red flag!

ALSO READ: Should You Take A Personal Loan To Help With The Rising Costs Of Living?

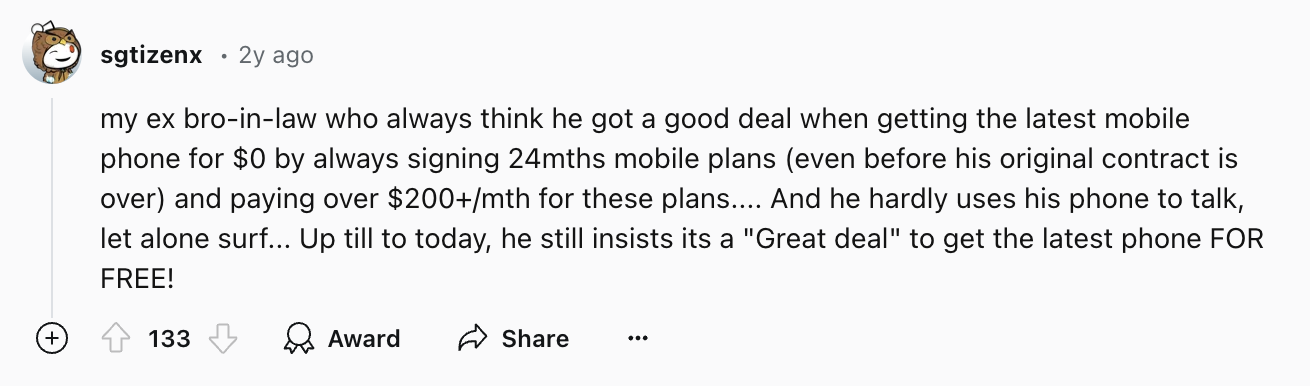

Red flag #2: Getting a phone “for free” with a mobile plan

Image: Reddit

Ah, we all know that guy who pays $200 a month for a phone plan and thinks he got his phone “for free”. I’ve done the math—this “deal” that telco providers cut you is never worth your dollar. You end up paying an extravagant sum every month for data that you could be paying less than $10 a month for instead.

Why it’s a red flag:

It’s okay to get yourself a new phone. The real problem here is that this person isn’t thinking about money logically and mathematically before they spend it.

