When we look at financial literacy in Singapore, it’s almost non-existent in the formal education system at the younger ages. That’s a shame because the money habits (and competence) that we pick up when we’re young are crucial lifelong skills that shape our money mindset in adulthood.

There are many instances of individuals reaching out in community forums and looking for “help” with their financial situation. One popular place where this happens is on Reddit, perhaps the most prominent of these community forums.

Users there are pretty open about their situation and are willing to share details with others on the platform. So, let’s take a look at one such Reddit thread and I’ll share some general observations on how someone in a similar situation could think about improving their finances.

[ms-toc title='How to start investing as a 33-year-old in Singapore']

Starting your financial journey in your 30s

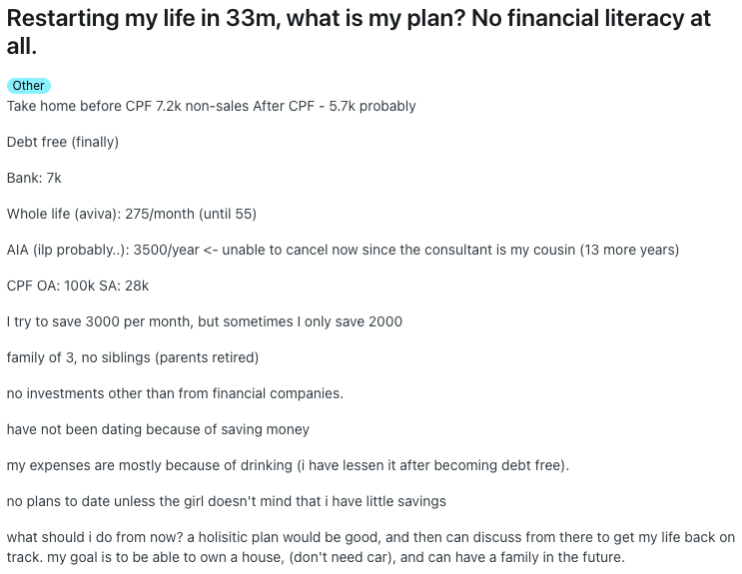

The OP in this case is a 33-year-old male who described himself as having no “financial literacy”. This might resonate with many people in their late 20s/early-to-mid 30s, and the question becomes: is it too late to start your financial journey?

The answer is of course, “no”. As the saying goes, when it comes to investing or getting your finances in order, “The best time to start was yesterday, but the next best time to start is now”.

Let’s take a deeper look at his current situation.

Current monthly obligations and situation

The OP reported a take-home pay of $5,700 and average monthly savings of about $2,000. That equates to a 35% savings rate, which is an extremely solid number.

He aims to save $3,000 per month, but if he can hit in between those two numbers (so save $2,500 per month), then his savings rate would go up to nearly 44%.

However, the OP has 2 significant ongoing costs: a whole-life policy that costs $275 per month and an investment-linked policy (ILP) that works out to just over $290 per month. I’ll be conservative and assume those premiums have to be paid out of his monthly “savings” stash.

Given those monthly premiums total over $550, that eats up over 25% of his current stated monthly savings of $2,000 per month. That’s a big chunk.

Whole-life and ILP products typically combine insurance protection with an investment component. Because of this structure, the premiums are usually higher than for standalone term insurance. The investment portions of ILPs, in particular, are often compared with alternatives like exchange-traded funds (ETFs) in terms of fees, performance, and flexibility.

Some typical ways individuals approach this include:

- Calculating long-term costs and returns to see how these premiums affect savings over time.

- Considering life stage needs (e.g., protection for dependents, property planning, retirement) to determine if the type of coverage still fits.

- Requesting an insurance review—a process where existing plans are assessed to check if they remain suitable or if adjustments might make sense—can be a useful exercise.

By exploring these options, he can build a clearer picture of whether his insurance spending still fits in his current life stage.

Focus on building a safety buffer

Another common consideration in personal finance is setting aside cash for an emergency fund—a pool of money that can cover several months of essential living expenses in case of unexpected events.

This is to ensure that if the OP loses his job or has an emergency he needs to pay for, he has sufficient cash to “keep the lights on”, so to speak. Many sources suggest 3 to 6 months of expenses as a reference point, though the exact amount depends on individual circumstances.

Given he’s saving $2,000 and taking home a salary of $5,700 per month, his monthly expenses work out to be $3,700. Based on that, an emergency fund with 6 months’ worth of expenses would be $22,200. His $7,000 in the bank is a good starting point to build this.

Where should he put those funds? There are different approaches people often explore when deciding where to keep an emergency fund:

- Regular savings accounts: Easy access, but usually lower returns.

