With concepts like FIRE (Financial Independence, Retire Early), and its offshoot concepts such as Lean FIRE, and Coast FIRE, it’s clear that people just want to be financially independent to live however they want.

But with things like inflation and rising costs of living every year, it’s only becoming harder and harder to achieve financial freedom - especially in an expensive country like Singapore.

Can Singaporeans truly be financially free? And how long will that take the average person to achieve?

A minimum of 27.3 years in fact. Well, according to the Singlife Financial Freedom Index 2023 released on 1 Aug 2023 anyway.

But before we dive deeper into the study, let’s first take a look at what it means to have financial freedom.

What is financial freedom?

Financial freedom is the state of having enough money to live your life comfortably and without worry. It means having enough money to cover your basic needs and expenses, as well as enough money to save for the future, invest in your goals, and take risks. Financial freedom also means having the freedom to choose how you want to spend your time and money.

A key thing to note is that financial freedom is different for everyone. For some people, it might mean being able to retire early and travel the world. For others, it might mean being able to quit their job and start their own business. It could also mean having a plan for the future, such as retirement savings and sufficient funds for your children.

Why do Singaporeans care so much about financial freedom?

Well, we know about the high cost of living here whether it’s food prices, GST or housing. Everyone I’ve met is hustling or trying to hustle. This even extends to the dating scene where I’ve heard stories from friends about how boring some guys are because they're just always talking about making money!

Not that making money isn't good but becoming obsessed with it can be dangerous too.

But for all the buzz about making money and hustling, only a third (29%) of Singaporeans feel that they have achieved financial freedom.

What was Singlife’s study all about?

This was a key finding from Singlife’s Financial Freedom Index 2023. A total of 3,000 Singaporeans and Permanent Residents aged between 18 - 65 were surveyed from December 2022 - January 2023 to “understand the attitudes of individuals from diverse income levels towards achieving financial freedom amidst inflation and the rising cost of living.”