Speaking of crunching those numbers…

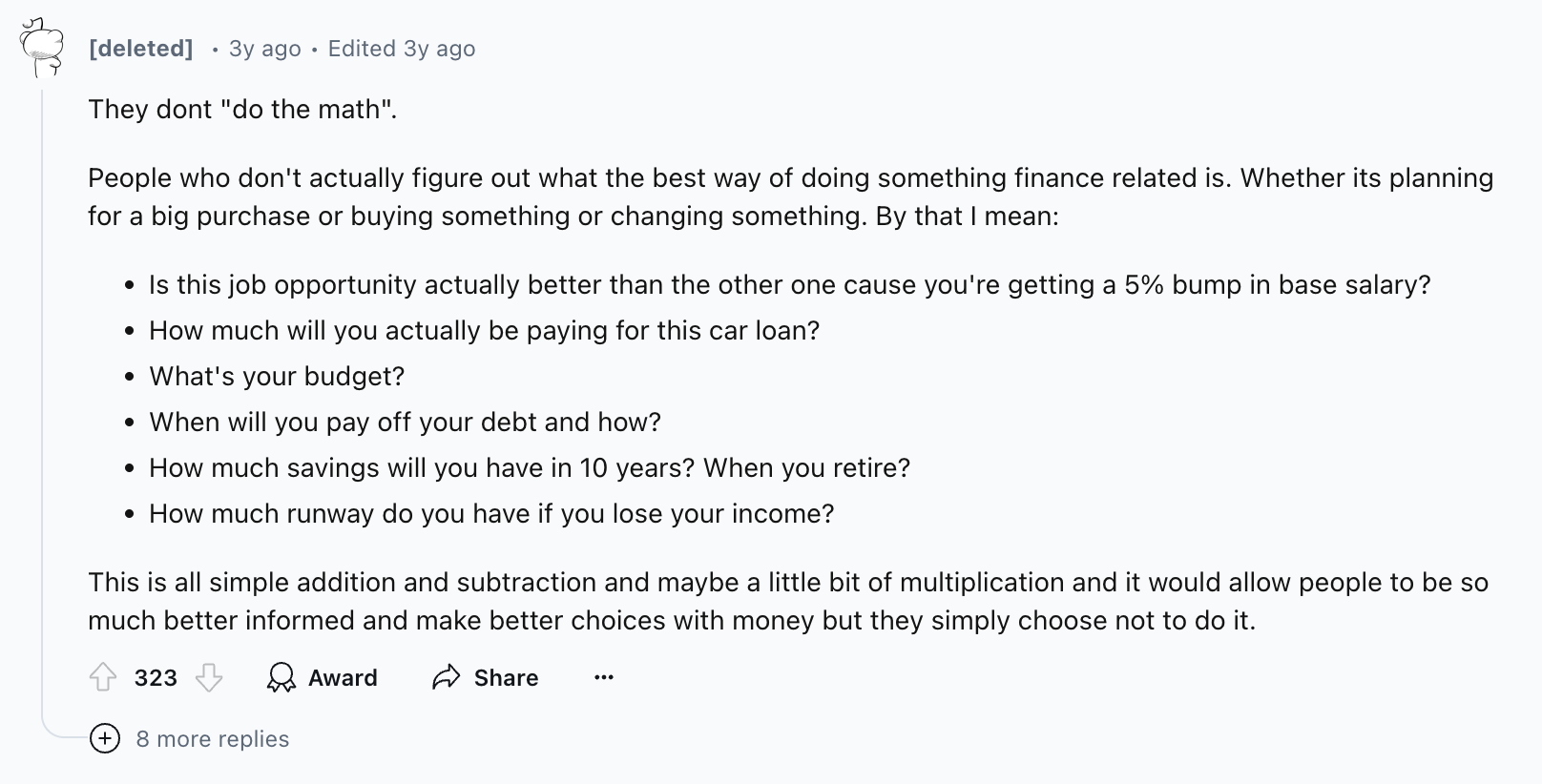

Red flag #3: Not doing the math

Image: Reddit

To me, working out the pluses and minuses is the foundation of financial prudence. You can get away with not doing your calculus homework at school, but your laziness is far more detrimental in real life when budgeting is essential.

Image: Reddit

Don’t tell me that you “it’s too hard and I can’t do it”—not when there are tons of online tools out there to assist you. For example, did you know you can use a stamp duty calculator, mortgage calculator, and Total Debt Servicing Ratio (TDSR) calculator to plan your property purchase?

Even if your situation is more complicated, these days you can even tell ChatGPT your long grandmother story and let it do the calculations for you.

Why it’s a red flag:

If you can’t even be bothered to use online tools or ChatGPT to do your budgeting, you clearly don’t care enough about your finances. No excuses. Do the math, or I’m flagging you red.

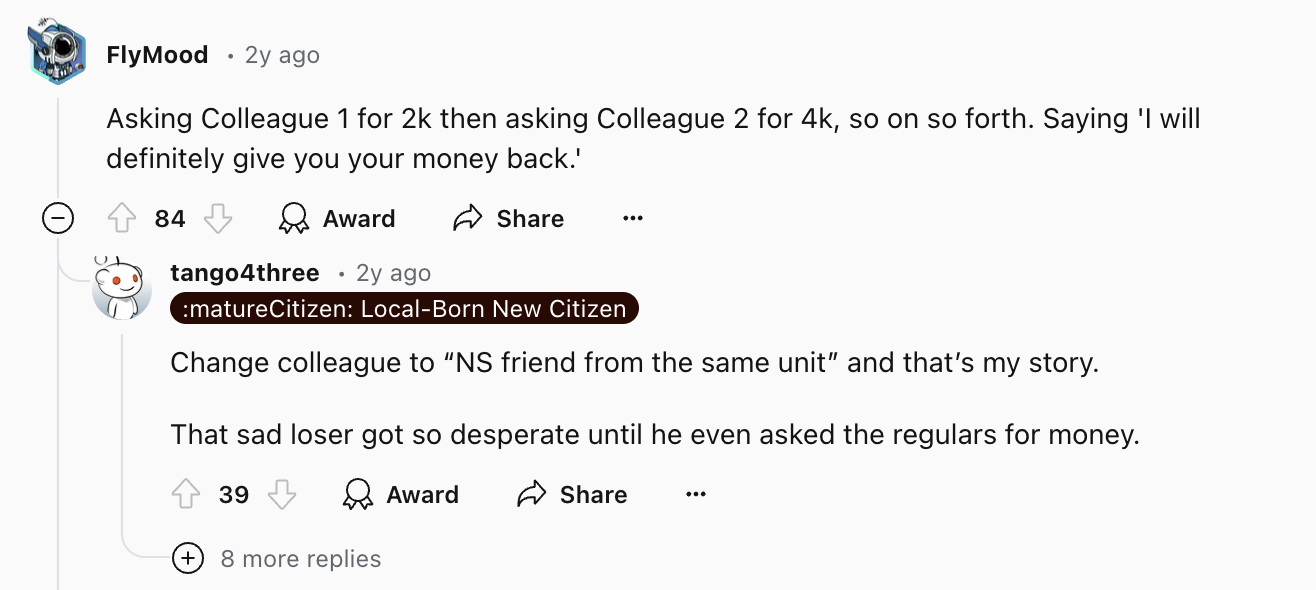

Red flag #4: Borrowing money from friends

Image: Reddit

I’ve experienced this before—but with my fellow prepubescent classmates in primary school! It’s a very different matter when someone borrows money from colleagues as an adult, and the small 20-cent or 40-cent loan has ballooned to include a few extra zeroes.

The problem isn’t in the act of borrowing money itself. For example, one of my father’s close friends recently asked him if he could transfer some money to her PayLah! because her dog had suddenly passed away and she didn’t have access to her bank account at the cremation facility. She transferred the money back to him via online banking within the week. The problem is when people keep borrowing money and don’t pay it back.

Image: Reddit

Even if it’s a small amount, money owed should always be repaid in a timely manner. This holds whether it’s a no-interest loan from friends or the credit card bill you’ve chalked up at the end of the month—we’ll get to that next.

