This post was written in collaboration with Great Eastern. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best information in order for you to make personal financial decisions with confidence. You can view our Editorial Guidelines here.

Not all countries have access to basic healthcare at subsidised rates, but in Singapore we do. This means that we enjoy subsidies on our hospital bills, through government plans and policies — even before our private insurance plan kicks in.

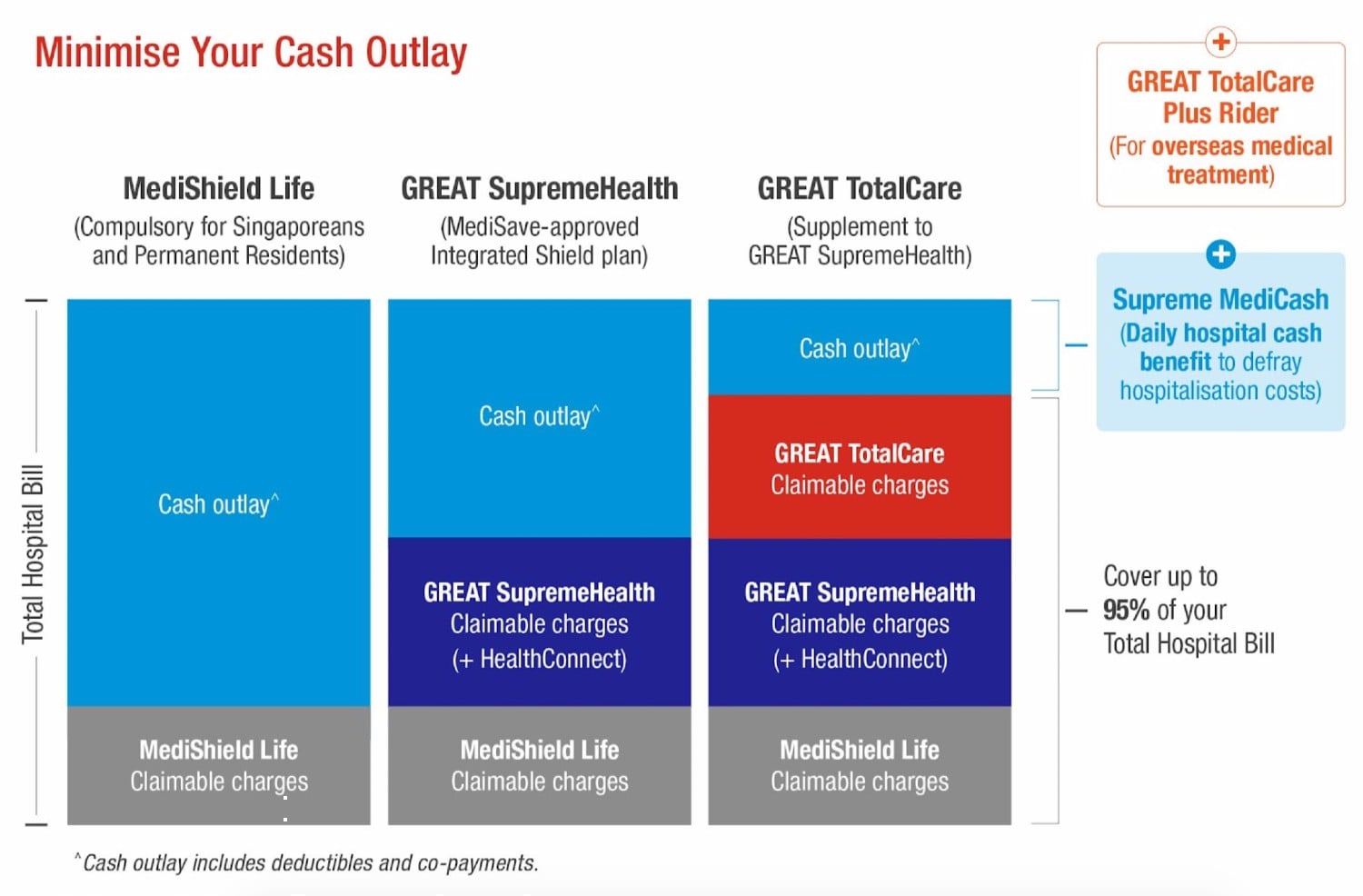

However, hospital bills can cost a fortune. Hence many of us buy some form of hospital plan — also known as an Integrated Shield plan or IP — to reduce out-of-pocket costs aka cash outlay or for coverage beyond the basic and even having care in a private hospital.