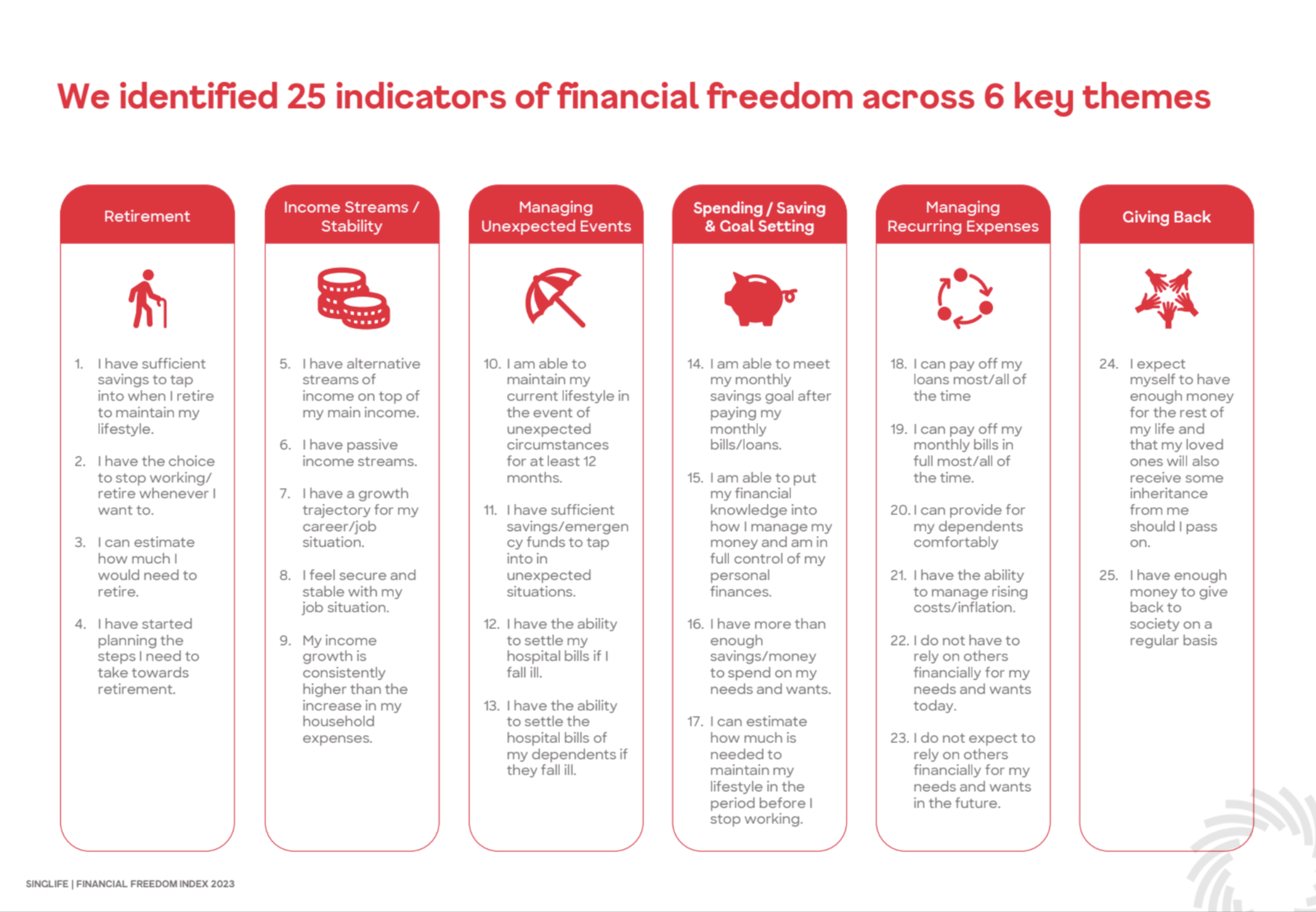

The Index was derived from 25 financial freedom indicators categories under 6 themes of retirement, income streams/stability, spending/saving & goal setting, managing recurring expenses, managing unexpected events, and giving back to society.

It found that for the average consumer to feel financially free, it would take 27.3 years provided they save at least S$1,733 per month to accumulate a median savings of $566,640.

Although 73% of respondents acknowledged the importance of financial freedom, only 29% consider themselves financially free. This group has an average monthly personal income of S$9,067.

