You hit that point in your career where you know you need an upgrade. Maybe you’re eyeing an intensive tech bootcamp to pivot industries, a specialist certification to secure the next promotion, or tackling a Master’s degree to break through the middle-management ceiling.

However, you’re currently weighed down with financial responsibilities. Between the monthly HDB mortgage, rising grocery bills, and family insurance premiums, allocating thousands of dollars in cash is a significant commitment.

Instead of draining your savings or putting career progression on hold, consider how you can finance via other means.

[ms-toc title="How to upskill on a budget"]

Why taking a loan is a calculated decision

We’re taught to approach personal loans with caution. Generally, it's solid advice. Taking out a loan to fund a luxury holiday or purchasing a depreciating asset is not advisable. However, education / professional upgrade serves a different function. When you upskill, you are actively investing in your future earning potential.

Rethinking "bad debt"

In wealth management, there’s a clear distinction between funding a lifestyle expense and leveraging capital to increase your net worth. Whether it’s for a 12-week coding bootcamp or for a comprehensive Master's degree, taking a loan to upskill is a highly calculated financial decision—with the goal of securing higher-paying roles.

With Singapore's statutory retirement age progressively rising to 64 in 2026, professionals are looking at a much longer career runway. Waiting years to save up means leaving money on the table, missing out on the higher salary you can earn during those extended working years.

Managing household obligations during study break

Unlike full-time university students, upskilling as a mid-career professional comes with existing financial commitments.

Mortgages, inflation, and emergency fund

Younger students may only need to consider transport and food. Whereas mid-career learners have ongoing responsibilities - mortgage payments, insurance premiums, and utilities.

With Singapore's annual inflation rate at 1.7%, fixed bills continue alongside the typical $1,465 baseline living expenses for a single adult. Paying $3,000 to $4,000 upfront easily can deplete rainy day savings. You need a financing solution to cover your education without compromising the cash buffers.

What about government grants?

While the SkillsFuture Level-Up Programme offers a generous $3,000 monthly allowance for select full-time courses, the situation is different for those under work-study programmes.

Adults taking part-time or specialised private certifications often have to cover thousands in out-of-pocket fees. Essentially, you’re on your own to figure out how to cover the remaining balance from somewhere, hopefully.

Why traditional financing falls short

When subsidies aren't enough, a study loan comes to mind. However, a major hurdle for adult learners in Singapore is that the traditional financial system caters almost exclusively to standard, multi-year academic tracks.

Strict criteria to qualify for education loans

Standard education loans from banks require enrolment in a multi-year undergraduate or Master's degree programme at officially recognised institutions.

Traditional loans are strictly designed to cover large-scale commitments. We are talking about programmes like the NUS MBA (approx. $99,000) or the 2-to-3-year SUSS Master of Counselling (ranges $30,000 to $50,000).

Professionals opting for short-term tech bootcamps at private providers like General Assembly, Vertical Institute, or Le Wagon find themselves ineligible for traditional education loans. Regardless, your need remains the same: a flexible, transparent way for manageable monthly payments.

Evaluating credit cards and legacy bank loans

If traditional study loans won't cover your course, how will you finance your studies? Most would turn to one of the two common—and costly—options.

Option 1: credit cards

Charge a $3,500 bootcamp fee or a $15,000 MBA directly to your credit card and it ties up your household credit limit. It gets a little problematic if you need that line of credit for emergencies.

Furthermore, if the balance is not paid in full by the end of the billing cycle, you are subjected to high interest rates of 18-27% p.a. Interest compounds quickly, redirecting any potential income upside to paying off those exorbitant interest fees.

Option 2: personal loans (from traditional banks)

On the other hand, personal loans often involve minimum quantums of $1,000 to $5,000. This rigid structure easily leads to over-borrowing, forcing you to pay interest on money you did not require.

Moreover, traditional bank loans include an extra cost: 1% to 3% processing fees. On larger sums required for executive diplomas, these percentage-based fees noticeably raise your effective interest rate, adding to your upskilling budget before you attend your first class.

Optimising course funding with a digital instalment loan

Don’t settle for financial products that don’t fit your circumstance. Find a financing method that avoids steep interest rates while allowing you to borrow the exact amount you require.

