By your 30s, a lot has changed. You've got a mortgage, a salary that actually matters, and a life that looks nothing like it did at 25. But while you've been busy levelling up, something important has probably been left behind: your insurance coverage.

It's not that you haven't tried. Most people in their 30s have some form of coverage. The problem is that what you set up in your 20s was built for a version of your life that no longer exists. Your income is higher. Your obligations are bigger, and your dependants are, well, depending on you. The gap between what you're covered for and what you actually need has been quietly growing ever since.

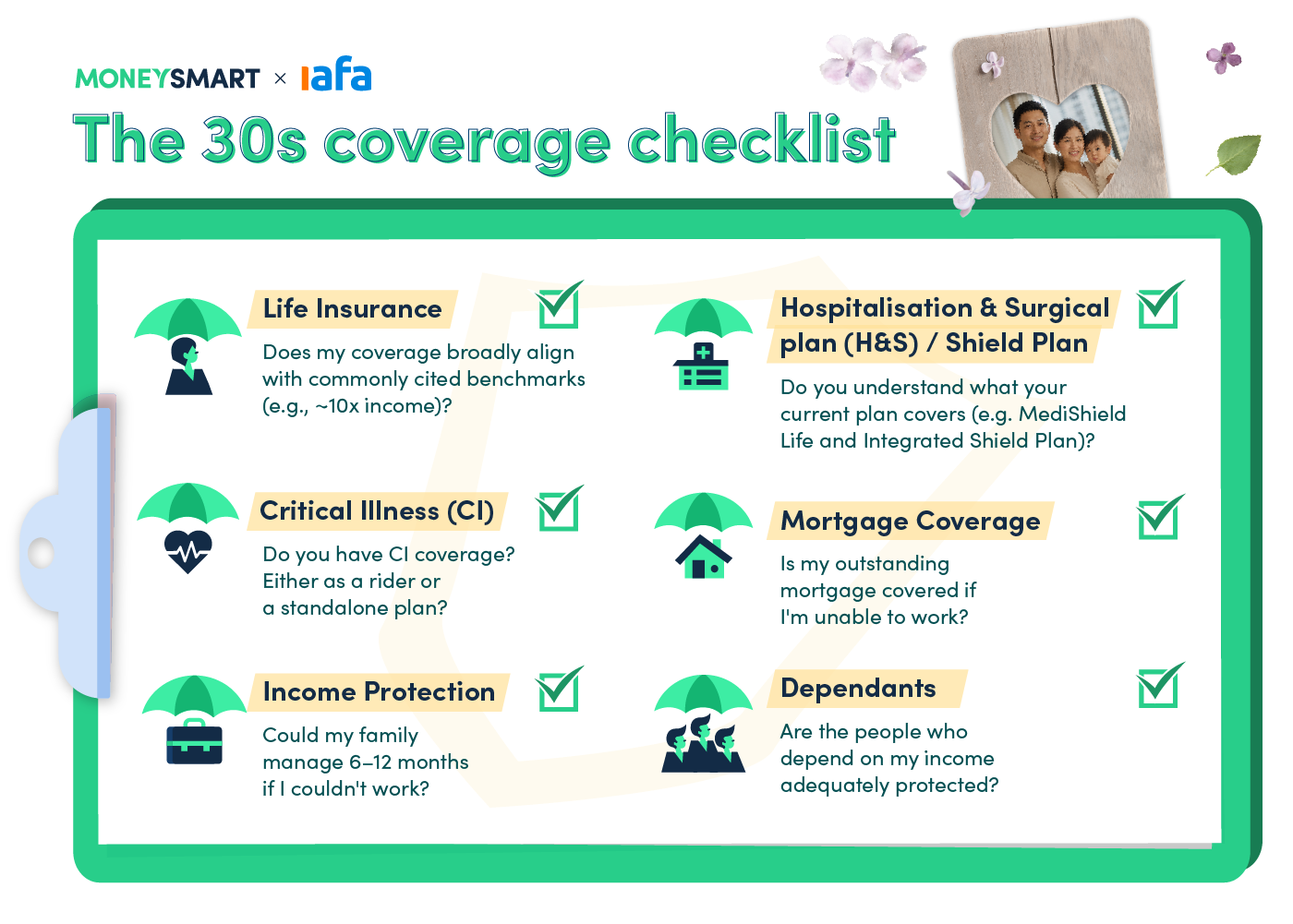

This checklist covers 6 areas worth reviewing. Be honest with yourself.

1. Life insurance: Is your sum assured still relevant?

According to the Life Insurance Association, 9–10 times your annual income is a general guideline for life cover, though the right amount will vary depending on your individual circumstances. If you took out a policy when you were earning $2,500 a month, your coverage needs may have changed, and likely by more than you think.