Image: Singlife

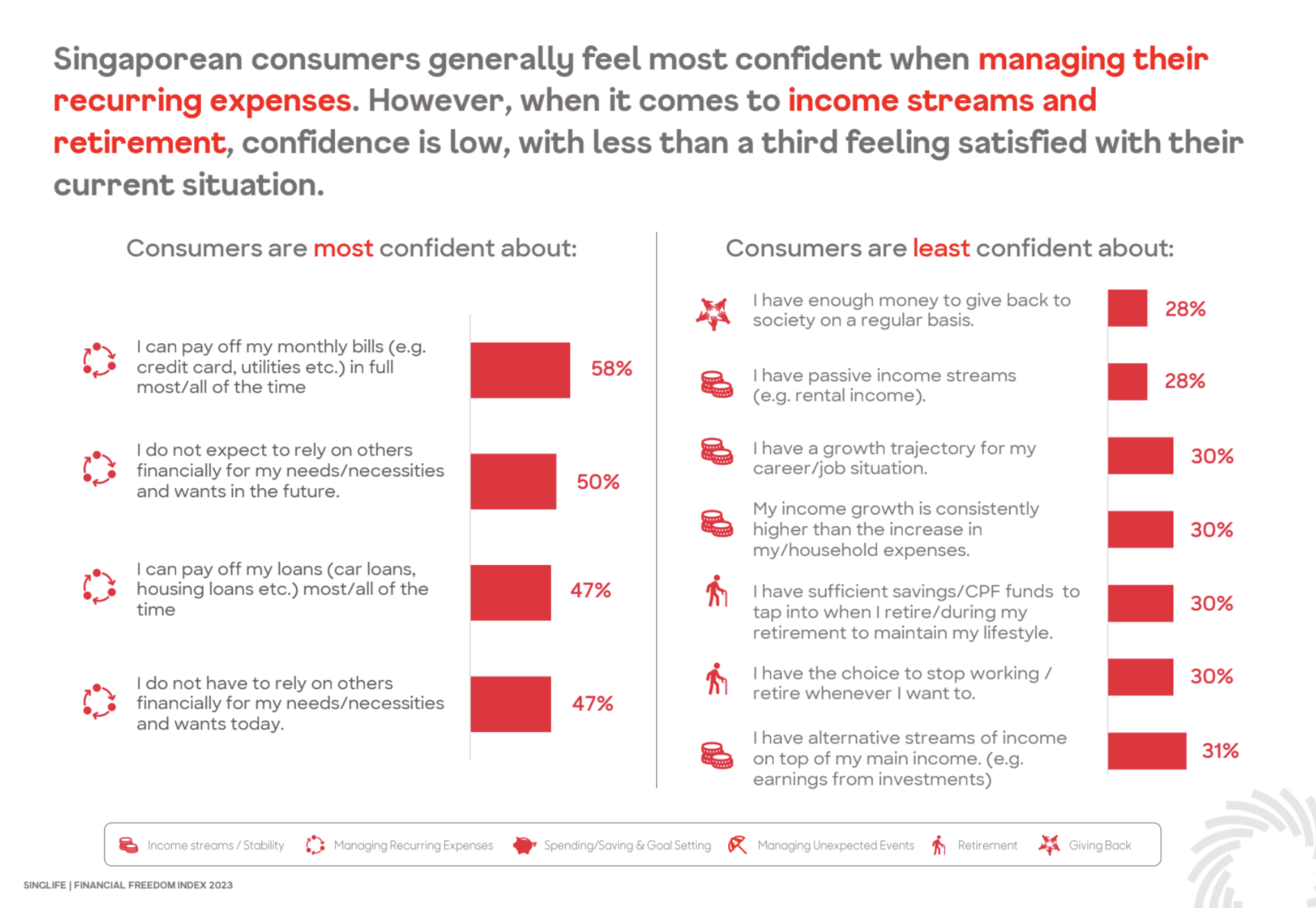

Diving into the specifics of the results, the top 3 ways Singaporeans felt financially free were:

- The ability to pay off monthly bills (credit card, utilities) in full most/all the time (58%)

- Do not expect to rely on others financially for their needs/necessities and wants in the future (50%)

- The ability to pay off loans (car loans, housing loans etc) most/all of the time (47%) + Do not have to rely on others financially for their needs/necessities and wants today (47%)

Where they felt they lacked most were:

- Having enough money to give back to society on a regular basis (28%)

- Have passive income streams (28%)

How long does it take for people in other countries to feel financially free?

While there's no global index of comparison for how many years you need to feel financially free across countries, a popular theory for how much you should have is the 4% rule. According to Investopedia, the 4% rule is a rule of thumb that states that retirees withdraw 4% of their retirement funds each year. And to adjust for inflation, increase that number by 2% each year.

There are also several rankings of the cheapest country to retire in. According to the 2022 Natixis Global Retirement Index, here are the top 10 best places to retire based on health, quality of life, material well-being and finances during retirement.

- Norway

- Switzerland

- Iceland

- Ireland

- Australia

- New Zealand

- Luxembourg

- Netherlands

- Denmark

- Czech Republic

However, some of these on the list are pretty expensive countries, which may not be helpful for financial freedom.

Another website, SmartAsset, has compiled a list of safest and mostaffordable countries to retire in, which are key considerations. After all, you don’t want to live out your golden years somewhere unsafe! The top 10 are:

- Portugal

- Malaysia

- Spain

- Costa Rica

- Panama

- Czech Republic

- Peru

- Slovenia

- Austria

- Australia

So how much do Singaporeans need to be saving every month?

27.3 years sounds fine or daunting depending how old you are. Of course, it's better if the number of years can be reduced whether through salary growth, investments and savings.

A tried and tested budgeting method is the 50/30/20 rule where you allocate 50% of your income to needs, 20% to wants, and at least 30% should be put aside for long-term savings and investments.

This method is a helpful guideline to help you not spend more than necessary and still channel leftovers to savings and growing your money.

Figure out what goes into your needs which can include things like bills, home loan repayment, groceries, utilities, public transport, insurance - basically anything that you have to pay for monthly.

This should leave you with the rest of your salary to portion out for savings and investments.

While the 50/30/20 rule is not a hard and fast one, you can adjust it according to your needs as long as you're not spending more than you're earning and are saving! You can also adjust the 50/30/20 ratio to increase savings and investments if you want to.

Besides this, there are also other simple ways to save:

1. Set financial goals

If you haven't done so already, this will help you start saving and growing your money. Once you know what you want to achieve with your money, you can start making a plan to get there. Do you want to buy a house in 5 years? Are you planning to have a child? Do you need to save for your child's university fees? By having a clear idea of what you want to achieve, you'll have a better idea of how much to save each month.

2. Automate your savings

This makes sure you're saving money on a regular basis. Set up a standing order to transfer a certain amount of money to a high interest savings account or savings plan when you get your salary every month. This way, you won't be tempted to spend the money and you'll be saving without even thinking about it.

4. Invest your money

Investing is a great way to grow your money over time. You'll want to find those that suit your risk appetite and financial goals. Make sure that you also diversify your investment portfolio to spread the risk you take on. Be sure to also do thorough research before you invest.

5. Reevaluate your expenses

Spotify, Netflix, Disney+, YouTube Premium - If you find yourself not having time to use these services as much as you like, it may be time to stop or reduce the number you're subscribed to.

The same goes for things like food and shopping expenses. Eat out less, buy less or buy secondhand - all these can contribute to your savings in a year. That's provided you don't use these savings gained elsewhere.

6. Get help from a financial advisor

If you're struggling to save or invest your money, consider getting help from a financial advisor. A financial advisor can help you create a financial plan that meets your specific needs and goals and direct you to take more informed actions.

There’s a whole bunch of ways to save and grow your income. The main thing is to take the steps you need to reach your individual financial goals and needs. Most importantly, don’t compare yourself to others!

Found this article interesting? Share it with you family and friends!

Related Articles