The shift towards digital financing

Here’s where digital instalment loans come into the picture. Instead of enforcing high borrowing minimums or restricting funds only to multi-year university degrees, digital loans offer a highly versatile approach to personal financing.

These platforms allow you to divide a lump-sum tuition bill into predictable monthly payments, making it much easier to budget alongside existing mortgage and living expenses. However, this should remain a calculated financial decision. Your chosen platform should offer transparency, zero hidden fees, and the flexibility to suit your learning needs.

Structuring your fees safely and transparently

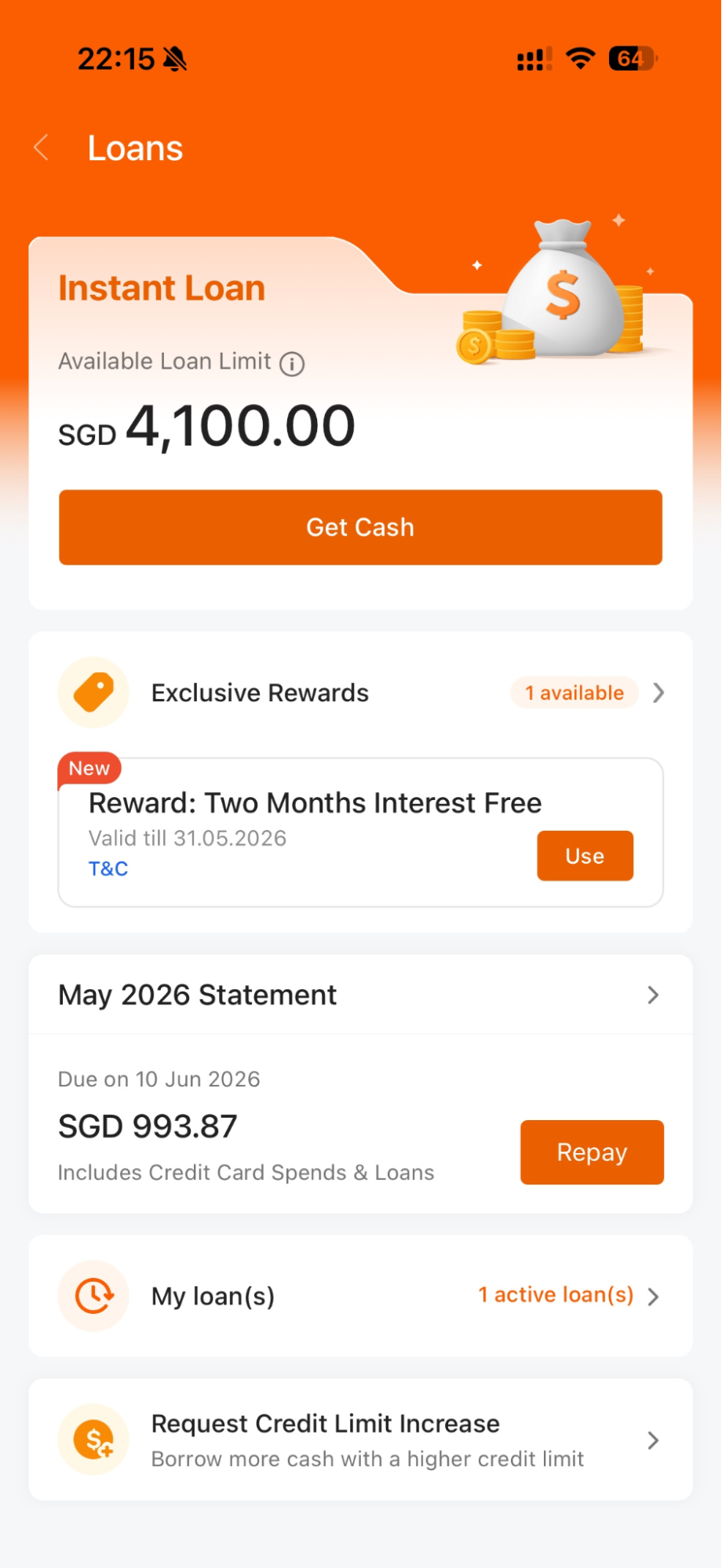

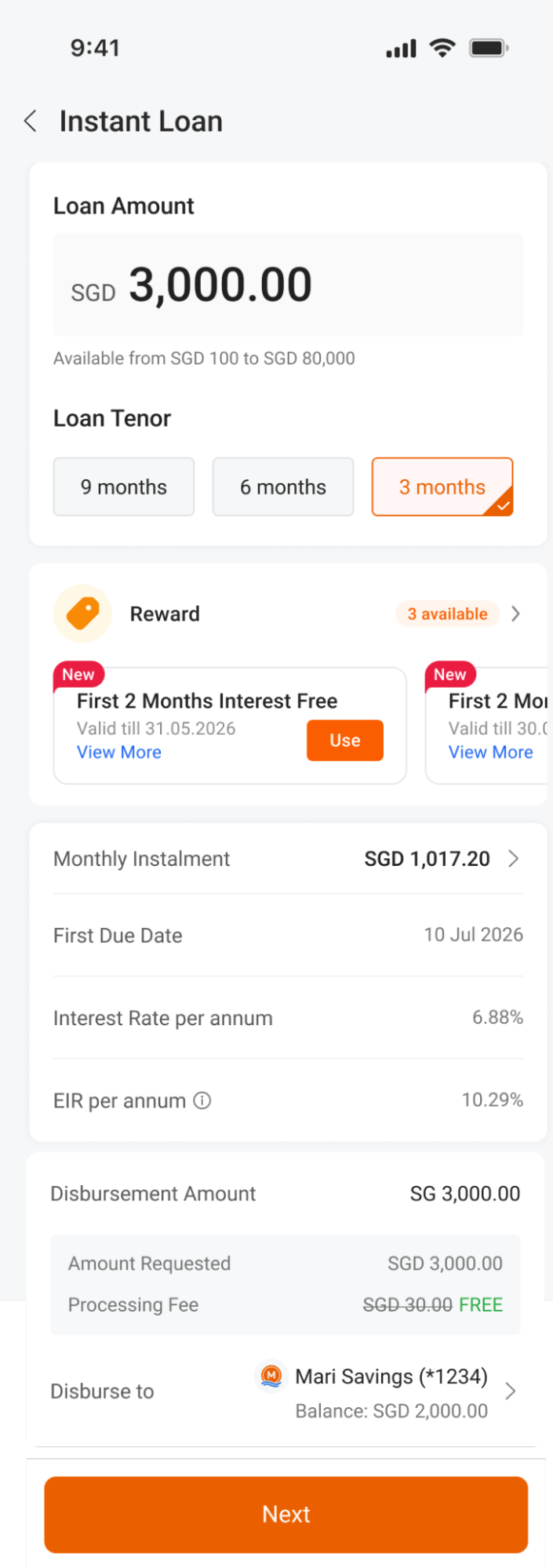

When evaluating, it is helpful to look for a facility that directly resolves the common issues of traditional options. For example, app-based options like MariBank Instant Loan are structured to serve as a calculated planning tool:

Image: MariBank

- Borrow what you need: Borrow the exact amount required, starting from as low as $100. This keeps your overall borrowing efficient, not paying interest on forced minimums.

Image: MariBank

- Zero processing fees: Proper financial planning demands complete transparency. The app charges zero processing fees. Without a 1% to 3% deduction, the rate you see is exactly what you get.

- Instant, straightforward approval: Working adults do not have time for extensive paperwork. The app provides instant pre-approved visibility via Singpass, letting you secure your funding efficiently so you can focus on your studies.

Comparing your financing options

It becomes clear why selecting the right tool is as important as selecting the right course. Here is an objective summary of how the 4 main financing options stack up:

Final words

Investing in yourself is a practical way to navigate inflation and a competitive job market. Whether it’s a short technical course or Master's degree, taking a loan to finance your education is a highly calculated investment to boost your own market value while keeping your finances stable.

Level up on your own terms. Consider the MariBank Instant Loan for your precise cash flow needs, and explore their promo today. Get a 1-month interest free when you apply for an Instant Loan with our promo code <MBMS2026>.

This post was written in collaboration with MariBank. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best information in order for you to make personal financial decisions with confidence.

Related Articles