Why it’s a red flag:

A chronic borrower is clearly spending unwisely and unsustainably above their means. They have no idea how to budget and lack the discipline to discern what’s a need and what’s a want. They’re likely to suck your bank account dry due to their poor spending habits!

According to our MoneySmart study conducted in Jun 2024, almost half (48%) of Singaporeans have argued with their partner about one of them spending too much. If you date someone with a red flag like always borrowing and never returning money, I’m pretty sure you would fall into that 48%.

ALSO READ: What Having Unlimited Pocket Money Taught Me About Saving Money

Red flag #5: Just paying the minimum credit card repayment

Image: Reddit

Paying the minimum $50 repayment sum out of the $1,000 on your credit card bill is a terribly bad idea. You’re going to incur a phenomenally high interest rate on the remaining balance—about 27.9%. Did you know that even personal loans have lower interest rates than that, from as low as 4% or 5%?

Not that you should do this, but you’re better off taking a personal loan to fund your monthly spending instead of incurring interest on credit card debt. And anyone who has done the latter is better off taking a personal loan to pay off the credit card debt at one shot, then servicing the personal loan instead.

Why it’s a red flag:

Paying the minimum on a credit card bill means you incur a whopping 27.9% interest. Very un-MoneySmart!

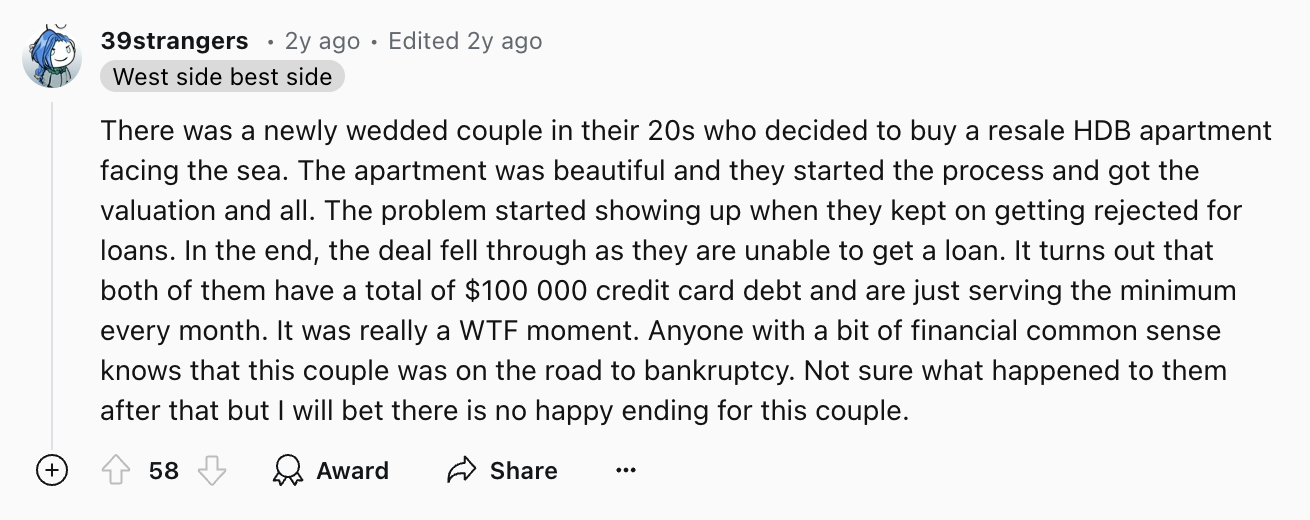

Red flag #6: Buying a flat with a seaview while $100,000 in debt

Image: Reddit

We just talked about credit card debt, but this story takes that to a whole new level. Here we have a couple that’s already incurred $100,000 worth of credit card debt between the both of them, and are only paying the minimum repayment each month. Yet they’re “delulu” enough to try to buy a waterfront apartment together! Of course, they were rejected from getting a home loan for their flat—as they should be. There’s no way they can or should be allowed to buy a house with outstanding debt like that to settle first.

If they are struggling with debt, credit card debt or otherwise, they could instead look into a Debt Repayment Scheme (DRS) to help them manage the money they owe and repay it in a sustainable manner over a course of up to 5 years.

Why it’s a red flag:

If your partner is swimming in debt and thinks it’s a good idea to add more by taking a housing loan, they are as “delulu” as it gets.

