Taking out a loan to buy assets can be necessary and beneficial in certain situations, such as starting a business or purchasing a home. In Singapore, almost 50% are willing to take on debts to fulfil their life-long dreams of owning properties. What about taking out loans for investment purposes?

In the world of finance, investing a loan or margin trading is used to purchase stocks, bonds, and other securities instead of physical assets. This approach can potentially help investors amplify their gains by increasing the amount of capital available for investment, thereby earning them more than the rate of interest. However, similar to other types of loans, loans to invest come with a set of risks, which can sometimes be even greater.

Recently, we came across a question on Reddit that caught our interest (no pun intended): "Can You Take Out A Loan To Invest?". To gain a better understanding of investing in a loan and the benefits/risks associated with it, we decided to take a closer look at the responses provided in this thread and assess whether investing through loans is a wise decision or not.

Source: Reddit

How many types of loans are there, anyway?

Loans in Singapore are rather straightforward and are generally divided into two categories: Secured and Unsecured loans.

1) Secured loans

Secured loans are a type of loan where the borrower pledges an asset as collateral to the lender, which serves as security. These assets can be your valuable items such as houses, cars, or any other high-value possession. In case the loan is defaulted, the lender has the right to seize and sell your collateral to recover their losses.

Although the approval process for secured loans may take longer than unsecured loans, they allow a higher borrowing limit with lower interest rates. Here are some of the most common secured loans in Singapore right now.

Car Loan

If you want to purchase a dream car, you can take up a secured loan through banks or licensed lenders. With this, you are pledging the car as an asset for guarantee. The banks or lenders have the right to seize it should you be unable to repay the loan.

Make sure the amount used from your gross monthly income for paying all loans, or your Total Debt Servicing Ratio (TDSR), stays below the limit of 55%.

Also, take note of how much money is being borrowed compared to the actual value of the car that you want to buy. Notable banks in Singapore including DBS, Standard Chartered and OCBC offer competitive interest rates around 2.28% to 2.78% per annum.

Property Loan

Once you’ve chosen the property you wish to buy, the next step is to determine your financing options. If you’re purchasing a private property, your only option is to take a bank loan.

- For private properties under construction (BUC): If your condo, private or landed property is under construction, it’s best to choose a bank loan without a lock-in period so you can reprice or refinance to a lower interest rate eventually.

- For completed or resale private properties: There are competitive home loans with fixed or floating interest rates from major banks in Singapore that you can choose from. Do note that you cannot take HDB loans for private properties.

Check out the latest mortgage/home loan interest rates from major banks in Singapore for resale private properties and BUC private properties in this article.

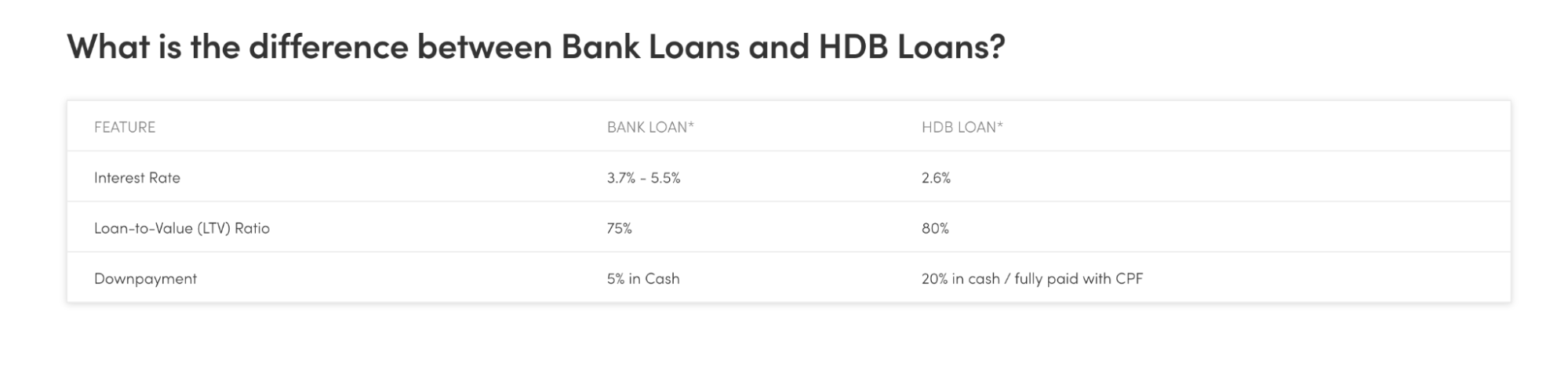

Meanwhile, to buy HDB flats, you can choose between a HDB Loan or a bank loan. You can apply for a HDB loan should you prefer a low-risk approach. They offer a fixed interest rate of 2.6%, a lower 10% downpayment splitting into two payments, and lenient mortgage repayments.

Differences between HDB & Bank Loan

Source:MoneySmart

If you have a good credit score with the capability to reprice and refinance your mortgage every few years, consider the wide variety of bank loan packages. At the end of the day, it comes down to your financial security and risk profile.