Life insurance isn't just about replacing your income when you're gone. It's about making sure the people who depend on you can continue to live the life you've built together—mortgage payments, school fees, daily expenses—without having to compromise.

Ask yourself: If something unexpected happens, could your family maintain their current lifestyle for the next 10 to 15 years?

2. Critical illness: Do you have sufficient coverage?

Critical Illness (CI) cover pays out a lump sum if you're diagnosed with a major illness like cancer, heart attack, or stroke, giving you financial breathing room to focus on recovery.

Many people assume their employer group plan covers this. It usually doesn't, or at least not adequately. According to a study by Life Insurance Association (LIA), economically active adults in Singapore carry a critical illness protection gap of 74%, amounting to an average shortfall of S$256,826—a gap that a group policy rider is unlikely to fill.

A CI payout isn't just for medical bills. Depending on your policy terms, it can help cover lost income during recovery, caregiving costs, and lifestyle adjustments that no one plans for until they're necessary.

Ask yourself: If you were diagnosed with a critical illness tomorrow, would your coverage be enough to let you focus on getting better, without your family having to worry about money?

3. Income protection: The coverage most Singaporeans overlook

Ask most people whether they're covered if they can't work, and they'll point to their savings. The maths often tells a different story.

According to Singapore's Household Expenditure Survey 2023, the average monthly household spending is S$5,931. 6 months of that comes to over S$35,000—and that's before factoring in mortgage repayments, which for many households run another S$2,000 to S$3,000 a month on top.

Income protection insurance replaces a portion of your salary if illness or injury stops you from working. It can be an important component of financial protection, especially for households running on two incomes. DINKs (dual income, no kids) couples in particular often assume their combined financial cushion makes them resilient.

But the OCBC Financial Wellness Index 2024 found that 58% of DINKs have not started making financial plans for their future—suggesting that a comfortable present doesn't always translate into protection for an uncertain one. In the event one income is disrupted, the other often isn't enough to carry both the lifestyle and the liabilities.

Ask yourself: Could your household genuinely manage 6 to 12 months of full expenses—mortgage included—if you stopped earning tomorrow?

4. Hospitalisation and surgical plan: Are you on the right tier?

When it comes to hospitalisation, having MediShield Life is the baseline. It covers Class B2 and C wards in hospitals—a solid foundation, but one that may no longer match your expectations or circumstances.

Integrated Shield Plans (IP) top up MediShield Life for access to higher ward classes or private hospitals. But having an IP isn't the same as having the right one. Many people signed up for whatever their employer offered years ago and haven't revisited it since.

If your lifestyle and income have grown, your hospital plan probably should too. The gap between a basic IP and one that actually fits your life can be significant when a large bill lands.

Ask yourself: Do you know what ward class your current plan covers, and whether that still reflects what you'd actually want if you were hospitalised tomorrow?

5. Mortgage coverage: Is your biggest liability protected?

For most Singaporeans, their home loan is their single largest financial commitment. HDB's Home Protection Scheme (HPS) covers your outstanding loan in the event of death or total permanent disability, which is a good start. But it doesn't cover scenarios where you're seriously ill and unable to work for an extended period, which is arguably a more likely risk.

As your mortgage balance, income, and life circumstances shift, so does what you actually need. Many people set this up once during the point of purchase and never revisit it.

Ask yourself: If you were unable to service your mortgage for 12 months due to illness, what would happen to your home?

6. Dependants: Does their coverage keep up with yours?

Once someone else's financial wellbeing depends on you, whether it's a spouse, a child, or an ageing parent, the equation changes. It's not enough to be well-covered yourself if the people relying on you aren't.

A common and quietly costly oversight is insuring yourself adequately while leaving dependants underinsured. For a non-working spouse, this might mean insufficient income protection if something happens to the breadwinner. For children, it may mean health coverage that stops at MediShield Life in a city where healthcare costs continue to rise.

Ask yourself: If you mapped out everyone who depends on your income today, would they be financially okay if you were gone?

The 30s coverage checklist

If you've paused on more than one of those questions, you're not alone. Many working adults in Singapore may find that their insurance coverage has not kept pace with the life they've built—not through any fault of their own, but because priorities change, and protection needs can shift over time.

The good news is that it doesn't take much to get clarity. A conversation with a financial adviser representative can help you better understand your coverage and options.

Speak to a financial adviser representative to assess your coverage needs.

This post was written in collaboration with Income. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best information in order for you to make personal financial decisions with confidence.

Related Articles