But the question on everyone’s mind is, should you get the highest-tier private IP available, a mid-range one, or just settle for the basic? I mean, the standard of healthcare in Singapore is generally high; so whether you opt for a private hospital or a restructured hospital, you’ll still be in good hands.

Let’s take a look at some scenarios to see how insurance can reduce our cash outlay, and to help us determine if we really need a private IP:

Scenario: Private hospital stay with surgery

Let’s introduce our fictitious character, Jim, who is in a private hospital for surgery. Using MediShield Life as the most basic coverage and basing the IP coverage on Great Eastern’s GREAT SupremeHealth (GSH) P Plus with and without the GREAT TotalCare (GTC) (Elite-P) supplementary plan.

P denotes coverage for private hospitals. With the add-on of Great Eastern’s GTC Elite-P supplementary plan, co-payment is limited to 5% of total hospital bills†.

Here’s how Jim’s estimated hospital bill would look like under the different tiers of coverage.

Incurred $10,000 at Private Hospital | MediShield Life only | GSH P Plus only | GSH P Plus and GTC (Elite-P) |

Eligible Hospital Bill | $2,500* | $10,000 | $10,000 |

Less: Deductible | $2,000 | $3,500 | $3,500 |

Less: Co-insurance | $50 | $650 | $650 |

Policyholder’s out-of-pocket cost | Deductible + Co-insurance + Excess of the hospital bill after applying the pro-ration factor | Deductible + Co-insurance | Co-payment (5% of the Eligible Hospital Bills) |

Claimable Amount | $450 | $5,850 | $9,500 |

* Since Jim stayed in a private hospital, his MediShield Life claim will be computed based on 25% of the bill. Jim will need to pay the excess of the hospital bill after applying the pro-ration factor.

Scenario: Restructured hospital stay with surgery

Let’s say Jim had decided to go with a restructured hospital instead. Here’s what his estimated hospital bill would look like under the different tiers of coverage.

Incurred $10,000 at Restructured Hospital — B1 ward | MediShield Life only | GSH P Plus only | GSH P Plus and GTC (Elite-P) |

Eligible Hospital Bill | $4,300‡ | $10,000 | $10,000 |

Less: Deductible | $2,000 | $2,500 | $2,500 |

Less: Co-insurance | $230 | $750 | $750 |

Policyholder’s out-of-pocket cost | Deductible + Co-insurance + Excess of the hospital bill after applying the pro-ration factor | Deductible + Co-insurance | Co-payment (5% of the Eligible Hospital Bills) |

Claimable Amount | $2,070 | $6,750 | $9,500 |

‡ Since Jim stayed in a B1 ward of a restructured hospital, his MediShield Life claim will be computed based on 43% of the bill. Jim will need to pay the excess of the hospital bill after applying the pro-ration factor.

Summary: Private hospital vs restructured hospital

Based on Jim’s scenarios above, his cash outlay is still manageable at a private hospital with the right insurance plan. Thus, here are some reasons why Jim would choose a private hospital over a restructured hospital:

Wait times: In general, people waiting to be admitted to a restructured hospital could expect longer wait times of 1 to 6 hours, as reported by the Ministry of Health. Meanwhile, for private hospitals, admission is usually within the first hour itself.

Comfort/privacy: There are various ward classes in a hospital, each offering a different level of comfort and privacy. For example, a B2 ward has up to 6 beds in the room, with a shared bathroom and there usually isn’t air-conditioning, your own TV or choice of meals. More privacy and comfort is accorded to class A wards in restructured hospitals.

Speed: You may have also heard of friends and family waiting weeks or months to get an appointment/surgery slot in a restructured hospital, while those going to a private hospital can somehow get treatment within the week. This is because the restructured hospitals have to cater to many more people than private hospitals at each time, hence it’s really on a first come, first served basis.

Otherwise…

It’s true that insurance premiums for restructured hospitals are lower, and subsidies for B2 and C class wards are higher. Some may prefer the social aspect of being in a ward with other patients, and some would rather opt for a non-air conditioned ward.

It’s also possible to just remain with MediShield Life alone and not get an IP if you’re content with basic care. You’ll be limited to class B2 and C wards, and out-of-pocket medical costs for pre- and post-hospitalisation are not covered.

In some cases, the individual could also be insured by his/her employer’s hospital plan, however this may be subject to limits and co-payments determined by the employer, and the plan would cease should the individual stop working for the company in the future (or retire).

All in all, it really depends on an individual's healthcare preferences and his/her budget available for insurance.

What Shield plans does Great Eastern have?

As we’ve been using Great Eastern’s GREAT SupremeHealth and its GREAT TotalCare supplementary plan in the scenarios above, let’s now look at these plans in more detail.