- Singapore Savings Bonds (SSBs): Government-backed, relatively safe, and offering some interest.

- Short-duration bond funds: Potential for higher yields, though with added market risk.

Based on his monthly savings of $2,000, he could meet the $22,200 target in just under a year.

ALSO READ: Why Every Singaporean Needs an Emergency Fund—And How You Can Build Yours

Then consider investing

What about investing? Well, after building a safety buffer and reviewing insurance coverage, many people turn their attention to investing. The aim is usually to grow wealth over time and keep pace with inflation.

Some investors begin with small, regular contributions (say 5-10% of monthly savings) to diversified investment products, such as exchange-traded funds (ETFs), to gain exposure to markets gradually. The key is understanding one’s risk tolerance and goals before committing funds.

Once a solid financial foundation is in place, exploring diversified, low-cost investment options—like global index-tracking funds—may be one of several ways to build long-term wealth.

Each of these paths involves trade-offs in terms of risk, cost, and involvement. For the OP, thinking through these factors, or discussing them with a financial professional, could help clarify which approach, if any, feels most suitable at his stage.

What about CPF?

The OP shared that he has $100,000 in his CPF Ordinary Account (CPF OA) and $28,000 in the CPF Special Account (CPF SA). For many Singaporeans, CPF plays multiple roles: the OA can be tapped for housing, while the SA is designed to grow steadily for retirement with a base interest rate of 4% per year.

For the OP, this raises several considerations. Since he has mentioned future goals of owning a home and starting a family, his OA funds may eventually be important for a property down payment and mortgage servicing.

Assuming he remains single, he can potentially buy a HDB flat in 2 years (at age 35), and then the funds in his CPF OA will become important for funding the deposit for a property and any mortgage payments.

Meanwhile, his SA funds will continue to earn 4% interest, and there’ll be a step up in his SA contributions from his monthly CPF contribution once he hits 35, to close to 19%. In essence, the SA is really for retirement and should be viewed as such.

Under current CPF guidelines, members who reach the Full Retirement Sum (FRS) at age 55 can expect monthly payouts from CPF LIFE at 65. If he can hit the CPF Full Retirement Sum (FRS), which is currently $213,000, by the time he is 55, then he can enjoy monthly payouts from CPF LIFE at 65 of up to $1,730 per month. Actual future amounts will vary with inflation and policy updates.

Even better would be to meet the Enhanced Retirement Sum (ERS)–which right now is $426,000–and that can allow you to enjoy monthly payments of up to $3,300 at age 65.

Of course, the above amounts are for those aged 55 right now, so by the time the OP retires in 30 years or so, the FRS, ERS, and monthly payouts will be higher, in line with inflation.

Source: CPF.gov.sg

ALSO READ: CPF Changes in 2025–2026: What’s New, Who It Affects & What You Should Do Now

Lifestyle changes

The OP does say that a lot of his expenses come from “drinking”, which I take to mean alcoholic drinks, and we all know they are prohibitively expensive in Singapore.

Given the hefty excise taxes the Singapore Government imposes on alcohol, the average prices of drinks in the Lion City are among the highest in the world.

For the OP, this presents a potential area to reflect on. Some individuals in similar situations choose to:

- Track how much they spend on discretionary items like alcohol each month.

- Compare this amount with other priorities, such as building savings, travel, or health-related expenses.

- Consider alternatives, like redirecting some of that spending toward activities that provide long-term benefits, whether financial (increased savings) or personal (fitness memberships, hobbies, or wellness).

By reviewing his discretionary expenses, the OP could get a clearer sense of how lifestyle choices affect his overall budget and how those choices align with his longer-term goals.

Learn about markets and investing

For the OP, another step to consider—whether now or alongside building his financial foundation—is learning more about how markets and financial products work.

That’s because if we educate ourselves on the pitfalls, as well as opportunities, out there, we are better-equipped to understand what we should avoid while also ensuring we direct our savings towards the channels that can best serve our financial goals.

For the OP, focusing on education could mean reading about how stock markets operate, exploring how insurance and investment products differ, or simply following reputable financial resources.

And here’s the encouraging part: with steady savings habits, a growing understanding of financial products, and the willingness to keep learning, the OP isn’t “behind.”

In fact, He’s taking foundational steps that could help build financial resilience and flexibility over time.

Know someone who's trying to restart their finances too? Share this article with them!

The information provided in this article is for general information and educational purposes only and does not constitute financial advice. Readers should seek advice from a licensed financial adviser before making any investment or insurance decisions.

Related Articles