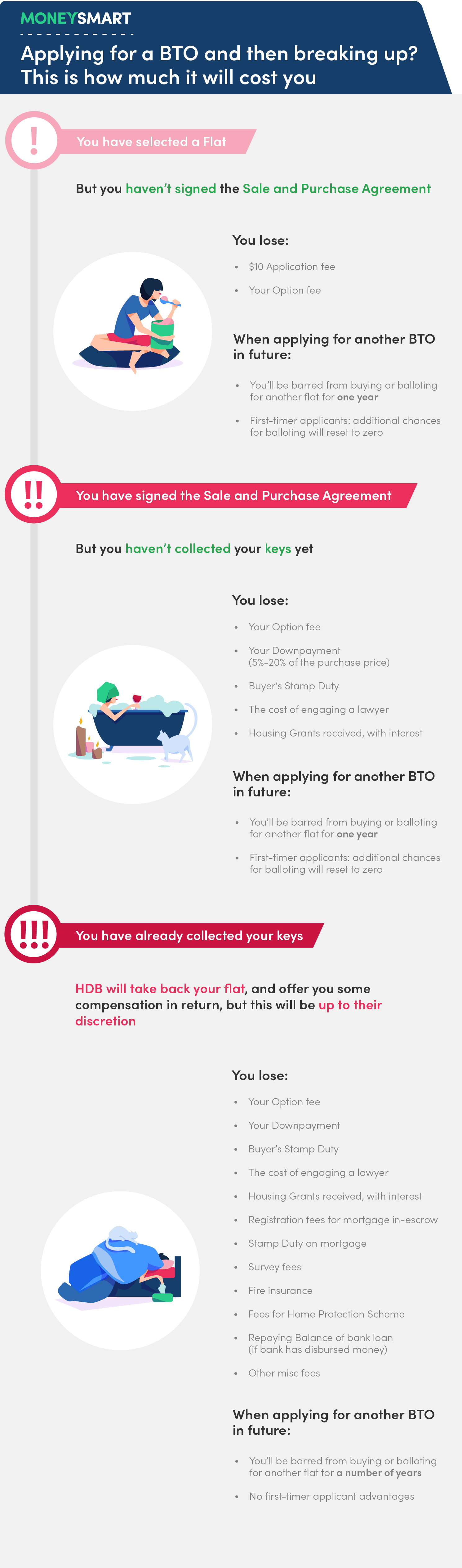

Breakups are one of the worst experiences some of us will ever go through. But it gets so much worse if you and your ex have already balloted for a BTO flat. Not only do you have to witness the falling apart of a relationship you thought would last a lifetime, you also lose money.

When you buy a BTO flat as a fiancé/fiancée, the HDB requires that you register your marriage by a certain date. If you fail to do this, you are no longer eligible for the flat and will have to cancel the purchase.

How much money you lose depends on how far you have advanced along the HDB BTO timeline. So, if you’re getting cold feet and want to call off the marriage, it’s better do so as early as you can.

Here’s what to expect when you break up and have to cancel your BTO flat purchase:

Stage 1: Breaking up after HDB BTO unit selection

So you’ve balloted for a flat, and been selected to pick a unit. When you chose your unit, you would have paid an Option Fee of $2,000 for a 4/5 room flat, $1,000 for a 3-room flat or $500 for a 2-room flexi flat.

The only cash you lose, other than the $10 application fee, will be the option fee. Financially, you’ll have emerged relatively unscathed, as couples who have signed the Sale and Purchase Agreement stand to lose a lot more.

You’ll not be allowed to apply to buy or ballot for another flat for one year. And the next time you decide to ballot for a flat, either as a single or with a new love, additional chances accumulated from previous unsuccessful applications will be reset to zero so you won’t find it any easier to get a flat.

Stage 2: Breaking up after signing the Sale and Purchase Agreement but haven’t collected your keys yet

At this stage in the purchase process, you would have already paid a total of 5% to 20% of the property’s purchase price as downpayment. This sum would include the option fee you paid earlier when booking the flat.

At this stage in the purchase process, you would have already paid a total of 5% to 20% of the property’s purchase price as downpayment. This sum would include the option fee you paid earlier when booking the flat.

If you are taking out an HDB loan you would have paid 20% of the purchase price (or 5% if under the Staggered Downpayment Scheme). Those taking out bank loans would have paid 20% of the purchase price (or 10% if under the Staggered Downpayment Scheme).

You would also have paid the Buyer’s Stamp Duty, as well as the cost of engaging a lawyer, whether HDB’s or your own.

Assuming you are buying a $400,000 flat and taking out a bank loan, that would mean you’d lose 20% of the purchase price amounting to $80,000, as well as $6,600 being Buyer’s Stamp Duty, and legal fees and disbursements incurred by the lawyer for lodging a caveat, etc.

Do note that it might be possible for your/HDB’s lawyer to apply to IRAS to ask for a refund of your Buyer’s Stamp Duty. HDB will excuse you from paying their conveyancing fee if you’re using their lawyers, but an external lawyer will not.

You will also have to give back to the government the housing grants you’ve received with interest, so hopefully you haven’t spent them on anything yet.

Finally, it goes without saying that you’ll be barred from balloting for or buying a flat for a year, and lose your advantages as a first-timer applicant the next time you do decide to ballot.

Stage 3: Breaking up after key collection

So you received notice that your keys were ready for collection, and that you would need to submit your ROM cert by a certain date. But in the end you didn’t go through with the marriage

In this case, the BTO flat is already in your possession and will have to be surrendered to the HDB.

At this stage, you would have already paid the balance of the purchase price of the flat using cash, CPF funds, and/or disbursements of your bank loan.

There are other miscellaneous fees you will have incurred at this point, such as registration fees for your mortgage in-escrow if you’re taking out a loan, stamp duty on your mortgage, survey fees, as well as fire insurance and fees for the Home Protection Scheme.

The HDB will take back your flat and offer you some compensation in return, the amount of which will be determined at their discretion, but you can still expect to lose quite a bit of money. If your bank has already disbursed your home loan, don’t forget that a large chunk of this money will have to go towards repaying this loan.

You’ll also be barred from applying for another BTO flat for a number of years.

As you can see, breaking up in Singapore is hard when there’s a BTO flat involved. Be that as it may, if you get a sinking feeling when you think of tying the knot, you’re better off going for counselling and if that doesn’t change things, calling off the union altogether. The consequences of a divorce can be far costlier and more emotionally draining.

Found this article useful? Share it with your family and friends.

Related Articles