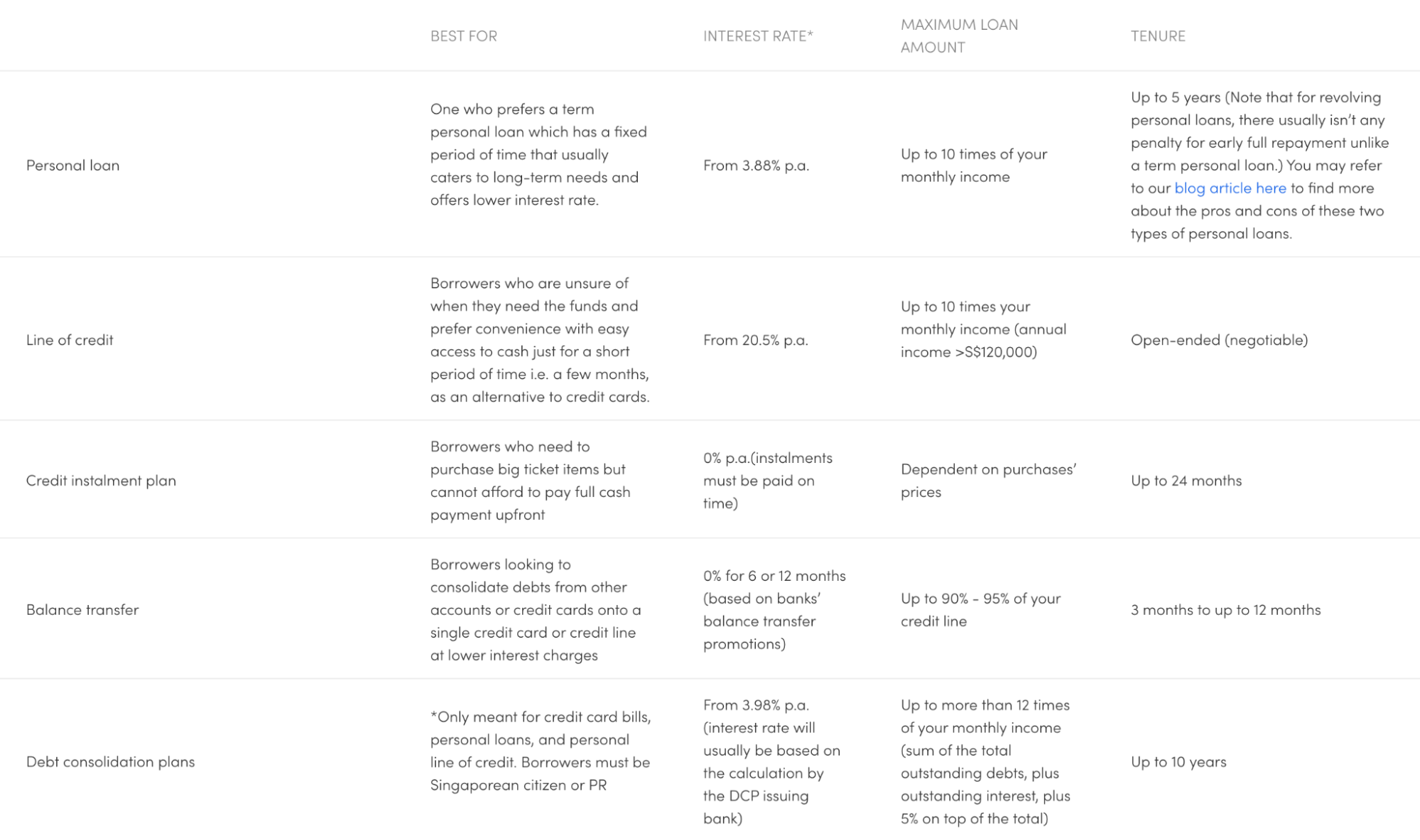

2) Unsecured loans

In contrast, unsecured loans don’t require collateral as a guarantee. They are assessed based on your credit score—the better the credit score is, the more likely you are up for approval. Unsecured loans usually have a fixed repayment period and higher interest rates than secured loans, as they don’t have physical assets to back.

Most personal loans available in Singapore are unsecured loans, with other categories include:

Source:MoneySmart

Why is it controversial to take out loans to invest?

Margin trading is no stranger to investors and traders in Singapore.

Simply put, it involves investing using borrowed money obtained from banks or stockbrokers. By taking out margin loans, you can purchase shares, stocks, and bonds that were previously unaffordable. It is a fast financing solution that yields great investment profits, exceeding the initial loans’ cost.

However, margin loans are debatable for their high risks. If your investments lose too much money, brokers will demand more funds or force-sell your shares to pay the loan. In Singapore, this happens when your margin level falls below 140%.

You can sink into debt if you're unable to pay the loan, leading to a damaged credit score, collateral seized, or even bankruptcy. Hence it is considered high-risk and recommended only for experienced investors. It's not advisable for risk-averse investors with limited financial resources.

Now that we have a better grasp on investing a loan, let's examine together whether the responses were helpful to our question.