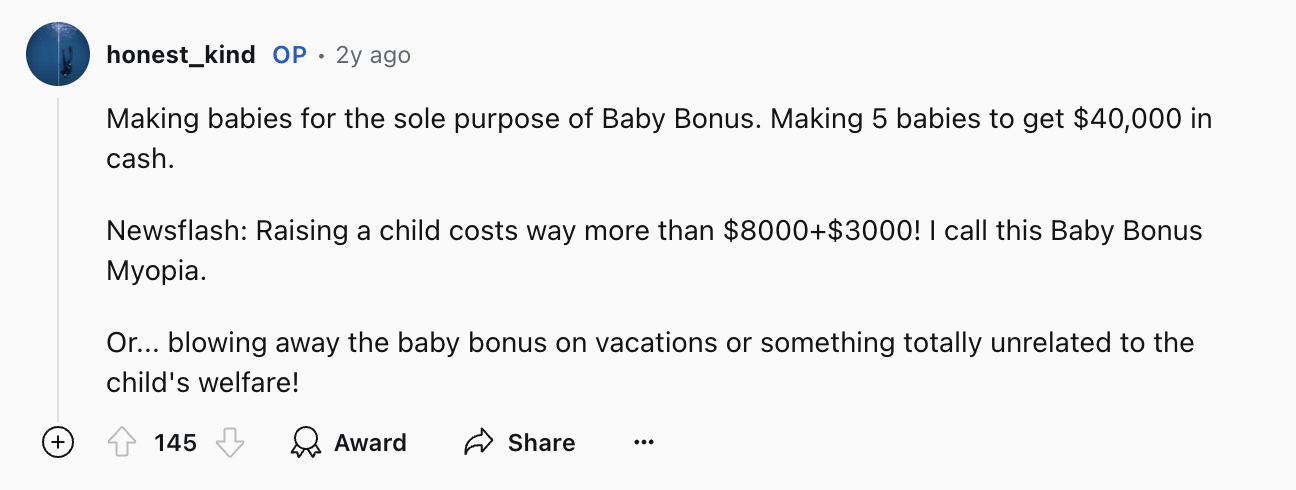

Red flag #7: Having babies just for the Baby Bonus

Image: Reddit

First of all, the primary reason to have a baby cannot be to make money. We’re talking about human life here!

Secondly, you aren’t going to make money from a baby anyway. Far from, in fact. Let me take you through the numbers.

The Baby Bonus Scheme in Singapore currently pays out up to $20,000 for your first child. This figure increases as you have more children, reaching up to $33,000 from your fifth child onwards.

For simplicity, let’s assume we’re looking at a couple’s first foray into parenthood. They might be able to “earn” up to $20,000 from the government, but they could easily blow half of that on the delivery alone in just 3 days at the hospital. Having a baby in Singapore is not cheap. Raising one is even worse. Aside from food, clothes and basic needs, education is going to be a huge expense. It can cost anywhere from $33,000 to $54,000 to complete a degree at a local university—and that’s assuming the kid isn’t studying to be a doctor or lawyer.

Even if one is ready for a fifth, the $33,000 Baby Bonus payout comes nowhere close to the 7-figure sum you’ll probably have to spend on raising a child to adulthood.

Why it’s a red flag:

You should have children because you want children, not because you want the money bonus the government will give you for having them. Besides, the latter is nothing compared to how much it’ll cost you to raise a child!

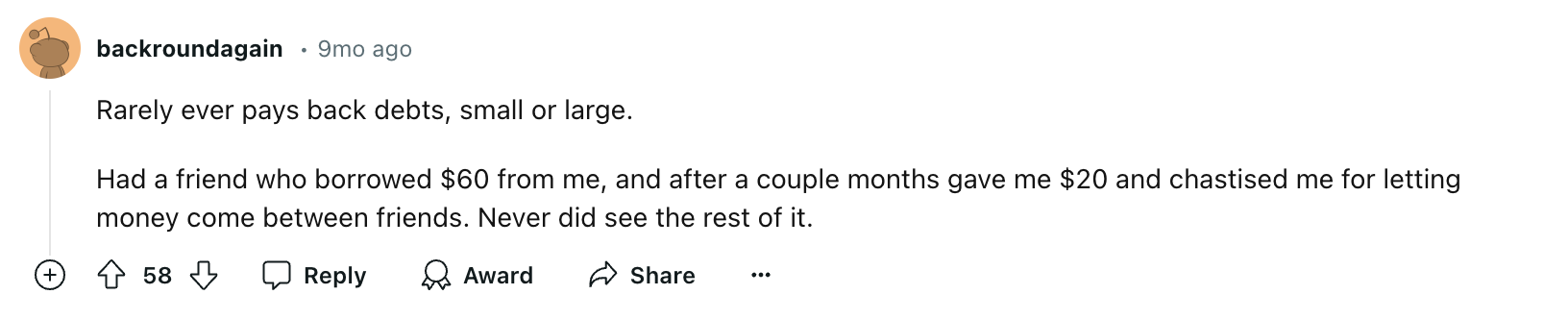

Red flag #8: Living paycheck to paycheck

Image: Reddit

We’ve talked about incurring debt and spending above one’s means, but what if you’re spending exactly what you earn? So you can maintain your current lifestyle, but you don’t save or invest any of your income because, well, there’s no “extra” at the end of the month.

This isn’t as bad as having $100,000 in credit card debt, but it’s not great either. Living paycheck to paycheck usually means you have no savings for unexpected expenses. Without any financial cushion, even small surprises can lead to debt and stress. It makes it hard to save for future plans—for example, how are you going to afford a house downpayment or mortgage?—or enjoy a sense of financial freedom.