Compare Affordable Great Eastern Health Insurance Plans 2021

GREAT SupremeHealth

GREAT SupremeHealth is an Integrated Shield plan that complements MediShield Life. It offers varying tiers of coverage, corresponding to ward class and hospital type. Though largely covered, you’d still need to pay the deductible and co-insurance.

Plan | Great Eastern SupremeHealth — B Plus (Class B1 and lower, restructured hospitals) | Great Eastern SupremeHealth — A Plus (Class A and lower, restructured hospitals) | Great Eastern SupremeHealth — P Plus (Private and restructured hospitals) |

Annual coverage limit | $500,000 | $1 million | $1.5 million |

Annual premium (Singapore Citizen 35 ANB) | $390 (MediShield Life) + $80 = $470 | $390 (MediShield Life) + $123 = $513 | $390 (MediShield Life) + $322 = $712 |

GREAT TotalCare

This is the supplementary plan for GREAT SupremeHealth, and depending on the plan type chosen, it will reduce your co-payment to 5% of your hospital bill, capped at $3,000 per policy year†. This too, has varying coverage tiers.

GREAT TotalCare | Annual Benefit Limit | Co-payment to be borne by policyholder† | Annual premium (Singapore Citizen 35 ANB) |

Classic-B (Restructured Hospitals, Class B1 Wards & lower) | $150,000 | 5% of total Eligible Bills§ or the Deductible incurred under GREAT SupremeHealth (where applicable), whichever is higher | $67 |

Classic-A (Restructured Hospitals, Class A Wards & lower) | $200,000 | $81 | |

Classic-P (Private & Restructured Hospitals) | $400,000 |

| $335 |

Elite-B (Restructured Hospitals, Class B1 Wards & lower) | $150,000 | 5% of total Eligible Bills§ | $145 |

Elite-A (Restructured Hospitals, Class A Wards & lower) | $200,000 | $211 | |

Elite-P (Private & Restructured Hospitals) | $400,000 | $712 |

§ Eligible Bills refers to the Expenses incurred, subject to Pro-ration Factor (where applicable), which are similar to those applied to the GREAT SupremeHealth plan.

In addition, GREAT TotalCare is currently the only IP supplementary plan that provides Outpatient Cancer Treatment coverage of up to $10,000 per policy year (subject to co-payment levels) without a hospital stay. It covers the treatment of cancer provided by a hospital or a legally registered outpatient cancer treatment centre for outpatient cancer treatment, even after 365 days post-hospitalisation.

More add-ons:

- GREAT TotalCare Plus rider — for 24/7 specialised support on hand during overseas emergency situations.

- Supreme MediCash — to receive a daily cash benefit of up to $200 each day for hospitalisation due to illnesses (including COVID-19) and up to $400 each day for hospitalisation due to accidents, even when overseas.

Claims-adjusted pricing

GREAT TotalCare (Elite-P) or (Classic-P) policyholders can also benefit from claims-adjusted pricing, in which the premiums payable at each renewal is determined by one’s claims experience during the Assessment Period. i.e. Those at the Standard Premium Level who have made no claim during the Assessment Period, can enjoy the Preferred Premium Level which entails a 20% discount off their standard premium rates.

For a limited time only, sign up and enjoy 20% off first-year premiums for GREAT TotalCare (Elite- P) and (Classic-P) plans. Find out more about GREAT Eastern’s Integrated Shield plans here or request a call back from our Financial Representatives.

#Lifeproof your hospitalisation needs, for life.

Notes:

† Co-payment varies by Great TotalCare plan types and can be either (i) 5% of the total eligible bill; or (ii) 5% of the total eligible bill or the deductible, whichever is higher. The amount of co-payment required by the policyholders will be capped at $3,000 per policy year, for restructured hospitals claims and/or pre-authorised private hospital claims.

The information presented is for general information only and does not have regard to the specific investment objectives, financial situation or particular needs of any particular person. GREAT TotalCare and GREAT TotalCare Plus are not MediSave-approved Integrated Shield plans and premiums are not payable using MediSave.

GREAT TotalCare is designed to complement the benefits offered under GREAT SupremeHealth. GREAT TotalCare Plus is a rider that can only be attached to GREAT TotalCare to extend medical coverage worldwide.

Age stipulated refers to age next birthday (ANB).

This advertisement has not been reviewed by the Monetary Authority of Singapore.

The above is for general information only. It is not a contract of insurance. The precise terms and conditions of this insurance plan are specified in the policy contract.

Protected up to specified limits by SDIC.

Information correct as at 13 December 2021.