Weighing on Redditors’ hot takes: “Taking out a loan is very risky unless you’re at a very old age”

Source: Reddit

Rating: ★★★★☆

Looking at the number of upvotes, many seem to agree that investments can only be made once we turn older and wiser. While it's true that saving money during your younger years is important, some have suggested investing along the way, instead of waiting. These include investing in insurance, medical insurance, PPF, equity & mutual funds.

In Singapore, many have started to invest in Singapore Savings Bonds (SSBs) as a way to diversify their portfolio. Another safe option is to automatically top-up your CPF Special Account (SA) which guarantees a return of 4-5% per annum.

The first thing you should do is carefully consider all of your financial resources and options. But in our opinion, it's neither too late nor too early to invest.

"Invest only the money you can lose"

Source: Reddit

Rating: ★★★★★

Not only does it present a memorable quote, but it also illustrates a frightening reality. Investing through borrowing may generate significant returns when the market rises, but it can also lead to losses of equal magnitude once the market becomes volatile.

For example, China's stock market faced major setbacks in 2015. Many inexperienced investors were pumping huge amounts of borrowed money via margin loans, leading to a surge in market volatility. As a result, the stock market experienced greater fluctuations than it would have otherwise.

When the bubble finally burst, investors sold their stocks en masse, thus amplifying the economic downturn. By estimation, over 80 million individual investors' fortunes evaporated in 1 year. We can’t stress enough that having a financial plan ahead of loaning is very crucial to you and your future security.

Here are a few examples of how to ensure it:

- Check credit history

- Consider financial budget

- Calculate (carefully) the interest rate

- Compare loan options

- Consider any collateral/assets involved

Win in life via wise planning. Without it, you are at risk of worsening your debt-to-income (DTI) ratio and can face personal bankruptcy.

“The question should be, can you earn >5 -7% to pay back your loan?”

Source: Reddit

Rating: ★★★★☆

Besides the response, ask yourself these additional questions:

- Will the investment increase your income?

- Is your interest less than your Return on Investment (ROI)?

- Can you afford the monthly payments, regardless of your investment’s performance?

If you can confidently say ‘Yes’, then there should be fewer worries, as you’ve probably planned out the phases of your investment. If not, this is a reminder for you to think twice about how manageable your investment will be in the long term.

“You can buy with margin on IBKR and other platforms. The interest rates are competitive unless you can borrow for even cheaper”

Source: Reddit

Rating: ★★★★★

When it comes to trades on SGX, IBKR offers some of the lowest minimum commissions in the market. In contrast, bank brokers like DBS Vickers or OCBC Securities can charge as much as S$25 per trade.

Alternatively, you can use CPF to invest or borrow funds from neobanks. Neobanks such as Trust Wallet often process and disburse loans faster, offering competitive rates and fees than the traditional ones, owing to their physical-less, low-operating costs.

But in this case, we do agree that IBKR is a more affordable and safer option. Compared to, let’s say, Saxo Markets, which requires a $5 minimum commission in their $1/month Bronze plan.

“I think you are referring to secured vs unsecured loans? Pledging a collateral allows FIs to loan you money at cheaper interest rates…”

Source: Reddit

Rating: ★★★★☆

To further illustrate, if you want to apply for unsecured loans in Singapore, you need to have a healthy credit score. This score should range from 1844-1910 (BB grade) to 1911-2000 (AA grade) as determined by the Credit Bureau of Singapore. They are considered the most optimal, demonstrating that you have a low risk of defaulting and a dependable credit history.

Anything lower will make it much more difficult to take out loans for properties, cars or even personal expenses. Here’s what you can do to improve your credit to an AA grade (or close to it):

- Always repay loans on time

- Don’t make multiple loans within a short amount of time

- Minimise the number of open credit facilities

- Repay short-term loans to repair damaged credit

- Never default on your loans

One thing to note, by leveraging margin yet being unable to pay back plus interest, your credit score will be damaged, thus making you ineligible for an unsecured loan application. Banks will then see you as a high-risk borrower and may outright reject your future applications, should you be in dire need of new loans.

So, back to the question. Loans to invest—is it worth it?

Well, ultimately, the decision rests with you. However, here are some key considerations before making up your mind:

The Pros & Cons of Taking Loans To Invest | |

Pros | Cons |

Potentially earn more than you would pay in interest & amplify returns | Have to pay interest plus other fees on the loan |

Borrowed funds provide the flexibility to purchase a variety of assets or securities | Losses will be amplified, which can result in margin calls or default |

Can purchase more securities than your cash balance allows | May risk worsening your debt-to-income (DTI) ratio. If unable to repay the loan, credit score can be damaged and possibly collateral seized |

While it may be tempting to pursue higher returns, you need to assess your level of risk tolerance, financial goals, and investment strategy. It's best to seek professional advice and verify whether the firms offering the assets are authorised to do so to avoid fraudulent transactions. They can help you make an informed decision and determine whether investing a loan is the right path for your financial situation.

Found this article useful? Share it with fellow investors!