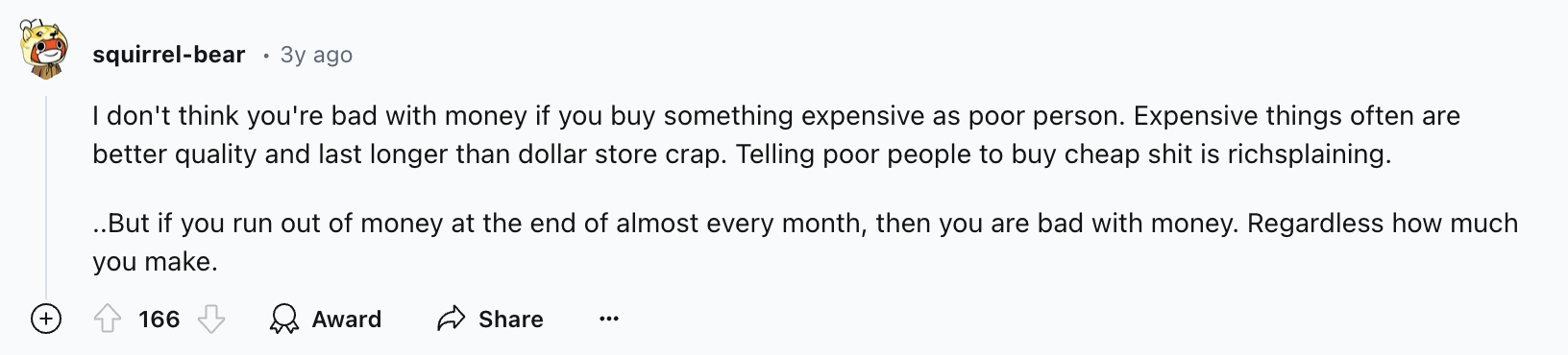

Image: Reddit

As Redditor “squirrel-bear” points out, buying something expensive is not the problem. For example, investing in a good pair of $100 shoes that will last you years is better than buying a poor quality $10 pair every month. The key is to know how to pace yourself and prioritise your expenses so that you still have some savings.

Why it’s a red flag:

Living paycheck to paycheck means you probably don’t have much savings and you aren’t budgeting your money well. This can be due to tough family circumstances or difficulties with getting a job with decent pay, but it’s a red flag if they are living paycheck to paycheck deliberately and don’t see anything wrong with saving $0 every month.

According to our MoneySmart survey, 37% of Singaporean couples regularly argue about differences in saving habits, and almost a third (32%) have argued because one of them hasn’t saved enough money. You need to get on the same page about saving habits, and that must mean actually saving a portion of your paychecks every month.

Red flag #9: Buying lottery tickets

Image: Reddit

Let me ask you this: Would you invest in a scheme in which your returns after 5 years could be anywhere between 50% to -100%? According to our writer’s brief survey among his acquaintances who have bought lottery tickets, that’s the range of returns you can expect to get when you try your luck at the Singapore lottery.

Sure, you could strike it rich and walk away with $10 million, but what are the odds? That wasn’t a rhetorical question. The odds to win first prize are anywhere between 1 in 10,000 for 4D and 1 in 3,983,816 for Toto. That means only 1 person out of almost 4 million is going to bag the big pot of gold. Do you consider yourself the luckiest person in a pool of 4 million? Didn’t think so.

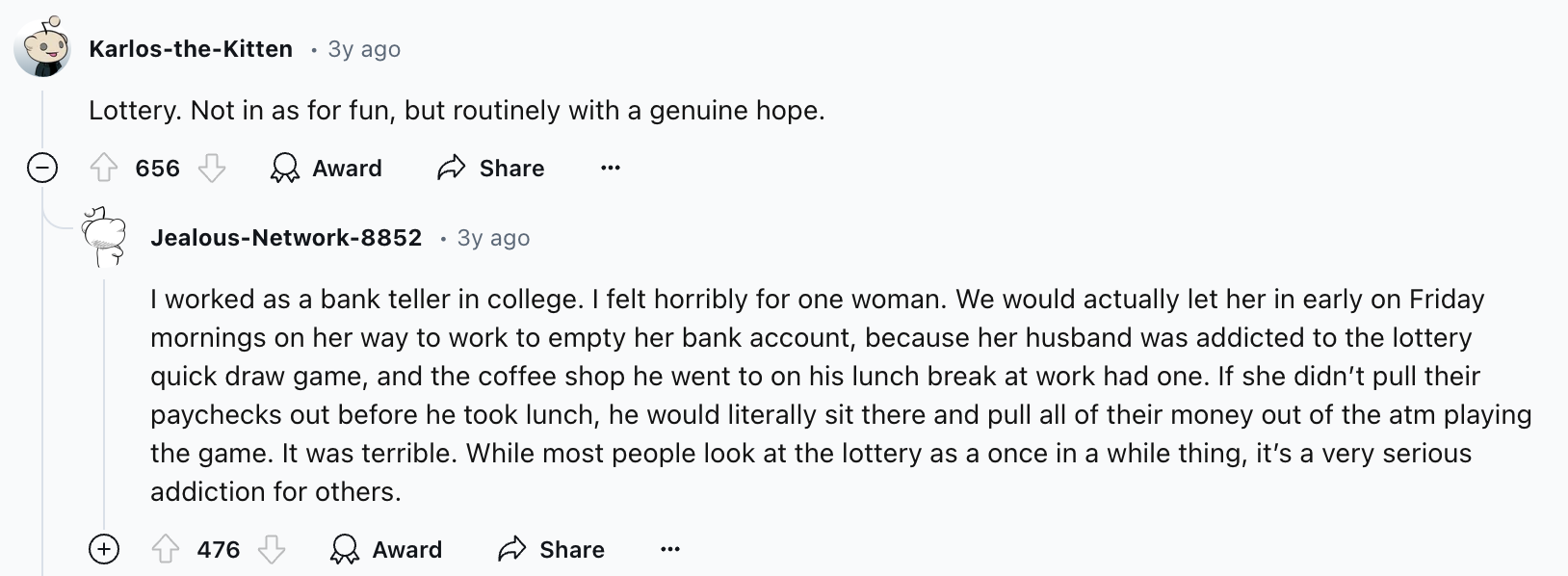

And yet there are people who hang on to that lofty hope: “Just one more—maybe this ticket will be the one!”

It can become a fiercely damaging addiction:

Image: Reddit

Why it’s a red flag:

When it comes to the lottery, the odds (1 in 10,000 to 3,983,816) are never in your favour. I think buying 1 or 2 for funsies is okay, for example if you want to mark a milestone in your life and buy the licence plate number of your first car. But please don’t think you’re actually going to win. And for goodness sake, don’t make it a habit.

Red flag #10: Smoking

I expected to see chronic borrowers and frivolous spenders make this list, but I was surprised to find smoking coming up again, again, and again.

Image: Reddit

Smoking ruins both your financial and physical health. According to Statista, the average retail price of cigarettes in Singapore is about $15. If one were to smoke a pack a day, that’s about $450 spent on cigarettes a month.

Then there’s the thousands you’ll spend on treatment for the life-threatening diseases that smoking puts you at risk for. According to HealthHub, approximately 6 Singaporeans die prematurely every day from smoking-related diseases. These illnesses, including cancer, heart disease, stroke, and Chronic Obstructive Pulmonary Disease (COPD), also known as Chronic Obstructive Lung Disease (COLD), are among the leading causes of death here.

The worst part is that they’re very preventable. In fact, smoking (and its related diseases) is the biggest cause of preventable death in the world.

Why it’s a red flag:

Cigarettes are costly to buy, and related diseases like cancer might cost you your life. (Plus—and this is a personal opinion—smokers just don’t smell good.)

Red flag #11: Spending tons on flashy cars, Grab, and other unnecessary expenses

Image: Reddit

Image: Reddit

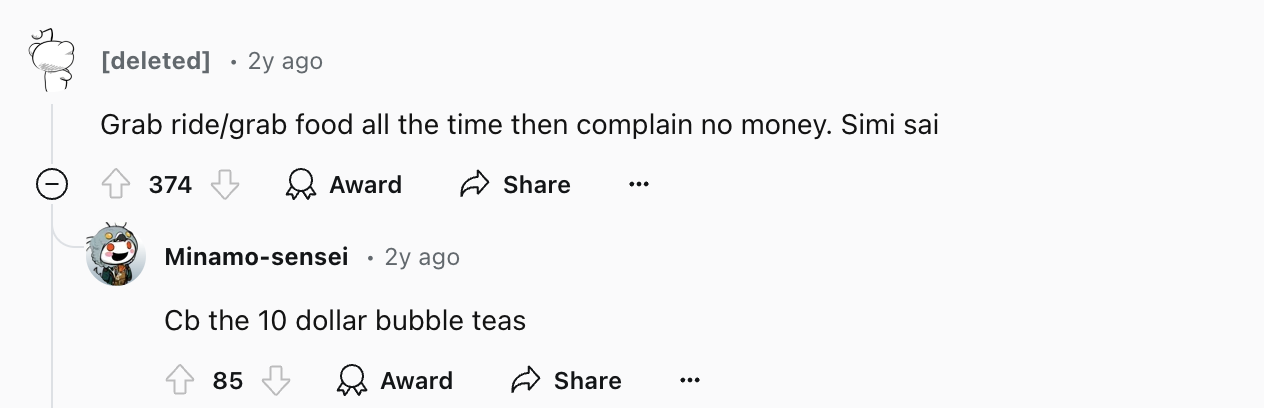

This is a pet peeve of mine. I hate noisy, flashy cars that owners “zhng” to be obnoxiously and unnecessarily loud. Sometimes, the new coats of paint they apply make me convinced both they and the staff at the workshop that did the job must be colourblind. Don’t get me started on the folks who remove their mufflers so that their car engines can make a louder revving sound, with absolutely no effect on functionality. How can something so ugly also be so useless?

The Redditors above also talked about unnecessary or unwise expenses in general. Most of us don't earn enough to be able to justify taking a Grab everywhere or ordering in food delivery everyday. These folks just want convenience, which is why they also tend to buy drinks at convenience stores instead of grocery stores or even dollar stores like ValuDollar. Wanting convenience is fine—if you have the financial means to be able to afford these lifestyle luxuries and still be able to save some money every month.

Why it’s a red flag:

People who spend on form instead of function are spending on wants instead of needs, and that tells me their priorities are not right. Most of us aren’t earning the kind of money that would justify such high expenses just for aesthetics or convenience.

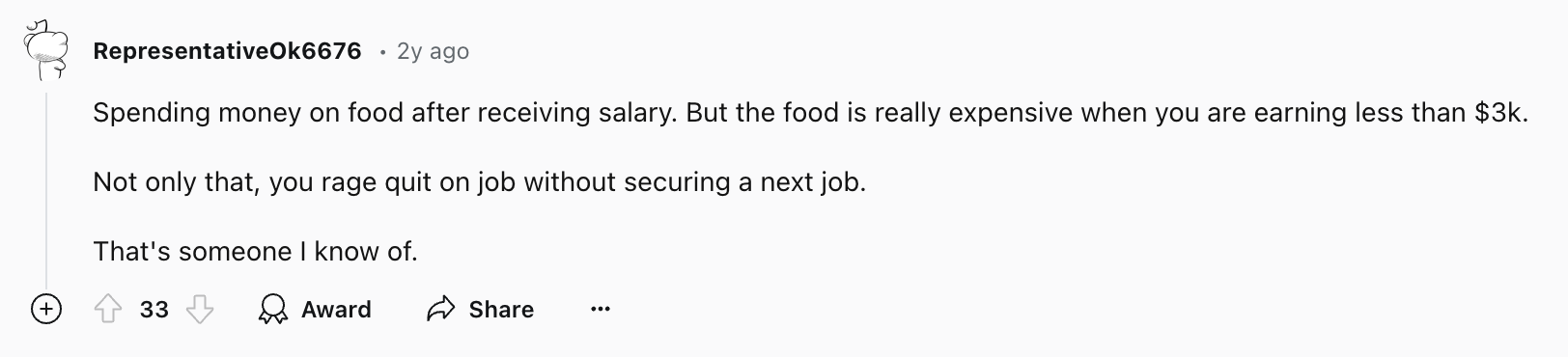

Red flag #12: Rage quitting without securing your next job

Image: Reddit

I’ve heard stories of toxic workplaces where bosses hurl vulgarities at you, micromanage you down to every minute of your workday, and threaten or blackmail you with your job on the line. I’ve told friends subjected to such treatments that they should quit ASAP for the sake of their mental health. So I don’t think suddenly quitting a job is always a red flag.

But It is a red flag if someone just got frustrated over something that can be discussed and worked out and walked out in a fit of anger—especially if they don’t have much savings to tide them over until they find new employment.

The Redditor above also mentioned spending on expensive food after receiving their salary. I’m personally against spending more at the start of the month when you just get paid. I would rather you pace yourself and, if you’re going to splurge a little, spend more at the end when you know you’ve already paid for other necessities (including setting aside some for savings) and still have some extra cash to splash.

Why it’s a red flag:

Barring abuse and blackmail (which you should report to TAFEP anyway), rage quitting a job because you’re unwilling to communicate or have anger management issues tells me that you’re rash and volatile. It’s even worse if you have no savings and spend lavishly too.

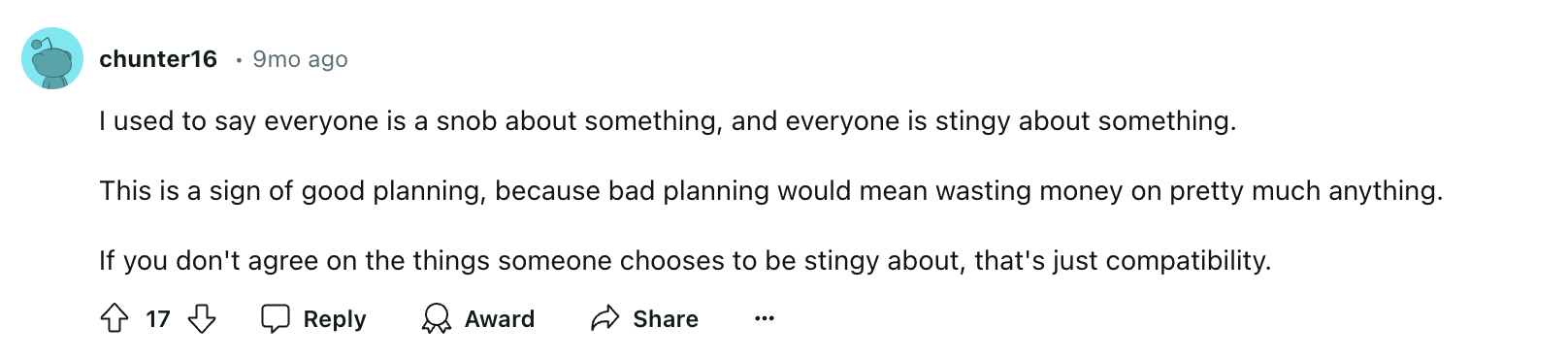

Red flag #13: Being stingy

Image: Reddit

Why it’s a red flag:

Hot take, it’s not. This Redditor raised an interesting point: “everyone is stingy about something. [...] If you don't agree on the things someone chooses to be stingy about, that's just compatibility.”

I’m thinking about how I spend a 3-figure sum every month on dance and guitar classes, while my sister would baulk at such an expense. Or about how my mother is happy to spend $80+ on a fancy high tea set, while my father would much rather spend $80+ buying bags of animal manure to fertilise his garden. (Yes, I just compared high tea to poop.)

The value of money is, in this sense, subjective. My mum might say my dad is “stingy” with his money because he won’t spend on atas dining experiences, while my dad might say she’s “stingy” because she won’t spend a cent on gardening supplies.

This isn’t a huge issue in their relationship because they each have their own hobbies they enjoy separately. But what if they were trying to decide if they should spend $8,000 to renovate the kitchen? Or if they were trying to decide if they should spend $800 on a staycation or $8,000 to travel overseas together? If we consider how they want to spend their money in a meaningful way, the problem of incompatibility might arise.

There are of course cases of extreme stinginess bordering on obsessive, unhealthy behaviours. I once saw a video about a woman who “cooks” lasagna in her dishwasher with her dishes to save on electricity. Spoiler: the lasagna was soggy, wet, and as you can guess, not really cooked.

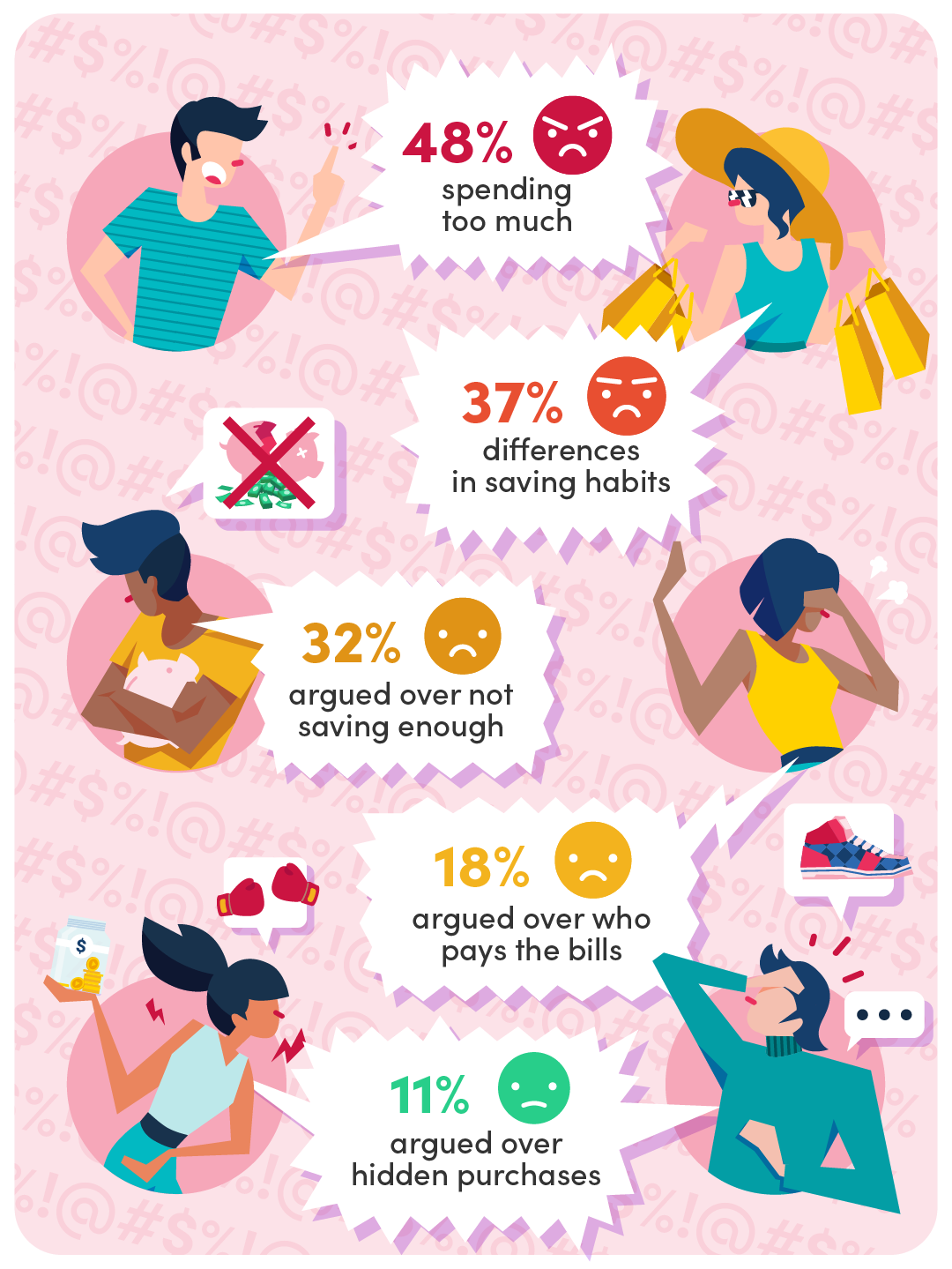

So, which is more important—money or love?

If you ask me, both. According to our MoneySmart survey in Jun 2024, at least 1 in 4 Singaporeans have had a relationship crumble due to money-related conflicts. If you think the love you have is real, reality check: so is money. So is the society you live in that runs on money.

Here are the top reasons we found couples in Singapore fought over financial issues:

At the end of the day, you can’t bank on love alone for a relationship to survive. Love does not conquer all. I don’t believe your partner has to be rich, but they should have a good grasp of how to manage their spending and saving habits in a way that allows the both of you to plan a future together.

For more insights on how finances affect couples in Singapore and tips on how to communicate about money, read the full survey results.

Found this article interesting? Share these red flags with your friends and family!

Related Articles